Back in my June report Less Than Zero: How The Fed Killed Saving, I explained how the Federal Reserve's policy of holding interest rates at record lows has decimated savers. Those who simply want to park money somewhere "safe" can't do so without losing money in real terms.

How bad is it?

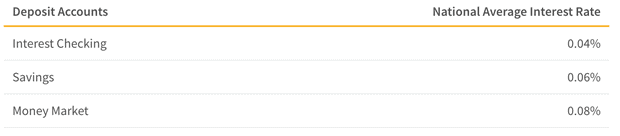

As this table shows, the average bank savings account today pays a paltry 0.06% interest rate to depositors:

(Source)

That's virtually the same as getting paid 0%. But it's actually worse than that, because once you take inflation into account, the real return on your savings is markedly negative.

As I ranted back in June:

0.06%.

Not 0.6%. And definitely not the 6% I remember receiving when I was a teenager. 0.06%.

As in, put $100,000 into your savings account and get back a whopping $60 per year.

Are you kidding me? $60 to have a hundred grand parked in an account subject to withdrawal restrictions and penalties, along with the usual smattering of administrative fees both overt and hidden? At a bank that stumbled mightily during the Great Financial Crisis? One with the potential to legally confiscate your savings through a "bail in" should another crisis hit?

Oh, and if you factor in the government's trailing 12-month inflation rate of 2.2%, your "savings" account has a negative (-2.14%) real rate of return. Your compounded savings actually loses purchasing power over time. And as we all know the official inflation rate is farcically understated, your loss of purchasing power is even more dire than it at first appears.

And to get your blood boiling further, when your local TBTF bank stores its own money at the Fed, the Fed pays it over a full 1% in interest -- that's 20 times what your bank is paying you. Your bank simply pockets the rest as pure risk-free profit. (Don't believe it? Watch Chris explain in this video).

//fred.stlouisfed.org/graph/graph-landing.php?g=fC7B&width=670&height=475

As usual, the banks get a sweet deal while the people they purport to serve get screwed.

If You Can't Beat 'Em, Join 'Em

As we've written about often at PeakProsperity.com, the Fed's chronic super-low interest rate policy is part of a deliberate policy playbook that economists call Financial Repression. Rock-bottom interest rates serve two important goals of the central planners: they sustain the government's debt orgy while making the elites filthy rich in the process.

The bad news here is that The Powers That Be are going to continue to pursue financial repression at all costs, for as long as possible. They have both too much to gain and too much to lose to do otherwise. The war on savers is not going to let up.

But there's also a little good news buried here, too. Individual investors savvy enough to understand the game being played can bend some of its rules to their favor and limit the damage they suffer a bit.

One of them enables you to get 16x more interest on your cash savings than your bank will pay you. With no additional risk (and perhaps even reducing risk).

TreasuryDirect

For those not already familiar with it, TreasuryDirect is a service offered by the United States Department of the Treasury that allows individual investors to purchase Treasury securities such as T-Bills, notes and bonds directly from the U.S. government.

You purchase these Treasury securities by linking a TreasuryDirect account to your personal bank account. Once linked, you use your cash savings to purchase T-bills, etc from the US Treasury. When the Treasury securities you've purchased mature or are sold, the proceeds are deposited back into your bank account.

So why buy Treasuries rather than keep your cash savings in a bank? Two main reasons:

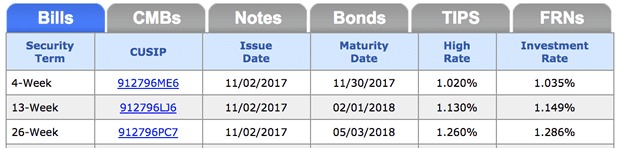

- Much higher return: T-Bills are currently offering an annualized return rate of over 1%. Notes and bonds, depending on their duration, are currently offering between 1.5% - 2.75%

- Extremely low risk: Your bank can change the interest rate on your savings account at any time -- with Treasurys, your rate of return is locked in at purchase. Funds in a bank are subject to risks such as a bank bail-in or the insolvency of the FDIC depositor protection program -- while at TreasuryDirect, your funds are being held with the US Treasury, the institution with the lowest default risk in the country for reasons I'll explain more in a moment.

Let's look at a quick example. If you parked $100,000 in the average bank savings account for a full year, you would earn $60 in interest. Let's compare this to the current lowest-yielding TreasuryDirect option: continuously rolling that same $100,000 into 4-week T-Bills for a year:

- Day 1: Funds are transferred from your bank account to TreasuryDirect to purchase $100,000 face value of 4-week T-Bills at auction yielding 1.035%

- Day 28: the T-Bills mature and the Treasury holds the full $100,000 proceeds in your TreasuryDirect account. Since you've set up the auto-reinvestment option, TreasuryDirect then purchases another $100,000 face value of 4-week T-Bills at the next auction.

- Days 29-364: the process repeats every 4 weeks

- Day 365: assuming the average yield for T-Bills remained at 1.035%, you will have received $1,035 in interest in total throughout the year from the US Treasury.

$1,035 vs $60. That's a 16.25x difference in return.

And the comparison only improves if you decide to purchase longer duration (13-week or 26-week) bills instead of the 4-week ones:

Repeating the above example for a year using 13-week bills would yield $1,149. Using 26-week bills would yield $1,286. A lot better than $60.

Opportunity Cost & Default Risk

So what are the downsides to using TreasuryDirect? There aren't many.

The biggest one is opportunity cost. While your money is being held in a T-Bill, it's tied up at the US Treasury. If you suddenly need access to those funds, you have to wait until the bill matures.

But T-Bill durations are short. 4 weeks is not a lot of time to have to wait. (If you think the probability is high you may to need to pull money out of savings sooner than that, you shouldn't be considering the TreasuryDirect program.)

Other than that, TreasuryDirect offers an appealing reduction in risk.

If your bank suddenly closes due to a failure, any funds invested in TreasuryDirect are not in your bank account, so are not subject to being confiscated in a bail-in.

Instead, your money is held as a T-Bill, note or bond, which is essentially an obligation of the US Treasury to pay you in full for the face amount. The US Treasury is the single last entity in the country (and quite possibly, the world) that will ever default on its obligations. Why? Because Treasurys are the mechanism by which money is created in the US. Chapter 8 from The Crash Course explains:

As a result, to preserve its ability to print the money it needs to function, the US government will bring its full force and backing to bear in order to ensure confidence in the market for Treasurys.

Meaning: the US government won't squelch on paying you back the money you lent it. If required, it will just print the money it needs to repay you.

So, How To Get Started?

Usage of TreasuryDirect is quite low among investors today. Many are unaware of the program. Others simply haven't tried it out.

And let's be real: it's crazy that we live in a world where a 1% return now qualifies as an exceptionally high yield on savings. A lot of folks just can't get motivated to take action by a single percentage point. But that doesn't mean that they shouldn't -- money left on the table is money forfeited.

So, if you're interested in learning more about the TreasuryDirect program, start by visiting their website. Like everything operated by the government, it's pretty 'no frills'; but their FAQ page addresses investors' most common questions.

Before you decide whether or not to fund an account there, be sure to discuss the decision with your professional financial advisor to make sure it fits well with your personal financial situation and goals. (If you're having difficulty finding a good one, consider scheduling a free discussion with PeakProsperity.com's endorsed financial advisor -- who has considerable experience managing TreasuryDirect purchases for many of its clients).

In Part 2: A Primer On How To Use TreasuryDirect, we lay out the step-by-step process for opening, funding and transacting within a TreasuryDirect account. We've created it to be a helpful resource for those self-directed individuals potentially interested in increasing their return on their cash savings in this manner.

Yes, we savers are getting completely abused by our government's policies. So there's some poetic justice in using the government's own financing instruments to slightly lessen the sting of the whip.

Click here to read Part 2 of this report (free executive summary, enrollment required for full access)

NOTE: PeakProsperity.com does not have any business relationship with the TreasuryDirect program. Nor is anything in the article above to be taken as an offer of personal financial advice. As mentioned, discuss any decision to participate in TreasuryDirect with your professional financial advisor before taking action.

This is a companion discussion topic for the original entry at https://peakprosperity.com/earn-more-on-your-cash-savings-with-less-risk/