The airwaves are full of stories of economic recovery. One trumpeted recently has been the rapid recovery in housing, at least as measured in prices.

The problem is: a good portion of the rebound in house prices in many markets has less to do with renewed optimism, new jobs, and rising wages, and more to do with big money investors fueled by the ultra-cheap money policies of the Fed.

On my recent trip to Salt Lake City Utah, after presenting to the conservative caucus in the capital building, a gentleman came up to me and introduced himself as a real estate agent. He explained that he'd been seeing something very strange over the past six months where very well-capitalized out-of-state private equity funds had been buying up huge swaths of residential real estate with cash. He wanted to know if I knew anything about this.

Of course I had been tracking this phenomenon for a while. But had not been aware that Salt Lake City had been one of the targets, so I asked him how the deals worked there. Apparently, the hedge funds make "full ask" price offers, sight unseen and without conditions (such as inspections and the like), for whole baskets of available properties, typically in the middle to lower price ranges.

The effect, not surprisingly, is that regular home buyers are being out bid and eventually priced out of the market. Over time, these full cash offers at the ask get noticed and home-sellers begin to raise their asking prices. For a young family saving to obtain the required 20% down, a 10% hike in price on a median house translates into an additional $3k - $4k that they must have to set aside to make the deal work (assuming they've not just been priced out of the house they wanted to buy).

The impact, he told me, is that a growing number of young families were finding themselves unable to obtain their first home.

They can thank Ben Bernanke for this. Here's why.

The Back Story

The housing propaganda machine has been turned on in full force as exemplified by this article in the WSJ which headlined the front page:

Home Sales Power Optimism

May 28, 2013

Home prices surged during the first quarter at their fastest pace in nearly seven years, the latest sign of a sustained warm-up in an economic recovery that has otherwise been marked by starts and stops.

The housing-market revival—and an accompanying report on consumer confidence—adds new grist for a debate inside the Federal Reserve about how far to push its easy-money policies, including an $85 billion-a-month bond-buying program which has helped to keep mortgage rates near historic lows, boosted asset prices and begun to stimulate hiring and spending.

Over the past year, the share of foreclosed property sales has fallen, particularly in California cities, Las Vegas, and Phoenix, which have posted the largest year-on-year price growth

The latest reports were big factors driving financial markets Tuesday. Stock investors, encouraged by the strong data, sent the Dow Jones Industrial Average to a new high.

There you have it. The rising house prices are being presented as a signal of a "sustained economic recovery" that feeds into consumer confidence and as reason to propel the stock market to new all-time highs. What's not to like in that narrative?

However, if you value context, the above article will leave you disappointed because it omits the main driver of house price gains in the areas mentioned: big, institutional money seeking rental income and future capital gains.

As the article noted:

Many of the largest home-price gains have come in the West, including many markets hit hardest by the foreclosure crisis.

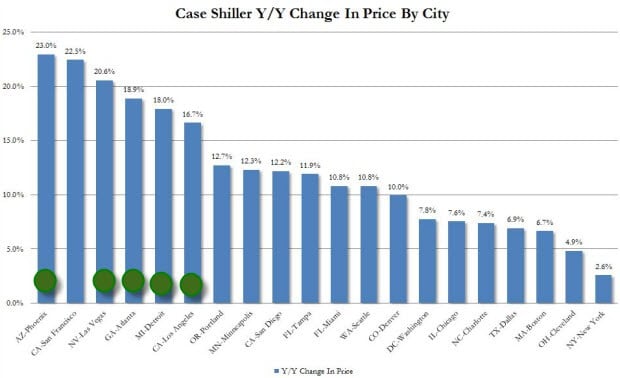

In March, prices were up by 22.5% in Phoenix from one year earlier, and by 22.2% in San Francisco. Other cities with double-digit gains included Las Vegas (20.6%); Atlanta (19.1%); Detroit (18.5%); Los Angeles (16.6%); Portland, Ore. (12.8%); Minneapolis (12.5%); San Diego (12.1%); Tampa, Fla. (11.8%); Miami (10.7%); and Seattle (10.6%).

The fact that big funds with big money have been very aggressive cash buyers in the formerly hardest hit markets is very well-documented and has been for well over a year. How such important context gets left entirely out of an article about house price appreciation in exactly those same markets is something of a mystery, at least from the standpoint of honest journalism.

Here's just one article out of many that have observed and reported on this issue:

Wall Street Institutions Behind Home Price Surges In Markets Like Phoenix

Mar 18, 2013

The March MarketPulse report from CoreLogic examines the rise of institutional investors and the effects they are having on distressed inventory. The analysis, compiled by CoreLogic deputy chief economist Sam Khater, looked at 16 major U.S. housing markets where bank-owned inventory (REOs) have been relatively high since the housing bubble burst.

He assessed whether local activity was comprised of mom-and-pop individual investors or institutional investors, defined as either entities that have purchased five-plus properties a year under the same name or under an incorporated name.

Here’s what Khater found: institutional investors have been targeting specific markets and then accelerating purchases of REOs in those markets, driving down distressed inventories and leading to notable increases in REO prices that have in turn led to larger market upticks.

Institutional investors have focused buying efforts strongly on south and southwestern cities that were hit hardest by the foreclosure crisis. The cities where investors activity has been particularly robust in the past year are Atlanta, Ga., Detroit, Mich., Las Vegas, Nev., Phoenix, Ariz., and Calif.’s Los Angeles, Riverside and Sacramento.

“In Q4 2012, Phoenix REO prices were 37% higher than a year ago, followed by Las Vegas (30%) and several California markets. All six markets with rising shares of institutional investors experienced double-digit increases and were among the top nine for REO price appreciation.

“More importantly, the ripple effects are greatly impacting the broader market. Lower-end home prices in markets with rising shares of institutional investors are up 15% from a year ago, compared to only 6% for the remaining markets.”

Institutions are most active in five states: Florida, Georgia, Arizona, Nevada and California. Interestingly the metro area that welcomed the most institutional activity in 2012 was Miami, Fla., with firms funding 30% of all sales. Single-family home prices for the Miami metro area rose about 11% in 2012 (including distressed homes), according to CoreLogic.

Institutional investors accounted for 21% of all sales in Charlotte, N.C., 19% in Las Vegas, and 18% in Orlando.

With up to 30% of all home sales in some markets going to funds, which have been notable for buying with cash at the asking price, it is not hard to conclude that the big funds are driving up prices.

A simple comparison of the Case-Schiller index which the media trumpeted as revealing that housing has recovered, with the list of areas where the big money funds have been most active shows (noted by green circles over the blue bars) the following:

That is, the places where the biggest price increases have been noted are the same places that giant institutional funds are buying up tens of thousands of properties at the ask.

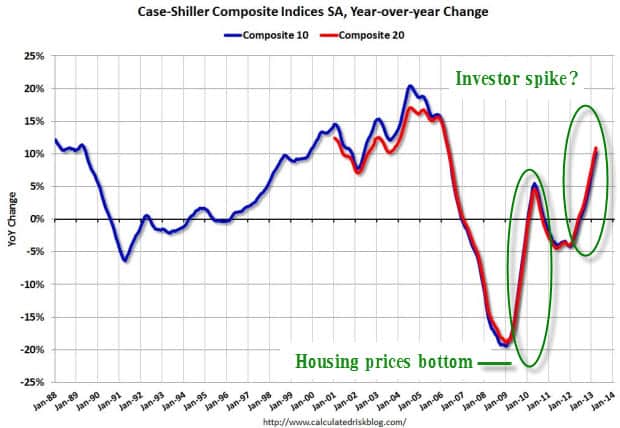

Where the first 'rebound' seen after a market correction is the prices of the asset merely stabilizing (because the yr/yr comparisons eventually head to zero), the most recent gains are definitely at levels that have been associated with bubbles and eventual corrections.

(Source)

Here are a few more article for context, each of which demonstrates the obvious impact of institutional money on various key housing markets:

Hedge funds crowd first-time buyers out of housing market

Dec 10, 2012

There are still a whole lot of foreclosed houses out there. You would think that means it's a great time for first-time buyers to purchase a house. But that's not the case: One reason, private equity firms are buying up huge numbers of single-family houses. Wall Street wants to turn them into rentals.

Jonathan Shidler is a realtor in California. Lately he gets at least one call every day from a hedge fund manager who wants to buy single-family houses in bulk.

He says they are buying them like a financial instrument, "which is fine and dandy. but what's different about these instruments is people live in them. You put your key in it and go inside. You get naked inside of it. So it makes it a little more personal."

Wall Street has been investing in residential housing for decades. What is new is the scale of these purchases. Hedge funds are buying thousands of single-family houses around the country, especially in states hardest hit by the housing crash, like California.

"This is a 1,200 square foot house with detached two-car garage, O'Rafferty said as he put a key into a ranch style home on a corner lot. The house he showed is what he calls "The gold standard of entry-level homes."

This is the type of home that hedge funds are snapping up. O'Rafferty put this house on the market on a Friday. By Monday he had 17 offers.

Those offers came from two types of buyers: Investors looking to turn a profit and families looking to get a piece of the American dream. These days O'Rafferty almost always sells to the investor.

Blackstone Buys Atlanta Homes in Largest Rental Trade

Apr 25, 2013

Blackstone Group LP (BX) bought 1,400 properties in Atlanta, some eligible for federal low-income housing subsidies, in the biggest bulk purchase for the fledgling homes-for-lease industry.

The private-equity firm, which has spent more than $4 billion on 24,000 rental properties in the last year making it the largest buyer in the U.S., purchased the residences from Building and Land Technology, said Marcus Ridgway, chief operating officer of Invitation Homes, Blackstone’s single- family rental division.

In the past 12 months Blackstone has raised over $8 billion to buy up medium and low priced housing, while JP Morgan has initiated a fund to buy up to 5,000 homes. Morgan Stanley has raised a billion dollars to buy up to 10,000 homes.

If it strikes you as odd that the big banks would be bailed out by the taxpayers and then turn around and use that same money to buy homes to then rent back to those same taxpayers, then we hold the same view.

This trend has been running for so long, and it is so obvious, that it really raises a very important question as to exactly how such context can be left out of any article on the recent rebound in house prices.

As we saw with bonds being driven to generational lows, the Fed's distortive buying habits shaped the prices for the entire bond market ranging from Treasurys to corporate junk. Nobody in their right mind would ever consider the prices of bonds to be telling us anything useful about risk, reward, the future, or even current conditions without noting that their current prices are heavily manipulated to the upside.

Similarly, the stock market is clearly being driven upwards on a sea of Fed supplied liquidity and everybody knows that once if that Fed money dried up today the stock market would fall like a stone.

Housing is no different. As big as the market is, prices are driven at the margins and the buying pressure of institutional money snapping us thousands and thousands of properties in a single markets in a single month means that this money too is having a distortive effect and is driving prices upwards.

Unfortunately, it seems like the lessons of 2008 went entirely unlearnt.

This is a companion discussion topic for the original entry at https://peakprosperity.com/housing-prices-are-being-dangerously-distorted-by-big-institutional-money-2/