The central planners are in a state of fear and panic. They are trying everything and anything to create market validation for their policies, watching with trepidation as their favored economic metrics fail to respond to all of their frenzied efforts.

They are so far over the tips of their skis right now that there's nothing they won't do. They've summarily thrown granny under the bus because they have this idea that negative real interest rates are the cure. The cure for what? The massive amounts of debts and imbalances their prior policies caused. So savers are punished in the pursuit of policy. You know, 'for the greater good' and all that.

They've spurred the greatest wealth gap ever in US history, greater even than at the extremes of the Great Depression, apparently without the slightest concerns for Plutarch's ancient admonition that "An imbalance between rich and poor is the oldest and most fatal ailment of all republics."

They've even gone so far in Europe as to now force negative nominal interest rates on savers, dispensing with their usual slight-of-hand of letting inflation steal from each unit of currency in their system. When you're panicking, there's no time for subtlety.

They look the other way as "someone" dumps huge amounts of gold contracts into the wee hours of the night, seeking one thing and one thing only: lower prices. But that's okay because the central banks destroyed price discovery a long, long time ago. First by invalidating the price of money itself (by driving interest rates to zero), and then in everything else -- most importantly risk.

The Federal Reserve, the Bank of Japan (BOJ), and the ECB have decided that they want you to take your money out of your bank account and place it into the stock market. Apparently they have models that say this is a good thing. Or they just want you to spend it. And to be sure that you follow their wishes, they don't leave you any better options -- and so virtually every hard asset has been targeted for price suppression. Except real estate because, hey, you have to borrow a lot of money from the banks for that, so they encourage and cheer your participation there.

In short, everything the central planners have tried has failed to bring widespread prosperity and has instead concentrated it dangerously at the top. Whether by coincidence or conspiracy, every possible escape hatch for 99.5% of the people has been welded shut. We are all captives in a dysfunctional system of money, run by a few for the few, and it is headed for complete disaster.

To understand why, in all its terrible and fascinating glory, we need look no further than Japan.

A Black Swan Flaps Its Wings

Back in 2012, Japan was my favorite candidate to be the black swan of the year -- meaning it could shock everyone and flip our reality to a new state. Of course, this has taken longer to play out than I initially thought.

However, here in November 2014, the world finally seems to be on the verge of waking up to the inevitable financial disaster that stalks Japan.

Japan is really in no better or worse shape than the rest of the developed world. But is a few chapters further along in the story, which means it holds both explanatory and predictive power for most of the developed nations. This is why we should study it closely.

The mystery, as always, is how so many participants are willing to pretend all is normal with Japan; merrily buying and holding Japanese yen and government debt instruments.

In a nutshell, every single monetary, economic, fiscal and demographic trend is working against the very goals that the Bank of Japan, in cahoots with the Japanese government, is trying to attain.

To make this clear, first, we're going to sketch the outlines of predicament and then, next, examine what will happen when it all finally breaks down.

The Halloween Massacre

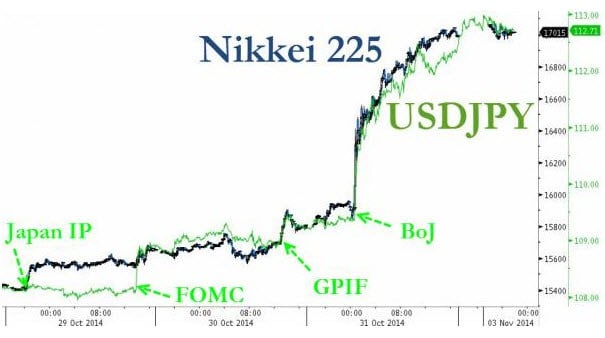

On Friday, October 31 2014 the Bank of Japan (BOJ) made a surprise announcement of a major new policy move that was specifically targeted to have maximum impact on the markets.

But it wasn't a unanimous or popular decision:

Split Vote Shows BOJ’s Kuroda Walking on Tightrope

Nov 2, 2014

TOKYO—The Bank of Japan ’s surprise move to flood the economy with more money boosted stock prices and gave a lift to its fight against deflation, but a rare split vote over the decision means further action will be difficult for Gov. Haruhiko Kuroda.

Those with knowledge of the maneuverings behind Friday’s 5-4 decision to step up the central bank’s yearly asset purchases point to growing skepticism among the BOJ’s nine policy board members toward the radical policy rolled out by Mr. Kuroda a year-and-a-half ago.

(Source)

The announcement specifically was that the BOJ would increase its purchases of Japanese government bonds to 80 trillion yen (up from 60 - 70 trillion) and triple its purchases of stock funds to 3 trillion yen annually.

You have to love the coded phrase used in the above article -- "gave a lift to its fight against deflation" -- which decoded means "they partially wrecked the yen which makes import prices go up (and which is not the same thing as the inflation they seek)." When you wreck your currency, all you do is steal purchasing power from savers and transfer it somewhere else, in this case to those most indebted and/or leveraged -- the biggest of these beneficiaries being the Japanese government and large speculators.

Also the 5-4 decision is quite telling. It indicates that this bold -- or reckless -- policy (depending on your point of view), is already not very popular, suggesting that it's more of a last desperate. Patience is wearing thin.

While some still question whether the US Federal Reserve is monkeying about directly in US equity markets, there is no such uncertainty with the BOJ: it openly buys equities under the pretense that a rising equity market is somehow good for the Japanese economy. This is a rather indefensible view, because the relative elevation of the Nikkei has nothing to do with how the economy will perform, as it's a derivative of the economy (or is supposed to be) not a driver of the economy.

After all, once a stock has been launched into the stock market, all that happens when a stock moves up and down is that money flows from one set of trading accounts to some others as people buy and sell. By buying equities, the BOJ has effectively said it wishes transfer an even greater amount of money from its accounts to others.

It's merely a gift to current holders of Japanese equities, which is a subset of the Japan population. Again not a terribly defensible, rational or fair policy. But there you have it.

Immediately on the news of this next round of wealth transfers and money printing, the Nikkei index leapt 1700 points and the yen plunged:

(Source - ZH)

The virtual lockstep nature of the falling yen and rising Nikkei tell us that we are living in an age of massive and rampant speculation where financial markets react in concert to the newly-unleashed liquidity floods.

All that matters in today's "markets" is how much more money the central banks are going to throw into the system. That's all the gigantic speculators care about, and fundamentals and long-range issues are not even remotely near the top of their list of important trading variables.

Unfortunately, like most market moves these days, the recent plunge in the yen and the rise in the Nikkei provide few useful clues as to Japan's actual current and/or future economic prospects.

What This Really Means

Okay, it's time to face some unpleasant facts. Ignoring the market gyrations because those have pretty much lost all of their true signaling capabilities, the most recent move by BOJ governor Kuroda smacks of sheer desperation.

It's important for all of us frogs sitting in this nice pot to recall that even five years ago such a move by the BOJ would have been utterly shocking. It would have commanded our thoughts and actions for weeks to come. But today, like the rest of the world, I'll bet you've already lost it into the din of other accelerating events barely a week later.

That Kuroda, just one man, can bet so much on an untested and radical experiment is mind-boggling. If he succeeds, he gets to claim honor and success. If he fails he ruins the 3rd largest sovereign economy in the world, along with its inhabitants' future dreams, for a very long time. How can such power be entrusted to a single person?

Unfortunately, this gamble cannot succeed over the long haul, and he has to know this. So perhaps he's simply focused on keeping things hanging together until he leaves office.

Here's how the ever-colorful David Stockman described the Halloween Massacre:

This is just plain sick. Hardly a day after the greatest central bank fraudster of all time, Maestro Greenspan, confessed that QE has not helped the main street economy and jobs, the lunatics at the BOJ flat-out jumped the monetary shark. Even then, the madman Kuroda pulled off his incendiary maneuver by a bare 5-4 vote. Apparently the dissenters——Messrs. Morimoto, Ishida, Sato and Kiuchi—-are only semi-mad.

Never mind that the BOJ will now escalate its bond purchase rate to $750 billion per year—-a figure so astonishingly large that it would amount to nearly $3 trillion per year if applied to a US scale GDP. And that comes on top of a central bank balance sheet which had previously exploded to nearly 50% of Japan’s national income or more than double the already mind-boggling US ratio of 25%.

(Source)

Yes, my fellow frogs who share this increasingly warm bath with me, Kuroda's move is pure madness. The BOJ has jumped the monetary shark and we need to keep that firmly in view as we make our decisions about where all of this is headed, and how likely it is to create a future financial accident of global and unprecedented proportions.

Bloomberg's Willaim Pesek described it this way, and I think quite accurately:

Japan Creates World's Biggest Bond Bubble

Nov 4, 2014

In announcing that it will boost purchases of government bonds to a record annual pace of $709 billion, the central bank has just added further fuel to the most obvious bond bubble in modern history -- and helped create a fresh one on stocks. Once the laws of finance, and gravity, reassert themselves, Japan's debt market could crash in ways that make the 2008 collapse of Lehman Brothers look like a warm-up.

Worse, because Japan's interest-rate environment is so warped, investors won't have the usual warning signs of market distress. Even before Friday's bond-buying move, Japan had lost its last honest tool of price discovery.

When a nation that needs 16 digits in yen terms to express its national debt (it reached 1,000,000,000,000,000 yen in August 2013) sees benchmark yields falling, you've entered the financial Twilight Zone.

Good luck fairly pricing corporate, asset-backed or mortgage-backed securities.

(Source)

If I lived in Japan, I would, under no circumstances, ever keep my money in yen. If you live there, get out of yen as much as you possibly can. Your central bank has said it wants to destroy the yen and their actions confirm this so they are apparently quite serious about doing exactly that.

Imagine if the Federal Reserve was monetizing $3 trillion a year, which pencils out to some $250 billion a month(!). A proportional amount of money is being dumped into the Japanese financial system under the new policy.

And so naturally, stocks rose and the yen fell, which makes some (twisted) sense. But gold fell heavily on the news, which makes no sense at all from a fundamental standpoint. However, it makes all the sense in the world if you understand that extreme central bank policies cannot tolerate even the slightest whiff of challenge.

Rising gold prices would signal doubts about the central banks' course of action. Conversely a falling gold price signals utter faith in the central planners. And so a falling gold price is what we get (but true demand for gold and silver demand another matter entirely).

The reason for all of this extreme central bank panicking and fear, we're told, is because Kuroda has a white whale he seeks, which has '2% inflation' stenciled on its side.

But inflation is not what central banks actually seek, even though the press consistently tells us that's what they want. Inflation is not a cure for anything and the banks know it (and our press really should know it by now, too).

Instead what the central banks desperately want, and know the banking system and over-extended governments need, is negative real interest rates. That is, they want to force upon savers the condition where their saved money is getting a lower rate of interest than the rate of inflation, which is what we mean by a negative real return.

We wrote about this extensively as a process in this article about the Fed purposely attacking savers. But the mechanism and rationale is the very same for the BOJ as it is for the Fed..

Briefly, when running this program of financial repression the BOJ (and the Fed, et al.) do not care if inflation is 6% and bonds are 4%, or if inflation is 2% and bonds are 0%, as both offer negative real interest rates. Negative real rates serve to confiscate purchasing power from the general population and transfer it to other parties. Those parties include the big banks. But perhaps that's just another happy coincidence in the game that central banks and bankers like to play with us which they call 'heads we win, tails you lose.'

But let's not be fooled. By the time a central bank Is behaving as recklessly as Japan, it's time to edge towards the exit, because the chance of a flash fire in the building has grown uncomfortably high. That is, instead of providing comfort, these most recent moves should invoke greater worry for those of us alert enough to see them for what they are: acts of panic.

There's just no other way to interpret the equivalent of $3 trillion of thin-air money besides an overt act of desperation. No, things are not okay. Yes, the risks for a disaster are growing.

Whether we call this the largest bond bubble in history, "reckless", "mad" or "insane", Japan has truly jumped the monetary shark. There's no way back and no way forwards that will be pain-free and this terrifies the BOJ. The best advice I have is that when you see your central bank panic, you should panic too and avoid the rush.

In Part 2: What Will Happen When Japan Breaks, we delve into the only questions that really matter: When will it happen? And how deeply painful will it be?

And last, but certainly not least: How much of the rest of the world's financial system will come crashing down with Japan's because they are all so interlinked now?

Click here to access Part 2 of this report (free executive summary; enrollment required for full access)

This is a companion discussion topic for the original entry at https://peakprosperity.com/central-planners-are-in-a-state-of-panic/