Famed market analyst and historian James Grant is no fan of the current policies of the US Federal Reserve:

Distortion in the cost of credit is the not-so-remote cause of the raging fires at which the Federal Reserve continues to train its gushing liquidity hoses. But the firemen are also the arsonists. It was the Fed’s suppression of borrowing costs, and its predictable willingness to cut short Wall Street’s occasional selling squalls, that compromised the U.S. economy’s financial integrity.At age 74, having lived through a number of economic booms and busts as well as having authored numerous books on the history of financial markets, Jim sees the degree of speculation, overvaluation and malinvestment in today's markets as about as bad as it's ever been.

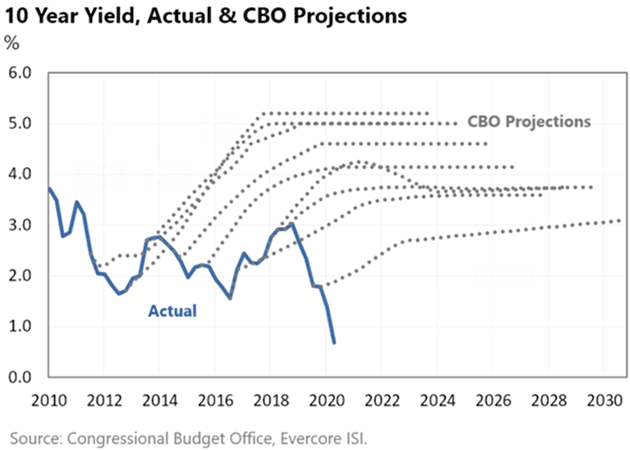

He lays much of the blame at the feet of the Fed and its global central bank brethren, who collectively through their intervention have suppressed interest rates to their lowest levels in all of recorded history:

This has resulted in all sorts of unnatural distortions and deformations that are hollowing out our economy and social structure.

As Jim recently wrote:

Needing income, investors will take imprudent risks to get it. And if 2% invites trouble, zero percent almost demands it.Not only do 0% interest rates act as "molasses" on growth by gumming the system up with zombie institutions and toxic malinvestment, but it imperils the social good.

Savers and investors, increasingly desperate for yield, are forced to accept worse and worse choices in attempt to stay afloat.

Under this regime, the rich benefit disproportionately at the expense of everyone else AND it creates a “hyperinflation in the cost of retirement”. This accelerating war on the 99% can not stand for much longer without serious consequences and repercussions.

We are thrilled Jim was gracious enough to come on the program this week. It was a huge honor to finally get to interview him (after years of attempt) and I can tell you firsthand, not only is he prodigiously smart, but he is ridiculously nice. A true class act.

But simply put, he’s one of the most respected market analysts and historians on the planet.

So when an expert like him warns that today’s markets are at one of the most dangerous levels of speculation in history, we all better be paying close attention:

")

And if you’re one of the many readers brand new to Peak Prosperity over the past few months, we strongly urge you get your financial situation in order in parallel with your ongoing physical coronavirus preparations.

We recommend you do so in partnership with a professional financial advisor who understands the macro risks to the market that we discuss on this website. If you’ve already got one, great.

But if not, consider talking to the team at New Harbor. We’ve set up this ‘free consultation’ relationship with them to help folks exactly like you.

This is a companion discussion topic for the original entry at https://peakprosperity.com/james-grant-why-market-risk-is-near-the-highest-in-history/

{kind=link}

{kind=link}

{kind=link}