With the Eurozone having being displaced from the financial headlines by the American presidential election, you might have briefly thought that its problems had gone away. They haven’t.

It’s just that the public is expected to absorb one major story at a time. And now that the presidential election is done and dusted, Europe is rapidly returning to the headlines. This is not desired by the powers-that-be, who desperately need us to believe things will get better with a little patience.

Behind the scenes, in order to prevent a systemic crisis, the authorities (through the European Central Bank) have been hard at work keeping a lid on interest rates for Spain and Italy, which act as everyone’s market bellweather. Their strategy focuses on the hope that high bond yields are just a lack of 'animal spirits' – and if only they can be reignited!

Time is working against all countries in the Eurozone because the good are being dragged down by the bad.

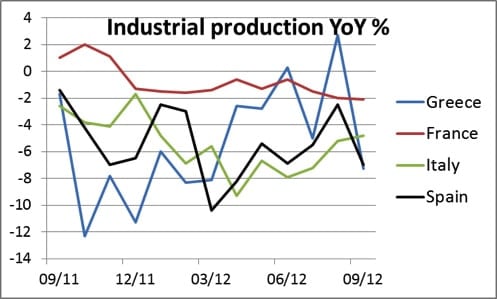

You don’t have to be an economic genius to understand that the perpetual uncertainty over the Eurozone’s future has led to a widespread freeze on industrial investment and development. Industrial production is collapsing at an accelerating rate, falling 7% year-on-year in Spain and Greece, 4.8% in Italy, and 2.1% in France. The downtrends for industrial production are readily apparent in the chart below:

The businesses that are doing well (and there are some) are those businesses with strong balance sheets and solid export order books for non-Eurozone markets; unfortunately, they are concentrated in countries like Germany, Holland, Finland, and Austria. They are not located where they can contribute to economic progress in Spain, Italy, Greece, or France, and so they are not adding to the tax revenue desperately sought by those governments.

Despite the recent deal worked out with Greece, the old cliché about kicking the can down the road is close to becoming no longer possible. Deferring the inevitable is only a political option so long as there is no immediate damage from doing so. But this is no longer true in the Eurozone, where political procrastination is now identifiably responsible for social unrest. It’s not just the trade unionists in revolt; now it is the middle classes as well. Doctors and teachers in Greece do not get paid anymore, and it is going that way in Spain, with regional governments surviving by simply not paying their bills. Government is destroying society, proving the falsity of the heretofore accepted belief (in Europe, anyway) that government makes society better. But then, anyone who has bothered to read Hayek’s The Road to Serfdom will not be surprised.

What was not anticipated in Hayek’s masterpiece is the divided state that is emerging. Greece is part of a larger EU and Eurozone bureaucracy and cannot achieve statist ends by turning her citizens into serfs. The government itself is subservient to higher authorities and is now having that medicine applied to it by its peers. Every visit by the Troika (collectively the European Central Bank (ECB), International Monetary Fund (IMF), and the European Commission) screws the Greek government further towards its own serfdom.

Keep in mind just one thing: Greece is utterly broke and cannot escape that fact. All of the posturing by the three Troika members is designed to avoid facing this reality. The political elite drive this party line and rigidly conform to it. However, there is increasing unease among powerful elements in the background, and in particular, sound money advocates in the Bundesbank are deliberately pushing for different solutions than those pursued to date.

Jens Weidmann, who is the Bundesbank’s chief and its representative on the ECB’s Governing Council, is remarkably outspoken on this issue. In a recent interview with the Rheinishe Post, Weidmann pointed out that the ECB and other national central banks in the Eurozone are now Greece’s largest creditors and cannot take a haircut on Greek debt. Furthermore, they cannot write off this debt, since that would amount to monetary financing, which is forbidden under Eurozone rules. So, he concludes, the ECB is trapped.

This intervention is important, because – unusual among the world’s central banks – the Bundesbank is viewed by the German public as the protector of the currency against the politicians. The German economy is traditionally driven by small savers, who are secure in the knowledge that the Bundesbank won’t let them down by printing money. While this is perhaps a stereotypical view, a hangover from the days of the deutschemark, it is still true with respect to public attitudes. And this is important because there is greater public trust in the head of the Bundesbank, Jens Weidmann, than in any politician, including Chancellor Merkel. We must listen to Weidmann, not Merkel.

Returning to Greece, forward-looking markets have already written it off, but getting there is not easy. On 11 November, by a slender majority, the Greek Parliament agreed to the latest austerity demands from the Troika, in the belief that the Troika will come up with urgently needed cash. This is cash for an economy that is tanking with its industrial production collapsing. Deposits have flown from the banks, which, without the ECB’s recycling of funds both through the TARGET2 settlement system and by taking in yet more worthless Greek debt as collateral, would themselves default. Tax revenues, insofar as they can be collected, are simply vaporizing. In the words of the classic Monty Python sketch, this parrot is dead, expired, and everyone knows it. Despite this, the Troika caved in (to ironic laughter from the press) on 13 November by giving Greece a further two years to get its government debt to GDP under 120%.

The concern, obviously, is that Greece is a dry run for Spain and Italy. It is also, as I argue below, a dry run for France, which is in terrible shape and deteriorating rapidly. This is why the protector of German savers, Herr Weidmann, is worried. He is signalling that the precedents set in dealing with Greece will ultimately destroy Germany.

In my last article for PeakProsperity.com, I argued that Germany, not Greece, should and will leave the Eurozone, perhaps taking Holland, Finland, Luxembourg, and Austria with her. It has always been clear that this is the last thing the political elite would consider, but unless Mrs Merkel reconsiders her position, she will be overruled by the Bundesbank, and perhaps also her own finance minister, Wolfgang Schäuble, who is known to be extremely concerned.

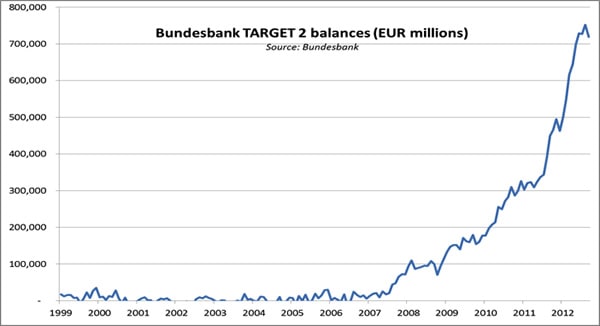

Anyway, let me throw in a little ray of sunlight for Germany (or is this the light an oncoming train in the tunnel?) For some reason that's not entirely clear, the outstanding TARGET2 claims by the Bundesbank on the other Eurozone national banks actually fell in October. The updated chart is below:

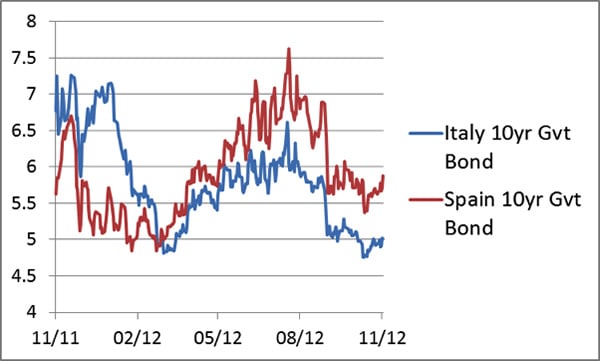

That's the good news. The bad news is that the previous down-tick (in December 2011) was in the wake of a drop in Spanish bond yields from over 7% in mid-2011 to a low of under 5% last January. This time, Spanish yields fell from 7.5% three and a half months ago to 5.4% a month ago. Italian government bonds have followed a similar pattern, as shown in the chart below:

It is perhaps logical to link changes in TARGET2 balances with changes in sentiment in Spanish and Italian bonds. These bond yields show signs of bottoming out, which is clearly visible on the chart. The only reason these bond yields have fallen to these low levels is because the ECB forced them there. But when these yields rise, which they probably will because there is little doubt the ECB’s manipulation cannot succeed for very long, the accumulation of TARGET2 imbalances on the Bundesbank’s book will quickly exceed €1 trillion.

And there is a further problem. One of the reasons French ten-year government bond yields are only 2.1%, and have even been briefly negative for her six-month bills, is that some of the capital flight out of Spain and Italy has been deposited in French banks, only to be then lent on to the French government.

But France, as I argue later in Part II of this article, is itself a basket case, only not yet widely recognised as such because it has benefited from this capital flight from Spain and Italy.

At some stage, probably in the next six months, these accumulated deposits in the French banks will, in turn, seek a safer home elsewhere – and where else but in the German banks? And so the Bundesbank faces the prospect of a second wave of capital flight and escalating TARGET2 imbalances.

Of course, this would not matter if it was certain that no one was leaving the Eurozone, and the TARGET2 system was constructed on the assumption that no one ever would. One could argue that Greece leaving would not be too much of a problem, other than the precedent it would create. This is why it is so important to keep Spain and Italy in the system.

In Part II: Europe's Mexican Standoff we explain why the answer to the question of Who will ultimately pick up the tab? when a Eurozone member leaves is not at all clear. In fact, the "stability" of Europe right now hinges completely on no one leaving (or defaulting).

After all, TARGET2 is a settlement system with offsetting cash creation and destruction carried out by the national central banks on delegation from the ECB. But nonetheless, it is understandable that the sound-money guardians at the Bundesbank are increasingly alarmed at the progression of events.

To borrow from Dirty Harry, it leaves those tied to Europe's future pondering a seminal question: "Do I feel lucky?" Well, do ya?

Click here to read Part II of this report (free executive summary; paid enrollment required for full access).

This is a companion discussion topic for the original entry at https://peakprosperity.com/europe-is-now-sinking-fast/