Originally published at: https://peakprosperity.com/sovereign-bonds-are-flashing-an-urgent-warning/

There are creakings and popping and various groanings emitting from the global financial system. While precious equities seem to constantly catch bids as they move ‘up and to the right,’ bonds are behaving very differently.

They are selling off. And have been for long enough that even the WSJ has taken notice:

The US 10-year yield recently hit 4.69% up from a low of 3.95% before the Iran War started.

But the rout in bond prices is not contained to the US, it exists across Europe and Japan too.

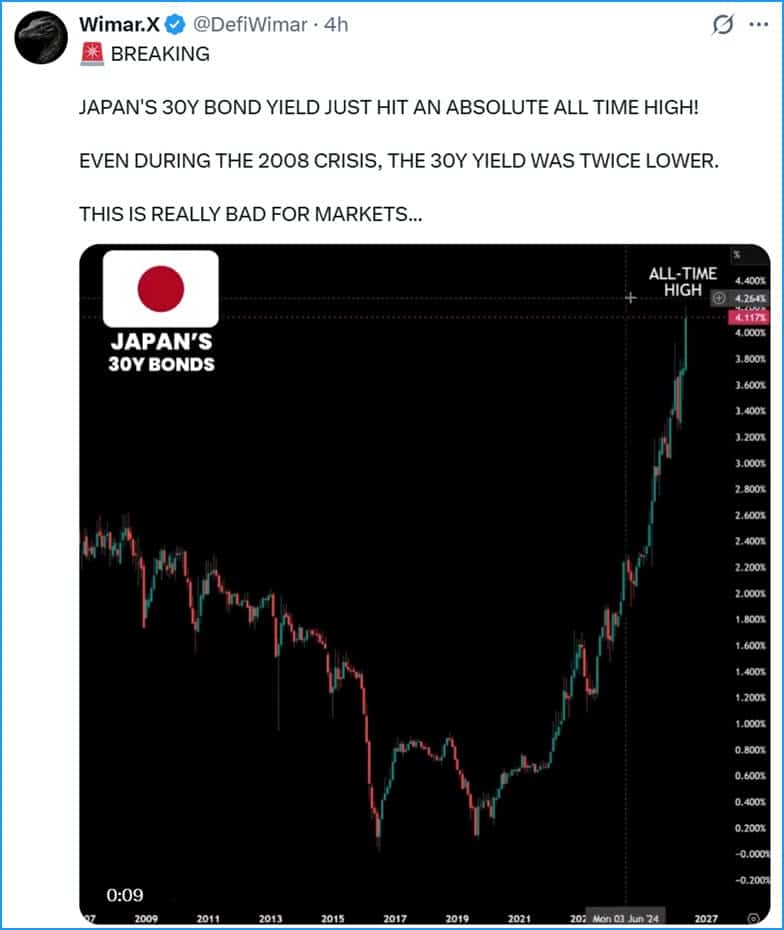

Japan, is in what appears to be deep trouble at the moment. Not only is the yen under tremendous pressure due to heavy fiscal deficits proposed by the current administration, but Japan imports 100% of its oil and oil products from abroad. As oil becomes more expensive, the outflow of yen accelerates.

Coupled to that dynamic are Japanese bonds which have been selling off viciously, as exemplified by their 30-year bond:

Higher government bond yields, of course, mean higher government interest costs which is another source of pressure on the yen.

But Japan is not alone. The UK is under quite comparable pressures, and its own 30-year bond is absolutely screaming distress.

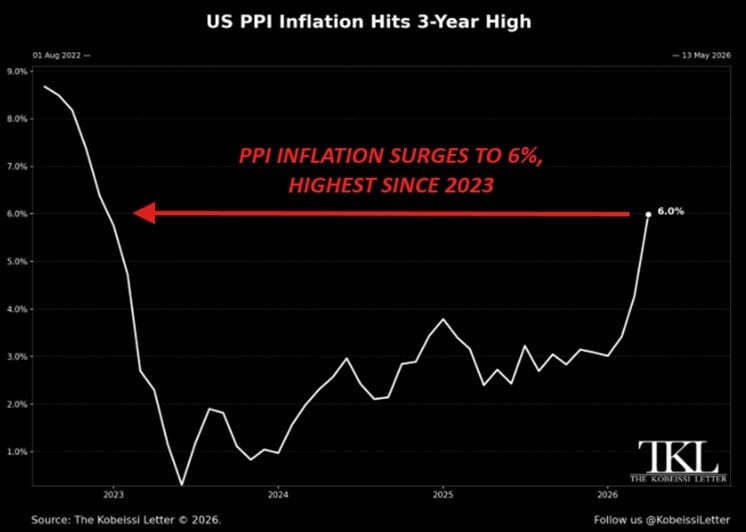

While there are several factors at play, Paul and I believe the biggest of them is the resurgence of inflation. Every indication points to inflation both heading higher and picking up speed.

In the US, producer price index (PPI) is heading north rapidly and now stands at 6%(!).

With history as our guide, the means that the headline consumer price index (CPI) will be flirting with 6% in about 3-4 months.

Obviously, nobody wants to hold bonds paying 4% is a world of 6% inflation. That’s just a guaranteed loss of purchasing power. Which explains why bonds are selling off.

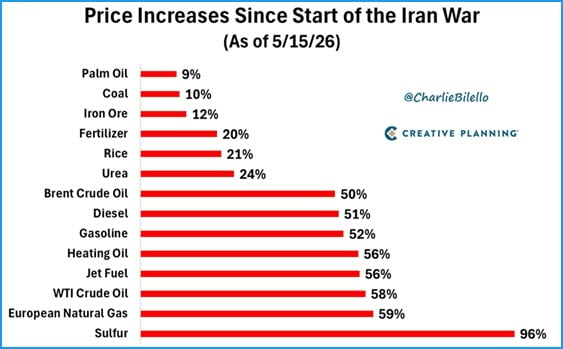

But it could get a hwole lot worse, and both Paul and I expect it to because (a) input prices are already in high to very high double digits and (b) the Strait of Hormuz is not open, and the negotiations are going poorly.

Ouch!

What the even…?

Add it all up, and it’s clear that a set of major regime changes are underway; the 40-year downtrend in interest rates has been broken and sustained, we’re in a structural energy crisis, and US leadership seems either unable to address the core predicaments, or are unwilling for some reason.

Despite all that, opportunities do exist for adaptive investors in undervalued areas (commodities, energy, emerging markets), but passive strategies and long bonds face what we feel are underappreciated risks.

That’s where having a strong financial plan, a good strategy, and a disciplined risk-managed approach are going to be vital to your future success.

Timestamps

00:34 The Bond Market’s Current Landscape

05:58 Inflation’s Impact on Retirement Planning

10:15 The Changing Dynamics of Real Estate Investment

15:23 Insurance Challenges in Property Management

19:45 Global Bond Market Trends and Their Implications

23:25 The Role of Inflation in Economic Predictions

31:34 Navigating the Yield Curve and Inflation Risks

36:37 Understanding the Debt Bubble and Market Predictions

43:40 The Impact of Oil Prices on the Economy

56:40 Energy Demand and Future Projections

01:01:40 Long-Term Energy Strategies and Market Trends

01:04:55 Market Valuations and Historical Context

01:06:56 Margin Debt and Market Risks

01:08:34 Investor Psychology and Market Discipline

01:12:17 The Role of Government and Central Banks

FINANCIAL DISCLAIMER:

The information contained in this video and the resources available for download through our affiliated website are not intended as and shall not be understood or construed as financial advice, nor should be interpreted as a solicitation to sell or offer to sell investment advisory services. No person who currently works for or contracts with Peak Prosperity or Peak Financial Investing is an attorney or accountant, nor are we holding ourselves out to be, and the information contained in the video and on the website is not a substitute for legal or tax advice from a professional who is aware of the facts and circumstances of your individual situation. While Peak Financial Investing is a registered investment advisor, please note that this podcast is not intended to be investment advice.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. We have done our best to ensure that the information provided is accurate and provides what we feel is valuable information. The views expressed are subject to change based on market and other conditions.<

No guests or clients appearing on the podcast receive any form of compensation for their appearance and obtained no other benefit from either Peak Prosperity or Peak Financial Investing.

All investing involves risks including the possible loss of capital. Asset allocation and diversification does not ensure a profit or protect against loss. Please note that out- performance does not necessarily represent positive total returns for a period. There is no assurance that any investment strategy will be successful. All investments carry a certain degree of risk. Dividends are not guaranteed, and a company’s future ability to pay dividends may be limited.

Additional important disclosures for Peak Financial Investing may be found in our Form ADV Part 2A, which can be found at https://adviserinfo.sec.gov/firm/summary/319672.