Crying Wolf?

It is easy to get the impression that the naysayers are wrong about Europe. After all of the predictions of Armageddon, ten-year government bond yields for Spain and Italy fell to the 4% level, France (which is retreating into old-fashioned socialism) was able to borrow at about 2%, and one of the best-performing bond investments has been until recently – wait for it – Greek government bonds! Admittedly, bond yields have risen from those lows, but so have they everywhere. It is clear, when one stands back from all the usual euro-rhetoric, that, as a threat to the global financial system, it is a case of "panic over."

Well, no. The decline in government bond yields for the troubled nations in the Eurozone was and still is a reflection of the ability of the European Central Bank (ECB) to manipulate markets and expectations. There has been some behind-the-scenes help from the Fed, which has helped foreign banks, mostly European, to the tune of over $700 billion of easy money since 2009.

The ECB has basically managed to talk yields down, and here it had some unexpected and temporary luck from Japan. Since Japan declared a policy of printing huge amounts of yen to get the currency down, global hot money was given a seemingly guaranteed profit by borrowing depreciating yen at negligible cost, buying euros, and investing in Eurozone debt. Since the introduction of Japan’s new monetary policy, Eurozone debt yields took a shift down, spreading happiness and joy to beleaguered Eurozone governments. That honeymoon was short-lived, as the fallacies behind Abenomics dawned on markets, and Japan’s latest export became monetary and financial instability.

And if you are a European insurance fund, pension fund, or bank wondering what to do with your liquidity, you probably took the view that falling yields on Italian debt, for instance, was evidence of a return of confidence. Therefore, the dramatic fall in yields had more to do with the ECB skillfully rigging bond markets and in partnership with the Fed global money flows, rather than any underlying improvements. As a result, the can has been kicked down the road one more time, but the underlying problems are very much intact.

Meanwhile the ongoing slump in the periphery nations is now so bad that it is even being reflected in official statistics, which, as we should all know, are more fiction than fact. Spain’s economy, according to official statistics, contracted by only 0.5% annualised in the first quarter 2013, Italy’s by 0.5%, and France’s by 0.2%. Germany is the only significant Eurozone economy still growing, having chalked up a magnificent 0.1%. But, as we should all know, official figures are a mixture of spin and manipulated statistics.

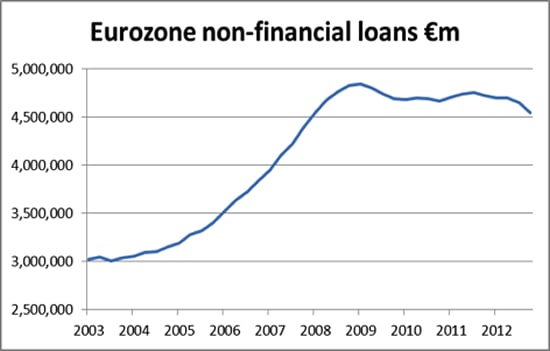

The fact is that, between unproductive government spending and high levels of unemployment, the Eurozone economy should be doing significantly worse than government statistics suggest. The difference between reality and government numbers can only be bridged by consumers drawing down their savings. However, figures from the ECB database also tell us that private sector borrowing fell over the period, so gross private sector savings must have been further reduced by the sum of the two. In other words the headline GDP statistic is masking a significant fall in the level of private sector savings, a fall that has accelerated from mid-2012 and which is a trend clearly picked up in the chart below. People are spending their savings to exist.

This analysis gives the lie to GDP statistics that complacently tell us that the whole Eurozone is contracting by less than 0.5%. It confirms and is in accordance with the hard evidence that unemployment is high – exceptionally high in the periphery countries.

Keynesians might argue that so long as people draw down on their savings to keep the rate of spending up it doesn’t matter, but there are two problems with that. Firstly, savings are being diverted from capital investment, starving the Eurozone economies of their long-term economic potential. And secondly, after a time, savings simply run out.

The effect on prices is a complex balance. The flight out of savings amounts to a preference for goods relative to money, which, other things being equal, would normally drive prices up. However, Eurozone inflation, including the recent fall in oil prices, was recorded at only 1.2% annualised in April, consistent with savings being drawn down to maintain essential spending at current levels rather than increasing it. This is fine so long as there are savings to draw upon, but this source of funding for everyday spending is at best a temporary fix. When it slows, GDP numbers will turn down, most probably rapidly, setting off alarm bells in the banks, central banks, and governments seeing tax revenues disappear.

The underlying situation is therefore very deflationary, which is bad for banks and bad for tax revenues. How do you stop it moving from being an underlying problem to coming out into the open?

The Keynesian solution is for the ECB to step up injections of credit and money, following policies instituted by the Bank of Japan. The alternative in black and white terms is the ECB throws in the towel and allows deflation to take its course. The latter is never going to be considered as a policy option, because ever since the 1930s depression, the establishment has had one over-riding priority: to prevent it happening ever again. Therefore, the ECB will seek to remove constraints on her ability to expand money supply.

This is the background to seemingly intractable problems in not just the small fry of Greece, Cyprus, Portugal, and Ireland, but also in Spain, Italy, and France. Things are not that rosy in the Netherlands, either, crippled by private sector debt, and Belgium, whose government debt-to-GDP is about 100%. The Eurozone’s central banks realise the seriousness of these dangers to the banking community, and they are aware that individual nations do not have the resources to stage a rescue when needed. This is why the European Parliament (which covers all 27 EU member states) is urgently considering how to legislate for the cost of bank rescues to be borne by uninsured depositors instead of taxpayers.

Depositor Discrimination

There is nothing new in this. It has been a topic under consideration since the publication by the Financial Stability Board (a BIS committee) of a paper, Key Attributes of Effective Resolution Regimes for Financial Institutions in October 2011, which was endorsed at the Cannes G20 summit the following month. This was followed by a consultative document in November 2012, Recovery and Resolution Planning: Making the Key Attributes Requirements Operational. In this latter document, it is stated in the introduction that “Reforms are now underway in many jurisdictions to align national resolution frameworks more closely with the Key Attributes” (i.e., the October 2011 paper). In other words, any changes to law to facilitate bail-ins have been or are being quietly made.

This confirms that all G20 members and anyone hanging on to their coat-tails are ensuring that they can legally favour some creditors over others, targeting uninsured depositors. This outcome is not difficult to achieve in practice when the alternative in almost all bank failures is for uninsured deposits to be wiped out completely. Governments have neatly extracted their liabilities to small depositors from the insolvency process. However, now that those who bear the cost will be decided by the relevant central bank, in a bank reconstruction it is more than likely that deposits by banks and other systemically important financial institutions will be given creditor priority as well as insured depositors, in the interest of stopping one insolvency from taking down other banks. So those depositors that do not fit in either of these categories will bear the whole burden of a financial reconstruction, after subordinated loan holders.

The first clumsy attempt to introduce this new regime was perpetrated on little Cyprus, and it won’t be the last. The implications are that any person or business with deposit balances in excess of the insured amount (generally €100,000 or about $130,000) anywhere in the Eurozone risks losing the excess.

Discrimination among bank creditors will probably spread to subordinated bondholders. It is proposed in Germany, for instance, that a bank rescue be facilitated by a good-bank/bad-bank regime, which will allow the authorities to select what gets transferred into the bad bank on both sides of the balance sheet. Subordinated bondholders are first in line to lose their rights to the good bank and be transferred to the bad. Further discrimination against private equity, hedge funds, sovereign wealth funds, and similar institutional investors and creditors cannot be ruled out, since they are commonly branded by politicians and the media as speculators and “locusts.”

The ECB and Germany’s Constitutional Court

The plaintiffs at the Karlsruhe court, who include German politicians, lawyers and ordinary citizens numbering some 35,000, claim that the ECB has created a risk over which German taxpayers and officials have no control, through an open-ended commitment to purchase government bonds in secondary markets with the express purpose of lowering bond yields. These purchases are known as outright monetary transactions, or OMTs.

The purchases of OMTs are conditional on the relevant Eurozone government’s request for this assistance and its agreement to the ECB’s terms. The ECB also made it clear that it would claw back the money supply created by OMTs through sterilisation “by any means necessary.” The amazing thing is that no country has yet requested OMT support, so the whole exercise has been no more than a successful bluff, a threat to any short-sellers of Italian or Spanish debt to stay clear.

There is no doubt that the OMT programme was constructed with a view to avoiding legal challenges, such as from the German Constitutional Court, whose 2-day hearings on this matter began on June 12th. The Court will now deliberate, and it is expected to delay its ruling until after the German election in September.

It seems unlikely that the German Constitutional Court will find against OMTs, though they may impose some conditionality. Anticipating this, the ECB is rumoured to be suggesting a limit on this unused facility. The most likely outcomes now are either to defer consideration until such time as it is used (How can the Court rule on something that does not yet exist?), or to kick the matter upstairs to the European Court of Justice, which is the superior court.

Meanwhile, the ECB led by Mario “whatever it takes” Draghi appears to have little more than hot air in its monetary tool chest. Given the acceleration of money-creation in Japan, the U.S., and potentially the UK under her new Bank Governor Mark Carney, the euro is likely to rise against the other major currencies. It will be an interesting summer, given the prospect of a rising euro and the effect on weaker Eurozone states. And it will be a challenge to German monetary orthodoxy, when the consequences are likely to be growing unemployment ahead of the German elections.

As Go the Banks Will Go the Rest of Europe

The rest of this analysis is devoted to the condition of selected banks in selected jurisdictions.

As analysts like Kyle Bass have been warning, Europe has not recapitalized its banking system the way the U.S. has (at great taxpayer expense, of course). Therefore, it is much more vulnerable. Where European governments and regulators have failed to make their banks more secure, it is because they tied their strategy to growth arising from an economic recovery that has failed to materialize. The reality is that the Eurozone GDP levels are only being supported at the moment by the consumption of savings; in other words, the consumption of personal wealth – wealth that is not infinite and is held by those not likely to tolerate footing the bill for much longer.

In Part II: Where Will the Minsky Moment Occur? we look at each major EU country and the (poor) health of its banking system. Which are most vulnerable? Which have the greatest likelihood to set off a conflagration that could burn down Europe's – and then the world's – financial system?

Time (and savings) is running out.

Click here to read Part II of this report (free executive summary; enrollment required for full access).

This is a companion discussion topic for the original entry at https://peakprosperity.com/europes-precarious-banks-will-determine-the-future/