Note: With so much going on with Europe's debt crisis, the continuing disaster and economic contraction in Japan, and the potential for a very hard landing in the Chinese growth miracle (which is in the running as my favorite "black swan candidate" for 2011), I am going to return our attention to oil in this report. The next report will assess the developing and unfolding debt crisis that will drag down most of the developed economies at some point, and this report will provide essential context for understanding why this result is inevitable and when it will occur.

The Next Oil Shock

The only thing that could prevent another oil shock from happening before the end of 2012 would be another major economic contraction. The emerging oil data continues to tell a tale of ever-tightening supplies that will soon be exceeded by rising global demand. This time, we will not be able to blame speculators for the steep prices we experience; instead, we will have nothing to blame but geology.

Back in 2009, I wrote a pair of reports in which I calculated that we’d see another price spike in oil by 2010 or 2011, based on some assumptions about global GDP growth rates, rates of decline in existing oil fields, and new projects set to come online. Given the recent price spike in oil (Brent crude over $126, now at $115) and recent oil supply data, those predictions turned out to be quite solid (for reference, oil was trading in the low $60s at the time).

One part I whiffed on was in my prediction that the world community would have embraced the idea of Peak Oil by now and begun adjusting accordingly, but that’s not really true except in a few cases (e.g. Sweden). Perhaps things are being differently and more seriously considered behind closed doors, but out in public the dominant story line concerns reinvigorating consumer demand, not a looming liquid fuel crisis.

How the major economies can continue proceeding with a business-as-usual mindset given the oil data is really quite a mystery to me, but that’s just how things happen to be at the moment.

At any rate, with Brent crude oil having lofted over $100/bbl at the beginning of February and remained above that big, round number for four months now, we are already in the middle of a price shock. It may not be a perfect repeat of the circumstances of the 2008 oil shock, but it's close enough that the risk of an economic contraction, at least for the weaker economies, is not unthinkable here. Japan, now in recession and 100% dependent on oil imports, comes to mind.

Looking at the new data and reading even minimally between the lines of recent International Energy Agency (IEA) statements, I am now ready to move my ‘Peak Oil is a statistically unavoidable fact’ event to sometime in 2012, which tightens my prediction from the prior range of 2012-2013.

Upon this recognition, the next shock will drive oil to new heights that are currently unimaginable for most. First, $200/bbl will be breached, then $300, and then more. And these are in current dollar terms; any additional dollar weakness will simply be additive to the actual quoted price. By this I mean that if oil were to trade at $200 but the dollar lost one half of its value along the way, then oil would be priced at $400.

Stampeding Into a Box Canyon

In 2009, I wrote a special report on oil that explored the interplay between energy and the economy. At that time, the stock market was in the tank, global growth was in a freefall, and things looked gloomy.

But I knew that thin-air money is not without its charms and that we’d experience a rebound of sorts. Here’s what I wrote:

I am of the opinion that these trillions and trillions of dollars, which, along with their foreign equivalents, are being applied to “ease the credit crunch,” will eventually find their mark and deliver what feels like a legitimate rebound in activity. All those trillions have to eventually go somewhere and do something.

For now, debts are defaulting faster than the various central banks and governments can inject new money and borrowing activity into the system. Banks aren’t lending because there are very few compelling loans to make, especially if future losses have to actually be carried by the bank making the loan.

But this won’t be true forever. Sooner or later, all the trillions of new dollars will trot out of the barn, begin to gallop, and then thunder off, creating the appearance of a healthy advance.

It will be a cruel illusion, though, as this stampeding herd of money is headed straight into a box canyon.

Money is only one component of growth. As we’ve strenuously proposed, energy is a necessary prerequisite for growth.

(Source)

Well, here we are a couple of years later, with those trillions and trillions out of the barn and stampeding off trying to create some real and lasting economic growth. As we score these efforts, it appears to us that the amount and type of growth that has been achieved is underwhelming, to say the least.

Housing remains in a serious slump, wage-based income growth is poor, Europe remains mired in a serious debt crisis, Japan has slumped back into recession, and the US fiscal deficit is a structural nightmare. Worse, GDP growth is relatively tepid and would be negative, deeply negative, without all the deficit spending and liquidity measures.

As predicted, all that thin-air money, once released into the wild, had a mind of its own and created a serious bout of commodity inflation, especially in food and fuel, which is now seriously impacting the poor and middle classes.

So it’s hard to call the trillions and trillions ‘well spent.’ I was hoping for better results.

Yet we can’t call the re-flation efforts a complete failure, as we are not in a serious, destructive deflation, and we’ve all been granted a bit more time to get ourselves prepared in whatever ways make sense. The gift of time has been invaluable, and for that I am grateful. But in terms of creating a true and lasting economic miracle? It turns out, once again, that 'printing' money electronically is no more effective than calling in the silver coin of the realm, making each unit slightly smaller, and then re-issuing it. Real economic growth has not been created.

What has happened is that false demand, spurred on by trillions in thin-air money, has also spurred on renewed demand for oil, hastening the day that a geologically inspired supply/demand mismatch will finally arrive.

We are driving at a high rate of speed into a box canyon.

World Crude Supply

Before we get into the specifics of where I think the immediate trouble lies in the world oil data, let's take a moment to look at the big picture.

There are a number of ways to look at the petroleum data. The one I prefer to look at is something called 'crude + condensate' (C+C), which leaves out things like ethanol and natural gas liquids, both of which are converted to 'barrel of oil equivalents' (BOE) and added to the C+C to yield total liquid fuels. The reason I like to focus on C+C is that this is mainly conventional oil, the cheap and easy stuff, and it gives us a better idea of where we are in the Peak Oil story.

Note: This next cluster of charts comes from data from the U. S. Energy Information Administration (EIA) that I am, frankly, uncomfortable with, so take them all with a grain of salt. The EIA upwardly revised the data for 2010 and added between 750,000 and 800,000 barrels per day of production to each month. This is the largest upward revision of which I am aware, and it's not yet clear to me why this occurred. Further, the EIA obtained some of that data from IHS, which is the parent company of CERA, the organization that best qualifies for the 'influential Peak Oil deniers of the decade' award.

And somewhat ominously, as suspect as the data may be, it has been an important source for decades for analysts, myself among them. Quite recently, the EIA has announced that, due to budget cutbacks, it will immediately terminate the collection and distribution of international energy statistics -- right at the exact moment they are needed most. Ugh. Very disappointing, and all due to a $15 million budget cut. (Source). This echoes the loss of the M3 monetary statistic, which turned out to be a perfect gold-buying signal. If this is a parallel event, it means that now is a great time to take Peak Oil more seriously.

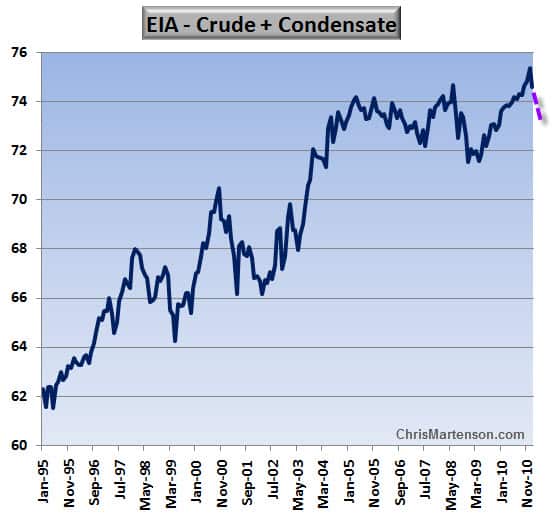

A chart of C+C reveals that the world has been bouncing along in a channel roughly between 72 and 74 mbd since 2005:

Yes, a new high was made in December 2010 and was exceeded in January 2011, offering hope that the world could break out of this limiting band of production, but then production fell back in February due to the Libyan conflict. I have added a purple dotted line to reflect where the data will most likely be for March after subtracting out the Libyan losses and the Saudi cutbacks. As you can see, we will be right back in the 72-74 channel.

Some will be tempted to write this off to a temporary setback due to the unrest in North Africa, but such unrest has always been part of the equation: Iraq, Nigeria, Kuwait, and many other countries have experienced supply disruptions along the way due to war and/or civil unrest.

Note also in this chart that oil production fell off by more than 2 mbd as a consequence of the global recession between 2008 and 2009. From the lows in August 2009, it has since climbed more than 2.4 mbd to its current level.

Where did those gains come from? Can we expect more?

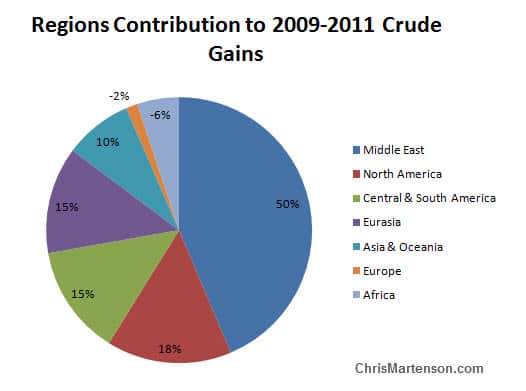

There's a very interesting story in here if we dig down one more layer. This next pie chart shows each region's relative contribution to the gains of 2.4 mbd that happened between August 2009 and February 2011:

In the above chart, I had to include negative percentages for two regions, which is an odd way to display things (how does one draw a negative pie wedge?), but it still all sums to 100%. I've included the negatives for comparison purposes and because they are important to keep in view. It's clear that the Middle East is the most important region; no surprise there. North America is about evenly split in gains between the US (Bakken) and Canada (tar sands), and Russia and China are the major players in their respective regions.

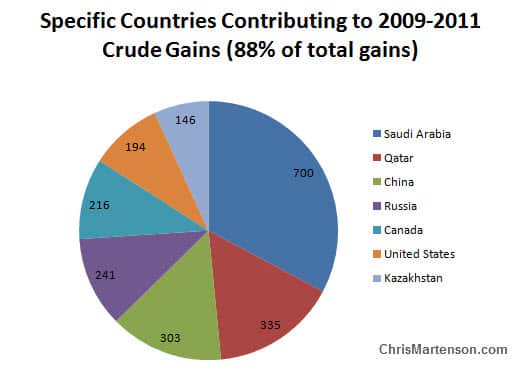

Taking the analysis one level deeper, here are the seven major countries that contributed 88% of the August 2009 to February 2011 gains (in thousands of barrels per day):

Saudi Arabia is the hands-down leader, being responsible for 700,000 barrels per day, or 29%, of the entire gains logged in that period.

There is a variety of interesting sub-stories that could be told across each of the other countries, but it's time to focus on the big fish.

Saudi Arabia – Where There's Smoke, There's Fire

Something is seriously wrong with the signals coming from the Kingdom of Saudi Arabia (KSA), and I am of the opinion that KSA is having geological difficulties that are preventing it from pumping more oil. Said plainly, I am of the mind that the KSA is already at peak.

One troubling bit of information is that Saudi Arabia justified its lowered oil output for March by claiming that the oil markets are oversupplied, even as Brent crude was perched above $120/bbl. There are several possibilities here:

- There really is an oil glut, and the KSA is being truthful.

- There is an oversupply, but only of the heavier, poorer grades of oil that the KSA has in relative abundance.

- The KSA can produce more, but doesn’t want to, preferring to withhold oil production in the interest of receiving higher prices.

- The KSA is already past peak and cannot pump more, despite its best efforts, and the oversupply issue is really just a cover story for the fact that the KSA cannot pump more even if it wanted to.

Let’s start at the beginning of this odd tale. Early in May, the KSA said this:

Saudi lifts April oil output to 8.5 mln bpd-sources

May 01, 2011

DUBAI/KHOBAR, Saudi Arabia, May 1 (Reuters) - Saudi Arabia's crude oil output edged back up in April to around 8.5 million barrels per day (bpd) from roughly 8.3 million bpd in March as demand picks up, Saudi-based industry sources said on Sunday.

The kingdom slashed output by 800,000 bpd in March, due to oversupply, oil minister Ali al-Naimi said last month, adding that he expected production in April to be a little higher than March's level.

So the story here is that the KSA claims to have 12.5 mbd of total capacity. Therefore, meeting the Libyan shortfalls of 1.3 mbd should be simple enough; just open the taps and let it flow. Yet the KSA barely cracked the 9 mbd mark, briefly, before falling back to 8.3 – 8.5 mbd, telling the world that this was a purposeful response to markets that were oversupplied. That's one possibility.

Several analysts thought that perhaps the KSA was simply gaming the markets and trying to obtain the best possible prices:

Saudi unlikely to lift oil output quickly

May 3, 2011

WASHINGTON — Saudi Arabia is unlikely to boost oil production quickly to ease the rise of crude prices, because it needs high prices for its own increased spending, analysts at an international banking think tank said Tuesday.

After producing 8.6 million barrels a day in 2010, the world's leading oil supplier will only kick up production to about 8.9 million barrels this year, said analysts at the Washington-based Institute of International Finance.

"So far the production of crude oil in Saudi Arabia for the first quarter was around 8.7, 8.8 (million barrels a day). And recently some unconfirmed reports said that production dropped in March," said Garbis Iradian, the IIF's deputy director for Africa and the Middle East.

"So we don't expect crude oil production in Saudi Arabia will rise over nine million barrels a day," he said.

While it's possible that the KSA production limitations are a matter of trying to engineer higher prices, one person I trust is Sadad Al-Husseini. The former Aramco engineer, who has a lot of credibility in these matters, thinks that the production limits have more to do with the grades of available oil rather than any mercenary market tactics on the part of KSA.

Saudi Sweet Oil Supply Too Low to Offset Libya, al-Husseini Says

May 17, 2011

Saudi Arabia, the world’s biggest crude exporter, won’t be able to produce enough low-sulfur blends to replace lost Libyan output for refiners in Europe, said Sadad al-Husseini, a former Saudi Aramco executive.

The country doesn’t have enough Arab Super Light to create sufficient amounts of low-sulfur, or sweet, oil similar to Libya’s grades, al-Husseini, Aramco’s former executive vice president for exploration and development, said today by e-mail.

The basic problem is that each refinery is geared for a specific and relatively narrow band of crude oil feedstocks, with the specific gravity and sulfur content being the most critical factors. So it is not as simple as the KSA pumping more heavy sour crude to offset the lost Libyan production. This is yet another possible explanation, and it is far more believable to me than either oversupplied markets or a pricing strategy.

The somewhat shocking news that followed just a few days after the above article was the begging by the IEA for OPEC to lift production. Such a frank admission or plea has never been made before. Reading between the lines, we can suspect that a serious supply shortage is looming if more oil does not find its way to market soon.

International Energy Agency Urges Oil Producers to Lift Output

May 19, 2011

PARIS — Expressing “serious concern” about elevated crude prices, the International Energy Agency on Thursday called for an increase in world oil production. It was an unusual move that highlighted consumer countries’ frustration at the failure of oil-producing nations to lift output in the face of rising demand and tighter supply.

(...)

The agency’s monthly Oil Market Report, respected by industry practitioners, has recently been warning about tightening market conditions as supply has not caught up with strong demand.

Despite commitments from Saudi Arabia, the biggest producer, to use its spare capacity to increase output and replace the supplies lost because of the uprising in Libya, the cartel’s production is now running 1.3 million barrels a day below the level seen before the crisis, according to the I.E.A.

Although the New York Times has positioned this unusual call by the IEA as perhaps a bit of political maneuvering, I feel they missed the real picture by not spending more time characterizing the mismatch between supply and demand. If that's true, then we have a near-perfect repeat of the 2008 situation, where, in the six quarters preceding the oil price spike, demand exceeded supply in five of those quarters.

Confirming this view recently was Goldman Sachs' energy division, which said:

While near-term downside risk remains as the oil market negotiates the slowdown in the pace of world economic growth, we believe that the market will continue to tighten to critical levels by 2012, pushing oil prices substantially higher to restrain demand.

Events in the Middle East and North Africa are having a persistent impact, which leads us to increase our oil price targets. We expect that the ongoing loss of Libyan production and disappointing non-OPEC production will continue to tighten the oil market to critically tight levels in early 2012, with rising industry cost pressures likely to be felt this year.

We are now embedding in our forecasts that Libyan production losses will lead to the effective exhaustion of OPEC spare capacity by early 2012. Consequently, we are raising our Brent crude oil price forecast to $115/bbl, $120/bbl, and $130/bbl on a 3, 6, and 12 month horizon.

(Source)

There’s a lot in there, including the idea that the unrest in the Middle East will be persistent, that non-OPEC production will continue to disappoint (which it should, as nearly every non-OPEC country is past peak), and that the more globally relevant Brent contract is the right one to quote now when discussing oil, not the US-centric WTIC contract.

So count Goldman Sachs among those that are now calculating an imminent supply-demand mismatch.

The End of Easy Oil

The really big news is that the Wall Street Journal finally ran an oil piece (on the front page, no less) acknowledging the difficulties involved in Saudi Arabia regarding oil production and the extraordinary efforts that are now underway to boost production by unlocking their remaining heavy oil reserves.

The critical parts in this story revolve around the costs of getting this oil out of the ground (in terms of both energy and money), the decades it will take to get the oil out, and the clear implication that going after such oil tells us everything we need to know about where we are in the Peak Oil story in general (and specifically in Saudi Arabia). All the better, easier, cheaper grades are already drilled and in production. This is what's left:

Facing Up to End of 'Easy Oil'

WAFRA, Kuwait—The Arabian Peninsula has fueled the global economy with oil for five decades. How long it can continue to do so hinges on projects like one unfolding here in the desert sands along the Saudi Arabia-Kuwait border.

Saudi Arabia became the world's top oil producer by tapping its vast reserves of easy-to-drill, high-quality light oil. But as demand for energy grows and fields of "easy oil" around the world start to dry up, the Saudis are turning to a much tougher source: the billions of barrels of heavy oil trapped beneath the desert.

Heavy oil, which can be as thick as molasses, is harder to get out of the ground than light oil and costs more to refine into gasoline. Nevertheless, Saudi Arabia and Kuwait have embarked on an ambitious experiment to coax it out of the Wafra oil field, located in a sparsely populated expanse of desert shared by the two nations.

That the Saudis are even considering such a project shows how difficult and costly it is becoming to slake the world's thirst for oil. It also suggests that even the Saudis may not be able to boost production quickly in the future if demand rises unexpectedly. Neither issue bodes well for the return of cheap oil over the long term.

The whole story is worth a read. I’ve excerpted quite a bit because there’s so much important information in there that I wanted you to see. Most importantly, the mainstream media in the US is finally waking up to the idea that all of the cheap and easy oil is gone.

They’ve not yet gotten to the appreciation of the idea of Net Energy, which is the real key to understanding why the future will not resemble the past, but they are edging ever closer. And they are beginning to circle around the idea that depletion in the fields that have driven the world’s economy for the past 50 years is a critical reality.

It’s not much of a hop, skip, and a jump from there to seeing it finally named for what it is: Peak Oil, otherwise known as the geological reality that will resist all efforts at human ingenuity and technology because it is a matter of finite limits, not of willpower or optimism.

One thing I thought the article did an especially good job of was actually delving into the engineering realities involved in the project. The article continues:

The Wafra project, however, is far more of a challenge than traditional steam projects. As in most of the Middle East, the oil at Wafra is trapped in a thick layer of limestone that also contains minerals that can build up inside pipes and corrode equipment.

An even bigger challenge is getting the two crucial elements for generating steam: water and a source of energy to boil it. Most successful steam projects are in places with easy access to relatively pure water and a cheap fuel source, usually natural gas. Saudi Arabia and Kuwait have little of either.

With no fresh-water sources in the Arabian desert, Chevron has been forced to use salt water found in the same underground reservoirs as the oil. That water is full of contaminants that must be removed before it can be boiled and injected into the ground.

Finding the energy to boil the water will be even tougher. Chevron could use oil instead of natural gas—literally burning oil to produce oil—but that would burn profits, too. So the company likely will be forced to import natural gas from overseas, an expensive process that involves chilling it to turn it into a liquid, then shipping it thousands of miles.

Some experts are shaking their heads.

The hurdles include mineral buildups, corrosion, water impurities, and the energy costs of heating all that water into steam. In short, getting this stuff out of the ground is going to be far more difficult and costly than prior efforts. End of story.

The reality involved in getting at the non-conventional oil is really just a story of declining net energy; the red curtain will extend down into the luscious green space that represents the surplus energy available to society. Less net energy means less economic activity and complexity. It means less growth. Below a certain level, it means no growth at all. And eventually it means persistent negative growth, a possibility not yet priced into any financial markets.

In some cases I have my concerns about whether these heroic efforts are worth the trouble at all. Perhaps we should invest the same amount of energy, talent, and expertise in energy conservation efforts and technological development.

At this point in the timeline, it's imperative for each of us to ask ourselves: how well prepared are we for this post-Peak Oil future? Part II of this report: How To Position for the Next Oil Shock explores the probable impact the next energy crisis will have on key asset classes, employment, and society in general. As we've shown above, we likely have little time left. Use it wisely.

Click here to access Part II: How To Position for the Next Oil Shock (free executive summary; paid enrollment required to access).

This is a companion discussion topic for the original entry at https://peakprosperity.com/past-peak-oil-why-time-is-now-short-2/