Conditions today mirror 2016, when growing weakness in the global economy and wobbling financial markets caused the world’s central banks to absolutely freak out.

They responded by dumping more thin-air money into the system than ever before in history. And it worked (for them at least). Economic growth stabilized; and the prices of stocks, real estate, and other assets enjoyed another three-year joyride.

Similarly, as things started getting shaky in late 2018, the same playbook was deployed. And again, we've seen stocks rocket upwards ever since.

But will the strategy actually work this time? It's unclear. And a lot is riding on the answer.

Back in 2016 the financial world was falling apart. The US dollar was spiking. Emerging market currencies were getting destroyed. The S&P 500 equities was exhibiting a classic head-and-shoulders formation, indicative of a coming plunge. The macro-economic outlook looked grim, too, with global trade slipping into contraction:

(Source)

But then everything suddenly turned around, as if by magic.

Well, we now know that ‘magic’ was actually a massive quantity of monetary and fiscal stimulus pumped into the system by the world's central banking cartel.

Our concern is that the monetary and fiscal authorities are thinking that since they were “successful” back in 2016, they can repeat the same strategy here in 2019.

But can they? Maybe. Or maybe not.

If the answer is “yes,” our prediction is to expect what we got last time, just taken to more extremes: a vastly wider wealth gap between the 1% and everyone else, accelerated destruction of savers and the middle classes, and anemic GDP growth coupled with explosive further growth of global debt levels.

If the answer is “no,” a massive crash of epic proportions, unlike any most of us have ever experienced, is in store. Credit bubbles are ugly beasts. They're fun while they last but devastating when they burst. The longer they carry on, the worse the crash when it comes -- this bubble has been going on for longer than most people ever could have imagined.

2016: A Post-Mortem

It's eerie how closely recent developments resemble what took place at the start of 2016.

In 2016, there were slumping emerging markets, a slew of macro indicators pointing to a global slowdown, and equity bear markets all over the place. And then – presto! – everything reversed during one night in February 2016. It was as if nothing had ever happened.

Somehow all those fundamental macro warnings just melted away in a burst of financial market exuberance.

S&P futures took off in the overnight session between Feb 7th and the morning of February 8th as if the entire world suddenly had a change of heart:

From that moment on, the S&P started climbing to new all-time highs, practically unabated, until September 2018.

So, what happened here? What new information became available to the world’s investors in the wee late night/early morning hours of February 8th , 2016 that wasn’t available the day before?

Nothing fundamental, that’s for sure. Massive buy orders showed up in the middle of the night and it was only later that the economic data began to turn the corner.

What came first was the tremendous application of monetary, fiscal and financial stimulus. Just gobs and gobs of it. Economic recovery, such as it was, showed up later.

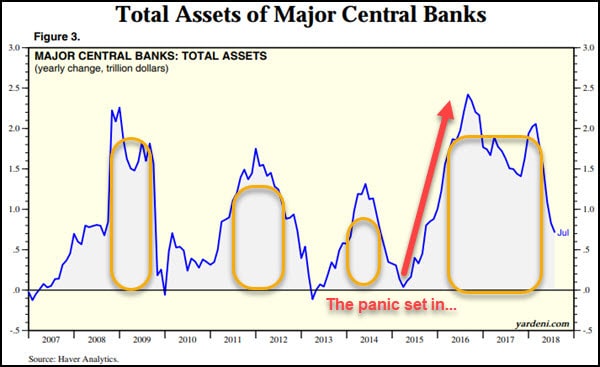

What you need to understand is that between 2016 and the middle of 2018 the world’s central banks opened up the floodgates here and poured the most amount of money into the system since the Global Financial Crisis began back in 2008.

In the chart above, you can see where the central banks panicked back in mid-2015. It didn't take long for their combined printing hit the highest run-rate of the entire crisis at $2.5 trillion dollars by mid-2016. They then kept the pedal to the metal clear through mid-2018. This represents by far, the largest stimulus of the entire mis-begotten Quantitative Easing experiment that began after the GFC -- printing up money from thin-air to jam into the financial markets (and thus into the portfolios of the rich).

The. Most. Money printing. Ever.

By a huge margin.

This wasn’t even remotely in line with their public statements, which were all geared towards soothing and placating the masses.

“The economy is robust” they said. “Growth is on track,” they cooed.

But behind the scenes they were hastily, and often haphazardly, dumping the largest-ever quantity of money and credit into the system the world had ever seen. Not unlike how a 5-year-old, fearing getting caught, pushes a pilfered bag of chips quickly under a nearby sofa cushion.

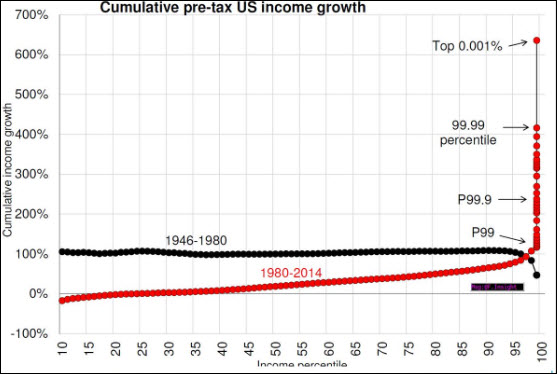

As mentioned frequently here at Peak Prosperity, even though a painful correction was likely avoided by these efforts, not everybody shared equally in the resulting years of continued gains:

In a system now as heavily financialized as ours is, the benefits of such extreme stimulus efforts accrue exponentially to those who own and control financial assets -- those at very tippy-top of the wealth/income distribution.

It's amazing to see how not only does the top 1% dramatically outpace the bottom 99%, but the top 0.1% leaves the top 1% in the dust. Same for the top 0.01% vs the 0.1%. And the top 0.001%? They're in a stratosphere all their own.

The developed world is quickly becoming an oligarchy. And more central bank printing only exacerbates that dynamic.

The more they prop up the system with more money printing, the more Trumps, Brexits, Yellow Vest protestors, and populist politicians we’ll see. Money printing is a political act of wealth redistribution from the bottom to the top. It’s unfair and socially destabilizing.

Even if they can't yet see the true culprit here, the masses are beginning to wake up to how badly screwed they're getting.

Until And Unless

“Until and unless,” we wrote in early 2018. We warned that "until and unless" the world’s central banks reversed course and began printing like crazy, the vast global cesspool of over-expensive bubbly financial assets would soon undergo a painful downwards re-pricing.

And start fall they did; through September 2018 up through Christmas Eve. Then, as they have done so many times, a “miracle” bottom was formed -- one that didn’t resemble a true bottom, where buyers and sellers settle in and wrestle for a while with neither side gaining ground. What we experienced instead was a very steep “V.”

A “needle bottom” if you will; an upside-down Matterhorn:

What caused this violent reversal? Some immediate return of global macro conditions to amazing awesomeness? Some new data revealing massive new sources of corporate profits?

No, none of that. It was just another $1 trillion of central bank money printing, coupled with every other conceivable option to shove additional money and credit into the system.

In a recent interview, James Grant (of Grant's Interest Rate Observer) provided his views on the Fed and other central banks and their role in backstopping every downwards wiggle in today's stock ““markets”” (emphasis mine)

Q: What would you do if you were at the helm of the world’s most powerful central bank?

A: I fear it might be too late, but to start with, I’m in favor of interest rates which are discovered in the marketplace. And, at the very short end, interest rates ought to be pitched at a level that provides some premium to the inflation rate.

So, my first order would be to give a speech saying that we are out of the business of manipulating expectations; we are out of the business of manipulating the stock market. The stock market is going where it wants to go, and if it goes down a lot, so be it. That’s not our line of work. We are in the business of securing a currency which holds its value and which provides a good medium of exchange.

Q: Sounds straightforward. But how would the financial markets react?

A: They would consider it as very radical and very unhelpful. But the way forward is to somehow reinstitute the interaction of supply and demand on Wall Street and to get the Fed out of the business of wholesale manipulation of values. Because today, the Fed is expected to intervene when things go badly and what this has given us is immense distortions.

(Source)

The central banks are so terrified of the Franken-Markets they’ve created that they now intervene both directly and indirectly, overtly and covertly, to do anything and everything necessary to prevent them from ever going down again.

James Grant thinks the Fed should get out of the business of wholesale manipulation of asset prices, and we could not agree more. Its constant interventions and manipulations are terribly destructive on so many levels – societally, structurally, ecologically, and politically – that it’s worth an entire book to point them all out.

But here we are. And the Fed does not look like it's planning to change its behavior anytime soon.

This Better Work

Our macro-beef with all of this is that even if the Fed is “successful”, we all lose.

The natural end to its current policies is a tiny fraction of the population owning everything.

But even worse than that, our planet is being despoiled by this desperate quest for more fantasy wealth, represented by fantasy digits within the entirely human-contrived fantasy of our financial markets.

The "immense distortions" that James Grant mentions above lead to all sort of malinvestment that should never happen in a rational world. But as long as there's a short-term profit motive funded by endless thin-air money, there's an incentive to harvest the last tree, fish the last tuna, drain the last aquifer. And then where will we be?

If we don’t tame our addiction to endless growth(always more, more!) then we’ll simply consume ourselves out of existence, or at least to a civilization-ending conclusion.

Real wealth consists of real things. It’s health. It's the safety and security of those we care about. It's access to food and clean air and water. It's being in meaningful relationships, held lovingly in the here and now.

What we call money is a claim on wealth. But it's not real wealth in and of itself. Hopefully we can all agree that if the sun blinked out for some reason, we’d soon realize that money was never the thing of vast importance we made it out to be.

Similarly, if our ecosystems crash, we’ll learn that the pursuit of money is much less important than we currently realize. Certainly not as important as eating.

Or if we stupidly allow the gap between the wealthy and the poor to widen, we’ll soon wake up to the type of revolution that history books are full of.

The steps being taken by today's central banks are diverting us from having the conversations we really need to be engaging in. Those in power perpetuate the repeatedly disproven idea that printing money is the same thing as prosperity. Our future is bleaker for their actions, not brighter.

The younger generations are starting to figure this out in droves as they face the piling evidence that they are inheriting a world burdened by debt, pollution and serious inequality. This is something the Baby Boomers running the central banks really ought to be noticing.

Sooner or later the propping, the manipulating, the cajoling and the distorting will fail. When it does, the aftermath will be quite unpleasant.

Tragically, we could have avoided much of the coming reckoning if we’d learned the right lessons from 2000 and 2008 and allowed the bad debts and the poorly-run large banks to simply fail. The world would have shuddered for a brief period, but it would have then carried on from a much more sustainable baseline.

The wealth gap would be a fraction of what it currently is, and Trump almost certainly would not be president, Brexit not on the table, and populist movements blooming like California poppies after heavy spring rains.

But we didn't learn the right lessons. And so here we are.

In Part 2: Why This Better Work, we look closely at just how awful the fast-deteriorating macroeconomic situation is. It's very bad. GDP is falling in nearly every region of the globe, long-hot real estate markets have nosed-over, world trade volumes are shrinking, industry energy consumption is in decline -- the list goes on and on.

Left to itself, the economy would enter recession in a skinny minute to flush out the many trillions of bad debt and malinvestment that have accreted over the past decade. To prevent this from happening and to keep asset prices moving higher -- or to even simply keep them at their current ultra-expensive levels -- the central banks will need to deploy a truly mind-boggling amount of intervention.

Will they? And will the system respond the same way it did before?

And even if it does, will the 99.9% placidly subsist on even smaller crumbs as the remaining wealth is hoovered into the pockets of the top 0.1%?

If the answer to any of these questions is "no", none of us is fully prepared for what's coming.

Buckle up.

Click here to read Part 2 of this report (free executive summary, enrollment required for full access).

This is a companion discussion topic for the original entry at https://peakprosperity.com/its-2016-all-over-again-or-is-it/