The melt-up discussed last week remains in full force, with the S&P 500 hitting a new intraday all-time high on Wednesday.

Just to make sure we’re all clear on this: stocks are back to their highest prices BEFORE the coronavirus pandemic exploded. Before Q2 GDP plummeted -33% in the US. Before 50+ million Americans lost their jobs.

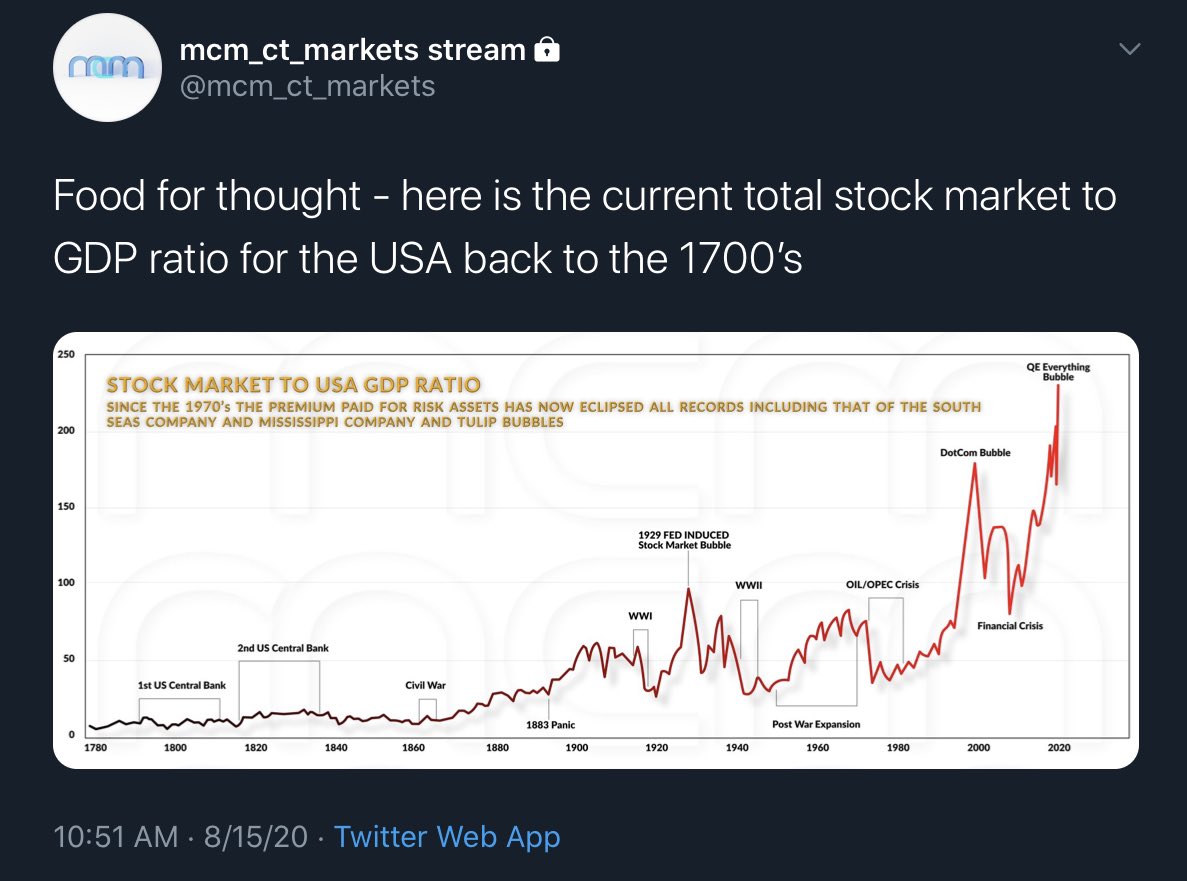

Thanks to the $trillions shoved into the system by both central banks and national legislatures since April, “investors” now believe the markets are a 1-way ride to forever-increasing wealth.

As the chart below from the National Association of Active Investment Managers shows, financial advisory firms that manage client capital are more fully-invested in the markets than at any other time in the past several years:

<img class=“aligncenter wp-image-578298 size-large” src=“https://peakprosperity.com/wp-content/uploads/2021/09/NAAIM-chart-1024x669-1.png” alt="“NAAIM chart” width=“1024” height=“669” />

So everyone in “all-in” on the belief that the markets are both fully backstopped and rising higher from here.

How realistic is this belief?

Michael Pento, this week’s Market Update video expert guest, thinks it’s willful delusion. History is crystal clear that disconnects like we have today between (over-inflated) asset prices and the underlying (contracting) economic reality always result in crisis – either a deflationary repricing, or a destruction of the purchasing power of the currency.

Michael shares the 20 financial and economic metrics on the dashboard of indicators he tracks to determine where we are in this story, and which outcome is looking most likely to happen when. This week’s interview is worth listening to for that list alone.

Not one to mince words, Pento believes this is the most treacherous time ever for investors – which means those blindly long the current melt-up will get slaughtered if indeed the risks he predicts play out. As always, we recommend working in partnership with an independent financial advisor who appreciates these risks, prioritizes preservation of your investment capital, and can help you chart the turbulent waters ahead when the reckoning arrives:

")

And if you’re one of the many readers brand new to Peak Prosperity over the past few months, we strongly urge you get your financial situation in order in parallel with your ongoing physical coronavirus preparations.

We recommend you do so in partnership with a professional financial advisor who understands the macro risks to the market that we discuss on this website. If you’ve already got one, great.

But if not, consider talking to the team at New Harbor. We’ve set up this ‘free consultation’ relationship with them to help folks exactly like you.

This is a companion discussion topic for the original entry at https://peakprosperity.com/market-update-overstimulated/

{kind=link}