It will be no surprise to PeakProsperity.com readers that the news coming out of the Eurozone just gets worse and worse. The reality is that Ireland, Portugal, Spain, Italy, Belgium, Greece, and France (in no particular order) are all in debt traps from which there is no escape. A debt trap is sprung when bankruptcy becomes the only outcome. With corporations, this usually becomes readily apparent and directors are forced by law to stop trading, but countries conceal this reality by printing money. Otherwise there is no difference in the two cases, despite what politicians and neoclassical economists would have us believe. This is why we are painfully aware that the Eurozone is in trouble, since nation states are unable to cover and conceal their obligations by printing money, having surrendered this role to the European Central Bank (ECB).

The ECB is meant to be independent of politics and political pressures. But the reality facing any central banker is that s/he cannot stand by and let politicians drown in their own mess. The politicians know this, and it's what is behind current attempts to move away from austerity towards Keynesian growth. The plea is exactly the same as that of the spendthrift who tells his bank manager that the only chance he has of getting his money back is to increase the overdraft to allow him to trade his way out of difficulty.

So the ECB knows, in its role as bank manager, that the argument is flawed. But unlike spendthrift individuals, politicians have real power, and the ECB has an ultimate responsibility not to upset the apple cart. And that is why the election of a new socialist French president is important. President Hollande is leading the charge away from austerity in Europe, and he has powerful allies, including President Obama in his own election year.

Unfortunately, the ECB and the politicians lack a proper understanding of their economic condition because they continue to operate within the neoclassical framework that has led them into this mess. The lack of understanding of the relationship between the elements of hard-to-predict future consumer preferences, as well as the entrepreneurial function and the role of time in their calculations, has led to a reliance on sterile economic models. These leave no room for the dynamic and unpredictable creativity of human nature that gives us real economic progress. It is the difference between a proper understanding of the role of free markets, and thinking they can be manipulated to achieve an outcome preferred by the state without adverse consequences. An important consequence has been the creation of credit-induced business cycles leading to escalating levels of debt in both private and public sectors, which is why so many countries have become ensnared in debt traps. This statement of the obvious is not recognised by Keynesians and monetarists who continue to argue that the solution is yet more debt, more stimuli, and the avoidance of deflation at all costs. And it is neoclassical Keynesians and monetarists that populate the central banks and advise politicians.

This brings us to an important consideration: Despite what her officials say publicly, austerity has limited support within the ECB itself, because it is run at the top by neoclassical economists. Instead, the real constraint is Germany, whose citizens’ savings are on the line and which faces the prospect of its third currency collapse in a century. So this is where the lines are drawn up: spendthrifts desperate for more money, a conflicted central bank, and Germany.

Angela Merkel has made considerable progress in pushing the German electorate in a direction that is completely against its instincts by playing the political card marked “there is no alternative.” With her considerable political skills, she may be able to push her people some more, but it is becoming increasingly difficult, because everyone in Germany can see that committing real savings to bailing out the spendthrifts only wipes out the savings. These are not euros simply conjured out of thin air, because the Bundesbank cannot print them and probably wouldn’t do so anyway. But the pressure is mounting on her, and she is being squeezed by governments such as the British and the Americans, who are now panicking over the consequences of failure.

This is why both countries went public last week, with David Cameron even visiting Merkel in person. It is a sure indication that major governments outside the Eurozone are beginning to expect the worst, and that unless Germany gives way, it will happen quickly.

Eurozone bank lending

While there is a stalemate at government and central bank level, this is far from the case in commercial banking. The period of expanding bank credit, which gave rise to unsustainable levels of debt, ended with the banking crisis in 2008, and since then, central banks have been dealing with the aftermath. The Eurozone countries facing problems today were beneficiaries of bank credit expansion, and thus are badly hit by the subsequent contraction.

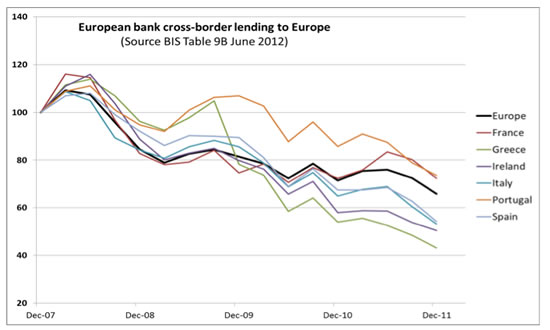

The chart below illustrates how Eurozone bank lending is collapsing, and represents European cross-border bank lending between European countries, rebased to 100 at 31 December 2007. The total is shown by the heavy black line, along with lending to selected Eurozone countries.

It becomes clear from this chart why the ECB offered its long-term refinancing operation last February, when it injected €530bn in raw cash into the banks. The contraction of cross-border lending was accelerating, having completely absorbed the November injection of €489bn. And it tells us that more LTRO injections will be needed very soon.

The underlying picture is more complex than shown by one chart. The lending shown is to both private and public sectors, and the drop in cross-border lending to governments was partially replaced by increased lending from domestic sources on the back of the ECB’s LTRO, and also by US banks (see below). But given that the Eurozone’s banks are already highly exposed to their individual governments, this increase in loan concentration has undermined their creditworthiness; hence the continuing ratings agency downgrading of the banks involved.

A further concern is that government borrowing is crowding out the private sector. Private sector borrowers are being badly squeezed, not only for capital investment funding but also for their working capital requirements. The consequence is that governments with large budget deficits are not going to get the future tax revenues assumed in economic forecasts.

This is why the only solution to the Eurozone’s problems is a round of massive and immediate cuts in public spending. Without these cuts, the destruction of real savings, vital to the economic wellbeing of society itself, continues. In the past, this destruction was a relatively slow process, but the speed at which it is now happening has accelerated exponentially. The importance of cutting public spending has become more urgent; unfortunately, the election of President Hollande in France has delayed this process.

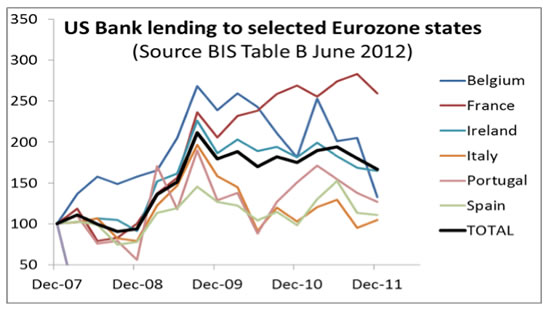

Help from outsiders only delays the inevitable and increases their exposure to the Eurozone’s problems. Lending to Eurozone countries by US banks has expanded in all the cases shown in the chart below, though lending totals have fluctuated widely. But total lending (the heavy black line) is still up 67% from December 2007. A cynic might say that the Fed has encouraged US banks to increase their lending to the Eurozone, on the basis that no banker in his right mind would have otherwise done so. But if this is true, the Fed has little flexibility to continue with this support, given that commercial bankers will be increasingly reluctant to commit further funds. It explains President Obama’s interest in the current state of the Eurozone, because if it goes down, there will have to be a major capital injection into US banks to keep them solvent. We get used to trillions being thrown around, but that is government spending and money-printing; in the context of the Wall Street banks, the quantities are not small, with the lending total at end-December 2011 being $347bn.

It is hard to conclude anything other than that all of the avenues for resolution have been explored and substantial sums of money thrown at the problem, much of it without the public’s knowledge. The ECB has expanded its balance sheet to offset cross-border lending contraction, and other central banks, particularly the Fed, have done their bit. Germany has committed enough of her own citizens’ savings to fill what is obviously a bottomless pit. New investors, except wild speculators, are non-existent. And without more outside help, Eurozone institutions do not have the resources to avoid a financial collapse.

That outside help is not there. The result is that the Eurozone is failing at an accelerating rate. George Soros is on record as giving Euroland three months. It will be lucky to last that long.

Points arising

While it's impossible to foresee the precise order of events in this accelerating collapse, in Part II: The Most Predictable Next Events, we detail the inevitable developments that will almost certainly arise over the course of Europe's struggle.

Remember that most commentators have little understanding of the true position, or are trained in neoclassical economics (if at all), and are generally recycling someone else’s take on things. Also bear in mind that the Eurozone’s politicians are desperate to allow no steps backwards in their cherished project, because they suspect that any regression will kill not only the euro, but the whole EU project. Everything will be done to prevent countries from leaving the Eurozone, including ignoring problems in the hope they will go away. And the bigger the country, the more resolute everyone will be to stop them from leaving.

Click here to access Part II of this report (free executive summary; paid enrollment required for full access).

This is a companion discussion topic for the original entry at https://peakprosperity.com/abandoning-ship/