There are large signs of stress now present in the credit markets. You might not know it from today's multi-generationally low interest rates, but other key measures such as liquidity and volatility are flashing worrying signs.

Look, we all know that this centrally planned experiment forcing financial assets ever higher is simply fostering multiple bubbles, each in search of a pin. As all bubbles do, they are going to end with bang.

I keep my eyes on the credit markets because that’s where the real trouble is brewing.

Today’s markets are so distorted that you can reasonably argue that there’s not much in the way of useful signals emanating from them. And I wouldn’t put up too much of a counter-argument. But it's my contention that the bond market is the place to watch as it will provide the most useful clues that a reckoning has begun. And when these markets eventually return to earth, there will be blood in the streets.

While some may hope that rising yields are signaling a return to more rapid economic growth, or at least that the fear of outright deflation has lessened, the more likely explanation is that something is wrong and it’s about to get... wronger.

Rising Yields

Let’s begin with the first canary in this story, rising yields. The yield of a bond, expressed as a rate of interest, moves oppositely to its price. The higher the price goes, the lower the yield goes. The lower the price, the higher the yield. Imagine the relationship like a playground see-saw.

Over these past few weeks and months, we’ve seen yields moving up quite a lot across a wide variety of bonds, at least in terms of the percentage size of the move (yes, the yields are still historically low by any measure).

Again, not everybody thinks this is ominous. Some think it’s a healthy sign that growth, as well as a "healthy" return to inflation, is on the way:

Interest rate climb brings out optimists

Jun 16, 2015

WASHINGTON — Consumers, businesses and investors are facing an era of higher borrowing costs as some of the lowest global interest rates in modern history begin to rise.

Yet the message from most economists is a reassuring one: Rates won't likely climb fast or high enough to inflict much damage on economic recoveries in the United States or Europe.

Part of the reason for the optimism is that rising rates are a healthy sign: They mean that U.S. and European economies are strengthening, people are spending, companies are hiring and prices are starting to rise at more normal rates. The risk of too-low inflation — which typically slows spending and makes loan repayments costlier — has receded.

(Source)

However it’s not entirely clear that these rising rates have anything to do with better economic prospects or higher inflation.

Why? The world’s markets have been primarily driven by liquidity flows. The headwaters of that river are the easy money policies of the world’s central banks. From there, the river picks up steam as corporations issue debt to buy back their shares. Adding gasoline to the fire, margin loans are extended, and speculators lever up to chase assets world-wide.

Add it all up, and fundamentals don't really matter at times like these. The huge flood of money and credit swamps everything.

Which means that the signals themselves become the news. And at this time, the direction of the tide of this money/credit flow is the signal that matters most.

And what is it telling us. That money is now beginning to move out of the credit markets. This is a huge development.

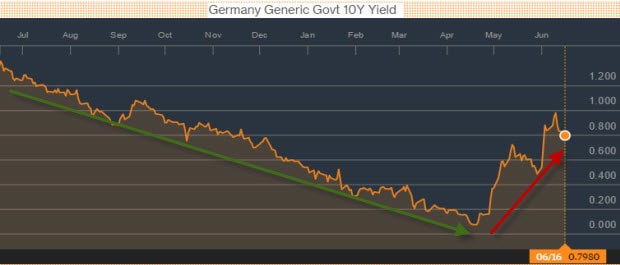

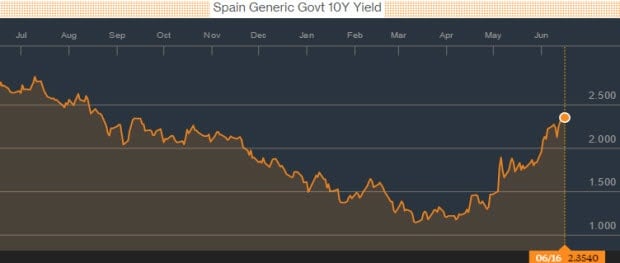

Take a look at these following charts of German, Spanish, Italian, Portuguese, and US sovereign debt yields. Note that the yields have risen despite the beginning of the recent QE program in Europe. They are back to where they were in November 2014, and have risen by more than 100% from the lows in many cases:

There are a competing variety of explanations for these yield hikes, but since they are occurring across numerous countries -- and in the corporate and junk bond markets as well -- it suggests that instead of any particular economic or fundamental explanation, liquidity is being pulled out of bonds generally.

And why not? After years of bonds going straight up in price courtesy of central bank interventions, bonds have become a massive bubble. Perhaps enough buyers have finally realized that it's time to start selling before things get ugly.

One immediate impact will be on mortgage rates, which have finally ticked back above 4% recently:

Mortgage Rates Top 4% in Test for Housing

Jun 11, 2015

Mortgage rates vaulted above 4% for the first time this year, posing a challenge to the housing market’s strengthening recovery.

For the week ended Thursday, the average rate of a 30-year, fixed-rate mortgage rose to 4.04% from 3.87% the previous week to the highest level since last October, according to mortgage-finance company Freddie Mac.

The increase followed a Treasury-market sell-off over the past week that drove yields higher on most kinds of bonds. Bond yields rise as prices fall.

[img] Mortgage over 4 percent WSJ

(Source)

Of course this will have an impact on real estate, but probably not too much yet. In the immediate term, sales volumes will cool as people wait for rates to ‘get back into the threes’ before taking on a mortgage.

Stocks Are For Show, But Bonds Are For Dough

All told, since the March highs in bond prices some $625 billion has been wiped off of the global sovereign bond index. That is a lot of vaporized capital. And rates are still incredibly low. Imagine how much more could be lost if rates were to march back up to their historical averages.

The conclusion here is that you should keep your eyes firmly on the bond markets because they will signal for us that a change in trend has occurred well before the equity markets will. These rising yields should have your full attention.

The reason we care is because when the bond markets finally turn, all of the grotesque market distortions induced by the central banks are going to snap violently. The process will be fast, chaotic and exceptionally destructive for everyone who is not prepared.

Agreeing with this view is a former Fed staffer who went public this week with similar concerns:

Former adviser to Dallas Fed's Dick Fisher, Danielle DiMartino Booth speaking in a CNBC interview slams The Fed for "allowing the [market] tail to wag the [monetary policy] dog," warning that "The Fed's credibility itself is at stake... they have backed themselves into a very tight corner... the tightest ever." As she writes in her first Op-Ed, "The hope today is that the current era of easy monetary policy will have no deep economic ramifications. Such thinking, though, may prove to be naive... All retirees’ security is thus at risk when the massive overvaluation in fixed income and equity markets eventually rights itself."

(Source)

I’ll go further and say it is not just retirees' security that is at stake, but much more than that. Our financial markets may simply stop working when this "mother of all bubbles" -- comprising both equities and bonds -- finally bursts.

Given the much greater size of money and credit that will be desperate to find an exit, and the lack of remaining options the central bankers have now versus then, the 2008 crisis may look tame in comparison.

In Part 2: The Warning Indicators To Watch For Trouble In The Bond Market we examine the key factors that will signal the kind breakdown in bonds that could cause a chain-reaction conflagration across all financial markets.

After 90 months of risk-free money inflows courtesy of the world's central banks, all the major market players are addicted and dependent on that ever-rising tide. What will happen when that tide reverses (and likely, all at once)? It's looking like we may be about to find out.

Click here to read Part 2 of this report (free executive summary, enrollment required for full access)

This is a companion discussion topic for the original entry at https://peakprosperity.com/credit-market-warning/