Originally published at: https://peakprosperity.com/the-big-print-how-to-survive-the-coming-inflationary-times/

For this week’s Finance U episode, I had the privilege of interviewing Lawrence “Larry” Lepard, an investment manager at Equity Management Associates LLC, a sound money advocate, and author of the new book The Big Print.

“Fix the money, fix the world,” Larry says, echoing my own view that fiat money is corrupt by its very design.

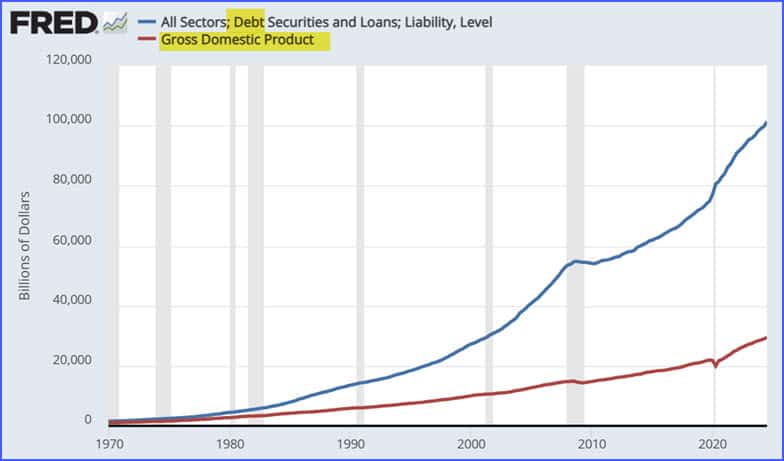

The US is on an unsustainable fiscal trajectory, and that can be determined simply by as looking at this one chart of GDP (red) and total debt in the US system (blue):

As I am fond of saying, you cannot grow your debts faster than your income forever.

In Lepard’s book, this gap aligns with Stein’s Law: “If something cannot go on forever, it will stop.” Larry’s view is that there’s always a chance things could turn around, but in this case, that would require thoughtful and brave leadership to suddenly emerge who would be willing to lead people through a very painful period of readjustment.

How likely is that?

It’s a Moral Issue

Both Larry and I have been tracking the fiscal and monetary issues for a long time. And it’s downright frustrating to watch the Fed and the US government double and then triple down on their middle-class ruinous policies while pretending to care about the average person.

The Fed enabled and juiced every crisis through its interventionist zero-interest-rate policies (ZERP) and quantitative easing (QE).

By printing money into existence, the Fed cheats everybody who has to work for their money. And there was no grander period of cheating than that performed because of the Covid “emergency.”

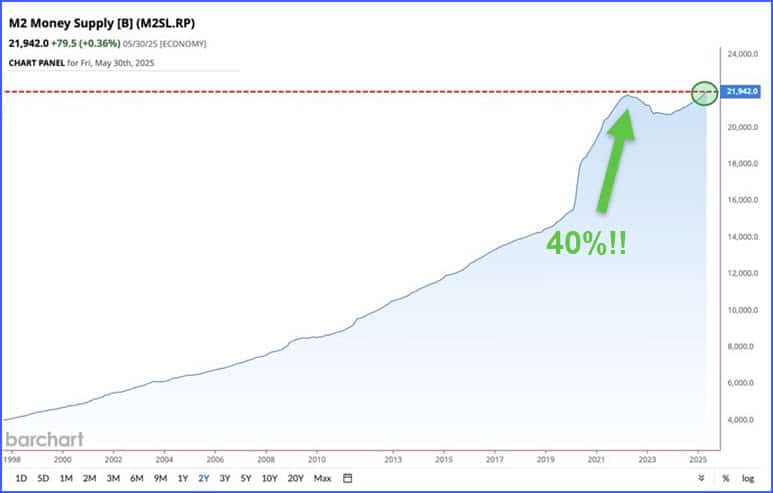

Every single saved dollar in existence was cut by 40% when the Fed printed up 40% more dollars in just 2 years:

This is no different than reaching into everybody’s savings account and removing 40% of their purchasing power. Instead, it is called inflation and we’re all suffering at the grocery store, with our insurance premiums, and real estate tax hikes.

In other words, it’s immoral.

Big Players Starting to Get Twitchy

Notably, lots of big financial insiders are starting to get worried. They are beginning to say the same sorts of things that Larry Lepard has been saying for years. Ray Dalio of Bridgewater Assocaites, is saying that this all ends very badly:

History tells us the preferred path for government policymakers trying to deal with too much debt is lowering interest rates and devaluing the currency the debt is denominated in.Doing this is a very hidden way of reducing wealth, because as your currency goes down, it makes it… pic.twitter.com/F6O60CogZG

— Ray Dalio (@RayDalio) July 3, 2025

Jamie Dimon the CEO of JPMorgan has warned that the bond market may crack:

I guess we don’t need to say it anymore.-Jamie Dimon, CEO of JPMorgan Chase “You are going to see a crack in the bond market, okay. It is going to happen” pic.twitter.com/GRMYWN8tAd

— Vandell | Black Swan Capitalist (@vandell33) May 31, 2025

While Elon Musk is all over “X” saying that the US fiscal situation is going to end in disaster:

And Jerome Powell is on record saying over and over again that the US government is on a fiscally unsustainable path.

When the big boys start to get twitchy, it’s time to get defensive.

Call To Action

There’s nothing the average person can do about the Federal Reserve or the federal government’s policies and actions. But we can protect our wealth by moving it into hard assets. Larry says that anybody who doesn’t move at least 20% of their wealth/savings into hard assets will come to regret that decision over the coming years.

The Federal Reserve is going to print and then print some more. Hence the name of Larry’s book The Big Print. He believes the next Big Print episode will take the Fed’s balance sheet from ~$7 trillion to between $15 trillion and $30 trillion. Inflation is going to rip higher and higher into the social structure, claiming new victims from ever-higher rungs of the socioeconomic ladder.

I urge listeners to read The Big Print, follow Lepard at @LawrenceLepard on X, and visit EMA2.com for his quarterly insights. At Peak Prosperity and Peak Financial Investing, we’ll continue advocating for financial resilience. Let’s end the Fed’s grip on our money and rebuild a system that works for all.

FINANCIAL DISCLAIMER. PEAK PROSPERITY, LLC, AND PEAK FINANCIAL INVESTING ARE NOT ENGAGED IN RENDERING LEGAL, TAX, OR FINANCIAL ADVICE OR SERVICES VIA THIS WEBSITE. NEITHER PEAK PROSPERITY, LLC NOR PEAK FINANCIAL INVESTING ARE FINANCIAL PLANNERS, BROKERS, OR TAX ADVISORS. Their websites are intended only to assist you in your financial education. Your personal financial situation is unique, and any information and advice obtained through this website may not be appropriate for your situation. Accordingly, before making any final decisions or implementing any financial strategy, you should consider obtaining additional information and advice from your accountant or other financial advisers who are fully aware of your individual circumstances.