Originally published at: https://peakprosperity.com/investing-when-nothing-matters-and-anything-goes/

The recent US equity market rally has a lot of people scratching their heads, Paul Kiker and I included.

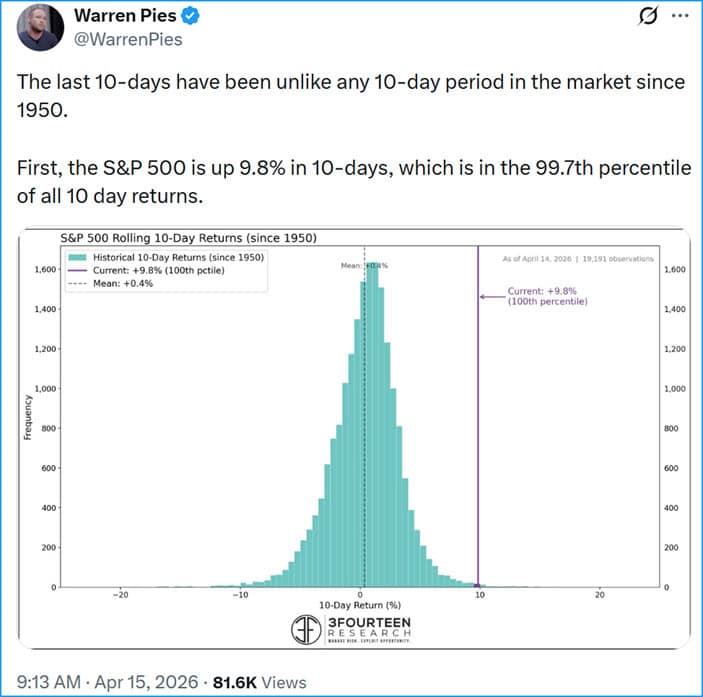

As of April 14th, the rally was not only strong, but in the 99.7th percentile for all 10-day market returns in all of the S&P 500’s history.

Are things really that awesome? Most people think not.

Especially Main Street, which is recording the lowest consumer confidence in decades.

That may be related to the fact that US housing sales are at “depression levels” according to Nick Gerli, who recently noted that the only worse month for March housing sales was March 2009.

This massive disconnect between Wall Street and Main Street is yet more evidence that the system which rules the financial and political spheres isn’t serving the majority, but rather a very narrow (and narrowing) set of interests.

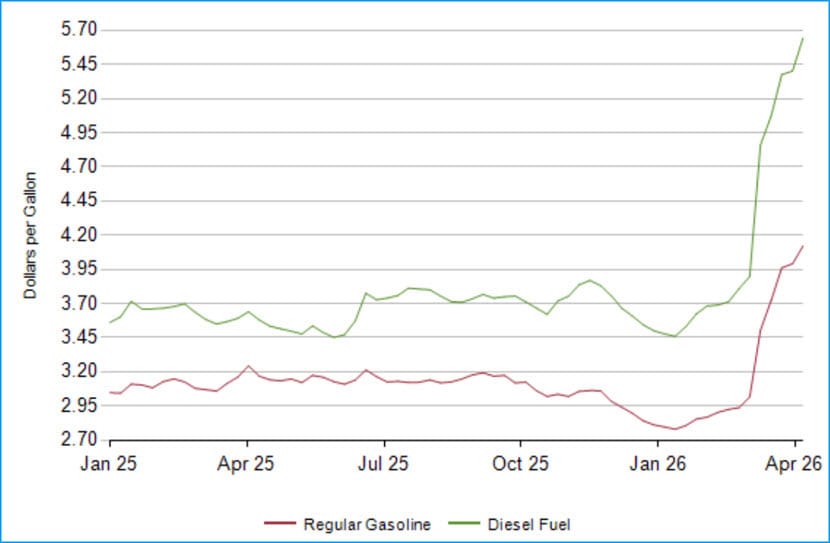

Most people have been living with the reality of the sharpest single-month hike in gasoline and diesel prices on record:

Of course, this is going to stoke inflation (as it’s measured), but in reality, this isn’t prices rising due to the overproduction of money (the definition of inflation), rather rising prices due to supply shortages.

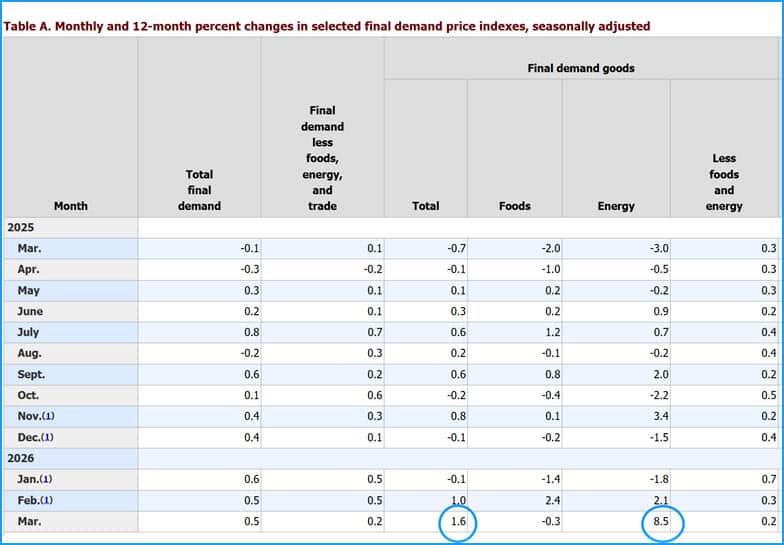

Naturally and predictably, the US BLS agency came out with a laughable Producer Price Index (PPI) reading. In it, the BLS claimed that energy costs had only risen by 8.5% for producers during March, a month in which oil-related energy sources were up by 37% to 66%.

If you note the total for Goods inflation, however, standing at 1.6% for March, that would annualize out to 21% inflation were it to be sustained.

Now, we’d expect that to moderate, but that depends on the Iran war ending today. Every week that it drags on is another week of oil supply shock that will have to be resolved via ‘demand destruction,’ which can only come about by price increases.

Well, it can also come about by forced government rationing, but that never actually works out because that merely enforces economic destruction from the top down rather than letting the economy work it out from the bottom up.

It seems that fundamentals (housing, consumer stress, energy, inventories) no longer align with US equity market price action. Welcome to the Truman Show.

It is a time that calls for prudence, caution, and having a defined plan of action to navigate what has become a set of markets that are disconnected from reality. But they always have to realign, and when they do, it’s usually ‘chaotic’ to use a euphemism.

Timestamps:

00:00 Market Movements and Economic Indicators

14:57 Housing Market Crisis and Consumer Confidence

28:11 The Rising Costs of Insurance and Its Impact

29:03 Concerns Over Private Credit and Insurance Markets

30:53 Oil Market Dynamics and Inventory Flows

32:46 The Global Oil Market and Price Influences

34:22 The Need for Price Adjustments in Oil

36:37 The Risks of Market Manipulation and Rationing

39:27 Unpredictability of Economic Responses

40:55 The Discrepancy in Oil Pricing and Market Signals

42:53 Producer Price Index and Inflation Expectations

46:34 Energy Price Shocks and Market Mysteries

50:45 Inflation Expectations and Market Confusion

52:26 Navigating the Strait: Economic Implications of Conflict

55:40 The Complexity of Global Supply Chains

01:00:02 The Ticking Clock: Oil Supply and Global Stability

01:05:18 The Role of Passive Investment in Market Dynamics

01:10:57 Prudent Financial Strategies in Uncertain Times

01:17:31 Preparing for the Future: The Impact of AI on Employment

FINANCIAL DISCLAIMER:

The information contained in this video and the resources available for download through our affiliated website are not intended as and shall not be understood or construed as financial advice, nor should be interpreted as a solicitation to sell or offer to sell investment advisory services. No person who currently works for or contracts with Peak Prosperity or Peak Financial Investing is an attorney or accountant, nor are we holding ourselves out to be, and the information contained in the video and on the website is not a substitute for legal or tax advice from a professional who is aware of the facts and circumstances of your individual situation. While Peak Financial Investing is a registered investment advisor, please note that this podcast is not intended to be investment advice.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. We have done our best to ensure that the information provided is accurate and provides what we feel is valuable information. The views expressed are subject to change based on market and other conditions.<

No guests or clients appearing on the podcast receive any form of compensation for their appearance and obtained no other benefit from either Peak Prosperity or Peak Financial Investing.

All investing involves risks including the possible loss of capital. Asset allocation and diversification does not ensure a profit or protect against loss. Please note that out- performance does not necessarily represent positive total returns for a period. There is no assurance that any investment strategy will be successful. All investments carry a certain degree of risk. Dividends are not guaranteed, and a company’s future ability to pay dividends may be limited.

Additional important disclosures for Peak Financial Investing may be found in our Form ADV Part 2A, which can be found at https://adviserinfo.sec.gov/firm/summary/319672.