Originally published at: https://peakprosperity.com/energy-shocks-and-inflation-vs-market-complacency-which-is-stronger/

In this episode of Finance U, Paul Kiker and I once again note how the current US equity markets ‘feel’ like they did in February 2020 when they were studiously ignoring Covid. Whereas in times past, equity markets were both discounting machines and a source of early warnings about future events, they have somehow become lobotomized.

Placid, dull, and reactive, not forward-looking.

The core takeaways: A truly unprecedented energy-supply destruction event is underway; an inflationary is “in the pipeline,” yet paper markets remain distorted. Prudent preparation in the forms of portfolio risk management and physical resilience are called for over passive buy-and-hold and ‘eyes wide closed’ approaches.

The Energy Shock

With oil and NG, and an entire circus of downstream related products such as fertilizer and ethylene, suddenly missing from the global economy, the world has never experienced a shock of this magnitude.

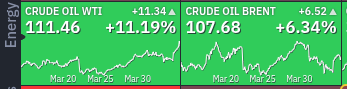

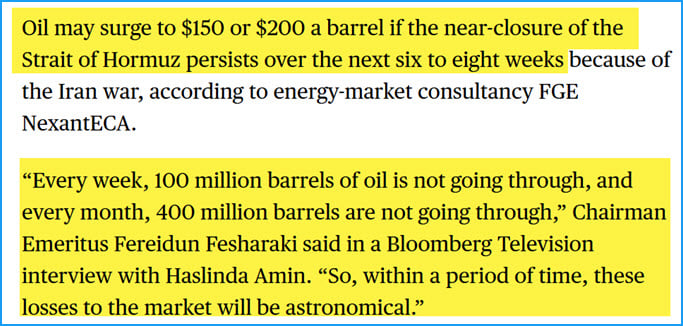

The Strait of Hormuz near-closure, plus Russian export losses, has already removed ~12 million barrels/day of crude/condensate, which is 35% of global exportable oil (a more important number than it being 20% of global daily supply).

If oil prices weren’t being actively suppressed in the paper futures markets by US and possibly Japan (as rumored), they would certainly be far higher. When the snap-back happens, the explosive rise in oil prices will shock the overly complacent markets.

Even if the war suddenly ended, repairing all the damage and sorting out all the supply shocks will take years, up to 5 years in the case of LNG exports from Qatar.

Inflation and Demand Destruction

Jet fuel shortages and price hikes have already forced thousands of flight cancellations, the grounding of 20 Lufthansa jets, emergency shipping surcharges (e.g., Maersk’s emergency bunker fees), and fertilizer and chemical shortages.

Demand destruction is already confirmed in the form of canceled flights, idled fleets, and spreading work-from-home mandates.

Europe, many Asian countries, and Australia are already experiencing severe diesel shortages with unpredictable (but observable) impacts on economic activity.

Petrodollar & Treasury Risks

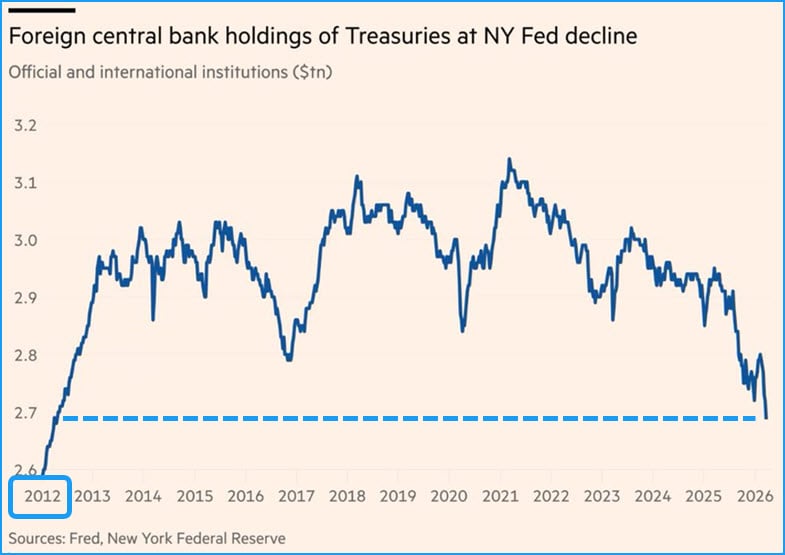

Foreign central banks have reduced NY Fed Treasury holdings by ~$100B, back to 2012 levels, despite U.S. debt having doubled over that time frame.

If more foreign holders (beyond central banks) also cut their exposure to US Treasuries, that will put upward pressure on interest rates…and a particularly awkward time for the US government, which was already running a massive deficit before the war against Iran.

Iran is quite provocatively – at least to the existing world order – linking Hormuz transit fees to the Chinese yuan, accelerating both sides of the petrodollar equation; the linking of Gulf oil purchases to the dollar as well as the round-trip reinvestment of those dollars back into US markets.

To call this a profound shift is to understate it severely.

It is against this backdrop that US equity markets remain “priced for perfection” while risks (energy shock, inflation, fiscal irresponsibility) continue to mount daily.

Again, this is a time for prudence and caution, two things which passive investing strategies completely ignore.

If you’ve been thinking, “I may give Paul Kiker and his team a call someday,” don’t put it off any longer. We all need help navigating these turbulent times, and at a minimum, you’ll come away with a sharpened understanding of your financial position and options.

Timestamps

00:30 Market Manipulation and Oil Prices

14:51 The Inflationary Beast

30:01 Energy Supply Crisis and Economic Impact

35:17 The Complexity of Oil Production

39:03 Inflationary Pressures and Market Dynamics

43:41 Global Supply Shocks and Food Inflation

45:42 Foreign Investment in US Treasuries

50:45 Understanding Market Risks and Valuations

01:05:20 Historical Lessons and Future Strategies

FINANCIAL DISCLAIMER:

The information contained in this video and the resources available for download through our affiliated website are not intended as and shall not be understood or construed as financial advice, nor should be interpreted as a solicitation to sell or offer to sell investment advisory services. No person who currently works for or contracts with Peak Prosperity or Peak Financial Investing is an attorney or accountant, nor are we holding ourselves out to be, and the information contained in the video and on the website is not a substitute for legal or tax advice from a professional who is aware of the facts and circumstances of your individual situation. While Peak Financial Investing is a registered investment advisor, please note that this podcast is not intended to be investment advice.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. We have done our best to ensure that the information provided is accurate and provides what we feel is valuable information. The views expressed are subject to change based on market and other conditions.<

No guests or clients appearing on the podcast receive any form of compensation for their appearance and obtained no other benefit from either Peak Prosperity or Peak Financial Investing.

All investing involves risks including the possible loss of capital. Asset allocation and diversification does not ensure a profit or protect against loss. Please note that out- performance does not necessarily represent positive total returns for a period. There is no assurance that any investment strategy will be successful. All investments carry a certain degree of risk. Dividends are not guaranteed, and a company’s future ability to pay dividends may be limited.

Additional important disclosures for Peak Financial Investing may be found in our Form ADV Part 2A, which can be found at https://adviserinfo.sec.gov/firm/summary/319672.