The American spirit is rooted in the belief of a better tomorrow. Its success has been due to generations of men and women who toiled, through both hardship and boom times, to make that dream a reality.

But at some point over the past several decades, that hope for a better tomorrow became an expectation. Or perhaps a perceived entitlement is more accurate.

It became assumed that the future would be more prosperous than today, irrespective of the actual steps being taken in the here and now.

And for a prolonged time – characterized by plentiful and cheap energy, accelerating globalization, technical innovation, and the financialization of the economy – it seemed like this assumption was a certain bet.

But these wonderful tailwinds that America has been enjoying for so many decades are sputtering out. The forces of resource scarcity, debt saturation, price inflation, and physical limits will impact our way of life dramatically more going forward than living generations have experienced to date.

And Americans, who had the luxury of abandoning savings and sacrifice for consumerism and credit financing, are on a collision course with that reality. Like the grasshopper in Aesop's fable, they have partied away the fair seasons and winter is now on the way, which they are not prepared for.

The prudent thing to do here would be to have an honest, adult-sized conversation with ourselves about our level of (un)readiness and how best to use the resources and time we have left while the system still works more or less the way we're used to. There are certainly strategies and steps we can take in the here and now to best match priorities to needs, and meet the future as prepared as possible.

But you won't find this discussion in the national media. Our politicians insist on charting a course of more of the same, no matter how unsustainable, adamant not to touch any political third rails – for fear of not pleasing the electorate and/or donors. Major media outlets have abandoned the investigative journalism that once held the mirror of truth up to power, and instead, run superficial puff pieces that conclude with platitudes – for fear of not offending viewers and/or sponsors. The message is clear: The future will be better as soon as economic growth returns. Or oil prices come down. Or the iPhone 6 comes out. Or whatever the magic bullet du jour.

So it's up to the concerned and critical-thinking among us to look at the math, the hard data underlying the headlines, and construct what we can best calculate to be true.

And the truth is: The three adult generations in the U.S. are suffering, and their burdens are likely to increase with time. Each is experiencing a squeeze that is making it harder to create value, save capital, and pursue happiness than at any point since WWII. At that point, we were a creditor nation with an economy exploding into dominance on the world stage. Now, however, the U.S. is the largest debtor nation and our economic hegemony is increasingly at siege across a number of fronts.

A continuation of the status quo is a decision to sleepwalk face-first into the constraints hurtling towards us.

Instead, shouldn't we stop fooling ourselves and ask: What should we be doing differently?

We'll address that after we walk through the numbers.

Seniors Woefully Unprepared for Retirement

In the late 1970s, the 401k emerged as a new retirement vehicle. Among its touted benefits was the ability of the individual to save as much as s/he thought prudent for his/her financial future. Companies loved the new private savings plans because they gave them a way out of putting aside mandatory savings for worker pensions. For a long time, everyone thought this was a big step forward.

Three decades later, what we're realizing is that this shift from dedicated-contribution pension plans to voluntary private savings was a grand experiment with no assurances. Corporations definitely benefited, as they could redeploy capital to expansion or bottom line profits. But employees? The data certainly seems to show that the experiment did not take human nature into account enough – specifically, the fact that just because people have the option to save money for later use doesn't mean that they actually will.

First off, not every American worker (by far) is offered a 401k or similar retirement plan through work. But of those that are, 21% choose not to participate (source).

As a result, 1 in 4 of those aged 45-64 and 22% of those 65+ have $0 in retirement savings (source). Forty-nine percent of American adults of all ages aren't saving anything for retirement.

Of those with retirement savings, the numbers are not good. Over half of US retirees have less than $25,000 in savings:

(Source)

Most planners advise saving enough before retirement to maintain annual living expenses at about 70-80% of what they were during one's income-earning years. Medicare out-of-pocket costs alone are expected to be between $240,000 and $430,000 over retirement for a 65-year-old couple retiring today.

The gap between retirement savings and living costs in one's later years is pretty staggering:

- As the table above shows, nearly 83% of retired households have less saved than Medicare costs alone will consume.

- One-third of retired households are entirely dependent on Social Security. On average, that's only $1,230 per month – a hard income to live on. (source)

- 34 percent of older Americans depend on credit cards to pay for basic living expenses such as mortgage payments, groceries, and utilities. (source)

As for Medicare, the out-of-pocket costs could easily soar over retirement. The Wall Street Journal reports that the current estimate of Medicare's unfunded liability now tops $42 Trillion. Such a mind-boggling gap makes it highly likely that current retirees will not receive all of the entitlements they are being promised.

And the denial being shown by baby boomers entering retirement is frightening. Many simply plan to work longer before retiring, with a growing percentage saying they plan to work "forever".

But the data shows that declining health gives older Americans no choice but to leave the work force eventually, whether they want to or not. Years of surveys by the Employment Benefit Research Institute show that fully half of current retirees had to leave the work force sooner than desired due to health problems, disability, or layoffs.

Add to this the nefarious impact of the Federal Reserve's prolonged 0% interest rate policy, which makes it extremely hard for retirees with fixed-income investments to generate a meaningful income from them.

The number of Americans aged 65 years and older is projected to more than double in the next 40 years:

Will the remaining body of active workers be able to support this tsunami of underfunded seniors? Don't bet on it.

Taxes and Inflation Are Sucking Productive Workers Dry

To borrow from another fable, U.S. policy is doing its best to kill the goose that lays the golden eggs. Bottlenecked between retirees and the younger "millennial" generation is the current "productive peak" working class. As government, mired in debt and budget deficits, grows desperate to boost tax receipts and keep interest rates on its debt manageable, it is increasingly both siphoning capital and stealing purchasing power from those generating income.

History shows that this cannot continue indefinitely. Eventually you exhaust the incentive for working and your productive class goes on strike.

How close are we to that breaking point? It's not hard to find a litany of articles on the Internet these days warning that it's coming soon:

Personal Incomes & the Decline of the American Saver

If we put all of this together we can see a picture of the average American. The chart below shows the annual change in personal incomes combined with the annual change in personal expenditures. What is clear is that consumption has been supported by rising transfer receipts (welfare) and a drop in the personal savings rate which is now at the lowest level since just prior to the last recession. The consumer is clearly struggling to maintain their current standard of living and all indications are that they are going to lose this battle.

Consumer Spending Drought: 16 Signs That the Middle Class Is Running out of Money

Is "discretionary income" rapidly becoming a thing of the past for most American families? Right now, there are a lot of signs that we are on the verge of a nightmarish consumer spending drought. Incomes are down, taxes are up, many large retail chains are deeply struggling because of the lack of customers, and at this point nearly a quarter of all Americans have more credit card debt than money in the bank. Considering the fact that consumer spending is such a large percentage of the U.S. economy, that is very bad news. How will we ever have a sustained economic recovery if consumers don't have much money to spend? Well, the truth is that we aren't ever going to have a sustained economic recovery. In fact, this debt-fueled bubble of false hope that we are experiencing right now is as good as things are going to get. Things are going to go downhill from here, and if you think that consumer spending is bad now, just wait until you see what happens over the next several years

Looking from a bird's-eye view, real wages have been falling in the U.S. for decades. The below chart includes numbers based on the officially reported Consumer Price Index (or CPI, the methodology of which has been changed many times to make the output "kinder and gentler"), as well as those from ShadowStats, which applies a standardized and less fuzzy methodology to try to get to a truer picture. You can see that according to ShadowStats (the dark blue line), real wages have been plummeting in recent years as the Federal Reserve has been running the money-printing machines at full tilt:

Meanwhile, the cost of living has soared as the Fed's liquidity has found its way into the commodities markets and driven prices of essentials higher:

So today's worker is enjoying paying for substantially costlier goods with a materially devalued income – that is, if they are fortunate enough to have an income. Unemployment in the U.S. is still painfully high. Even the recently-celebrated declines are due to a jump in part time jobs as workers take on multiple jobs to simply get by. Full-time jobs are actually on the decline.

At the same time, in pursuit of greater efficiencies, U.S. corporations are investing more than ever in automation. Many of the less-skilled jobs lost during the Great Recession are simply not coming back, as human labor is increasingly replaced by robots and intelligent machines.

And yes, while the stock market is up nicely in the past year, the wealth gains from this are hyper-concentrated within the top 10% – really the top 1%, as this excellent video visualizes. (Warning: viewing this may make the blood boil.) The mean U.S. household currently only has about $50k in savings (and that average is skewed upwards by the super-rich).

<p class="rtecenter" style=">

These workers have also been whipsawed over the past decade by several asset bubbles blown by central banks that have knee-capped their efforts to amass wealth. The S&P 500 stock index has just returned to price territory last seen in 2001 and 2007, and housing prices are only slowly beginning to rise again in the aftermath of the vicious correction begun in 2007. Sadly, it seems that new bubbles in stocks, bonds and housing are being inflated once again – sure to take a large swath of wealth from these workers when they burst.

Perhaps the arriving cohort of younger workers will be able to support their elders once they hit their peak earning years. We can hope.

But again, the prospects do not look encouraging.

Millennials at Risk of Becoming a Lost Generation

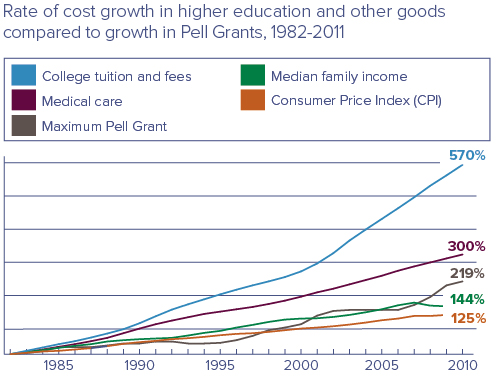

Pity the recent college graduate. The cost of higher education has been far outstripping inflation for years, largely due to that fact that most colleges have no exposure to their students' ability to repay their loans. So universities actually have an incentive to continue to raise tuition and other fees as high as the market will possibly bear.

The average graduating student has a student loan balance of over $27,000 (not including credit-card or other types of debt that many students also have). This puts them into a hole early in their adult lives that delays their ability to create families, buy a first home, or start businesses.

This challenge to capital formation is compounded by the frighteningly high unemployment rate of approximately 12% for those under 30. Not only are companies still hiring conservatively, but given the factors mentioned above, younger workers find themselves competing with older ones for entry-level positions to an extent not seen in living memory.

It's no wonder there's a growing perception that going deep into debt for a college diploma isn't a smart trade-off. A number of today's graduates will be finally paying off their balances around the same time their own children are heading off to college.

And along with the joys of debt-serfdom, younger workers are realizing they can't count on:

- loyalty from the companies they work for

- a national infrastructure that is the envy of the world

- low oil prices

- affordable healthcare

- affordable home prices

- easy access to credit

- Social Security

...and a number of other elements of the "American promise" that preceding generations were able to take for granted.

It's no surprise that millions of young workers are giving up on searching for work.

Of course, the big danger for this generation's members is that the longer they go without work experience, the less appealing they become to employers when hiring does begin to pick back up. Tomorrow's new college graduates will be hired for entry-level positions, leaving many of today's unskilled seekers "unemployable" – a lost generation.

Let's Stop Fooling Ourselves

In summary, if we're being honest with ourselves, the current narrative of recovery being pushed by Wall Street and the mainstream media doesn't make any sense. The American experience of rising standards of living and general prosperity have always rested upon a deep and healthy middle class. That middle class, by almost any available economic or financial measure, is steadily losing ground as a direct consequence of Fed and DC policies.

By forcing the stock market higher, the Fed has simply made a small minority of the country better off By funneling endless amounts of free money to the biggest banks, the Fed has enriched the banking system. The Fed truly seems to believe that this is the right course of action: that a stable and profitable banking system coupled to rising stock prices will somehow generate the necessary confidence within the middle class required for them to once again go on a borrowing binge.

Because that's what the system has devolved into, for better or worse: our economy is founded on credit and borrowing, not earnings and savings. The problem is, outside of the manufactured statistics of government and the manufactured stock prices of the Fed, the median family has far less earning power this year than last. And it knows in its heart of hearts that DC will tax more and return less as time goes on, and that job security no longer exists as corporations ruthlessly pursue bottom line results. Quite rationally, many families are realizing that's not an appropriate environment for taking on more debt.

More profoundly, the big picture numbers just don't add up. A nation that's collectively in hock to the tune of 373% of GDP – not including entitlement liabilities which launch that figure to more than 1000% – needs to seriously face the fact that it cannot make good on its current promises, let alone entertain making them larger. And yet here we are, with every outlet of the current power structure vigorously promoting that "all is well" while minimizing or completely ignoring those who would seek to open a dialog about the wisdom, or lack thereof, of ramming asset prices higher and supporting historically ruinous levels of deficit spending by printing money out of thin air.

Redefining Prosperity

As dire as the trends look, there is much that can be done to ameliorate their impact – and enter the future with grace and optimism – if as a society we have the courage to do it.

There's no doubt that simply continuing along the status quo is a vote for digging ourselves deeper as the constraints of the future arrive. Behavior change is necessary in order to improve our chances.

At the core of the needed change is redefining prosperity. In modern society, it has largely come to be defined by material possessions, usually assuming that the more (and the more expensive), the better.

In the future, we'd do much better to define it by:

- our health (both physical and emotional)

- our purpose

- our ability to meet our needs sustainably

- our relationships

- our level of happiness

All things that were once valued much higher in our culture.

It's important to realize that when the cheap energy and associated cheap-credit era arrived, the work of all those energy and liquidity "slaves" allowed us to disassociate ourselves from centuries-old customs and live a much more isolated, materialistic life. While freeing in ways, perhaps, we are beginning to realize that those values and norms evolved for a reason. We'll be on a journey of rediscovering their worth as we start trending back towards more historic baselines.

The good news is the list of prudent behavior to adopt is long, and it's growing as we (here at PeakProsperity.com and related sites) work together to identify those with the most promise. This is by no means an exhaustive account, and I look forward to active discussion and additions in the Comments section below:

- Live below your means – Rather than pride yourself on what you purchase, pride yourself on what you don't. That doesn't mean you must live miserly or live in poverty. Learn the peace of mind that comes from knowing you can afford the things you do buy, and the confidence that comes from growing your savings. (Frugality is the #1 quality that all self-made millionaires share)

- Buy quality and maintain it – When you do purchase something, buy for utility and longevity. "Cry once" is a good motto: in other words, pay a premium if necessary to get what will meet your needs best over the longest time horizon (versus "crying often" and spending more $$ over the long run because you bought an inferior product that needed chronic repairs or replacement). Take good care of what you do buy to ensure it will be there as you need it when you need it.

- Take control of your income – Avoid being a wage slave for your entire life. There are innumerable reasons why your situation with your employer can change faster and more drastically than you think. Cultivate an income you "own", either full-time or on the side, so that you aren't left 100% vulnerable to a sudden change in employment. (I realize this is easier said then done, but it is doable by just about everybody. We have a guide we'll publish on this subject within the next few weeks.)

- Cultivate resiliency – Invest in your skills, your homestead, your health, and your community. These will all serve you well as economic growth slows further due to reasons outlined in the Crash Course – and for the skeptics, these are solid investments no matter which way the economy turns. For those new to resiliency, our What Should I Do? Guide is a useful resource to start with.

- Simplify – Learn that less is more. Fewer things to deal with frees you up to focus more on those that matter most. In addition to being a good philosophy to live by, it also reduces the number of things to pay for and the number of things to be taxed on. Both of which leave more money in your pocket.

- Apprentice/mentor – Learn how to do important tasks yourself instead of becoming dependent on paying someone. If you can trade labor for learning, you may be able to avoid some or all of the excessive time and $ costs of academia. If you have expertise, pass it on to others around you. In this way, we create resiliency at the community level, improving the odds that an effective local support network is in place if ever needed.

- Shop & invest locally – Keep capital inside your community to strengthen it and enable re-investment. So much is currently sent to multinational corporations and Wall Street banks – never to return – that even a small percentage redirection will make a big impact at the local level.

- Prefer hard assets to paper ones – In a world of runaway central bank money printing, paper currencies (like the U.S. dollar) are not a smart option for storing wealth. Nor are dangerously inflated paper securities like stocks and bonds. If possible, purchase physical assets you can tangibly hold and store, like precious metals, and for the rest of your investments, find a financial advisor who has a strategy that takes hard assets and depleting resources into account. (We know a few, if you're looking.)

- Consider multi-generational living – The economics of the future may force this on us, and that may not be a bad thing. But it's better to adopt this lifestyle by your own choice, on your own terms, if possible. We have moved so far away from this model of living, at great cost – both money-wise and socially. Knowledge transfer, chore sharing, child/elder care, emotional support, cost reduction, pooled purchasing power – there are many advantages to co-habitating with close family or friends.

- Get and stay fit – The benefits of good health on quality of life, longevity, and net worth are just too numerous to ignore. The modern "sick care" industry over-focuses on treating what breaks. Instead, focus on achieving and maintaining wellness. Chris did it; you can, too.

- Use your productive output as an alternative currency – Much can be acquired without $, in trade for your support or skills. Both goods and services. Learn to ask: What can I trade? before asking How much does it cost? You'll save money while at the same time increasing your perceived value to those around you.

- Pursue happiness – Learn that pleasure comes from relationships, from having purpose, from creation, and having new experiences. All of these can be enjoyed in a multitude of ways, and few require spending lots of money. If you manage to simplify your life (see above) and find pleasure in doing so, you'll be much more likely to enjoy the future, whatever it brings.

- Require awareness and accountability for the future – Hold your elected officials to the same standards you hold yourself. Vote accordingly. Participate in the democratic process. It may not work as well or as fast as we want, but boycotting will only guarantee us disappointment. In a nutshell, hope for the best but don't plan on miracles.

- Trust yourself – Always rely on your own good sense and intuition about what makes sense for you and your family in your unique situation. Do consult with those who have insight and experience to share that will help you make the most informed choices you possibly can, but remember that your present and future are your own responsibility. Do not ever fully relinquish this power to anyone else – not the government, not a family member, not a professional adviser, not even "the experts ." Always, always trust yourself first and foremost.

There are other prudent behaviors to add to this list, but this is a pretty good start.

And a good start is what we need, as a country and a global community: to stop denying the reality around us and start getting on with how we want to deal with it.

~ Adam Taggart

This is a companion discussion topic for the original entry at https://peakprosperity.com/lets-stop-fooling-ourselves-americans-cant-afford-the-future/