Global Slowdown

The U.S. economy weakened appreciably in the first quarter of 2013. But what if this weakness persists into the second quarter just completed, and worsens still in the second half of this year?

Q1 GDP, as reported on June 26th, was revised lower to just 1.8%. And various indications suggest that Q2 could come in slightly lower still, at 1.6%. Might the U.S. economy be guiding to a long-term GDP of 1.5%? That’s the rate identified by such observers as Jeremy Grantham – the rate at which we combine aging demographics, lower fertility rates, high resource costs, and the burdensome legacy of debt.

After a four-year reflationary rally in just about everything, and now with an emerging interest rate shock, the second half of 2013 appears to have more downside risk than upside. Have global stock markets started to discount this possibility?

As explained in my last piece, Marking the Four-Year Reflationary Rally (May 6, 2013) the stock market in 2013 was starting to become decoupled from the economy. What looked like a blow-off top in global equities has so far turned out to be just that - especially with the help of Japan’s Abenomics-driven Nikkei, which came close to doubling in just six months' time, from late 2012 to early 2013. As usual, however, the Fed has made a rather big call on future growth at a key moment, and has begun to advertise or hint at the tapering of quantitative easing (QE), possibly as early as this year. Here was the Fed’s forecast for growth, announced just one week before the recent downward revisions to GDP:

The Federal Reserve projects that the unemployment rate could fall to 6.5% in 2014, a threshold it has conditionally set to begin raising interest rates. Still, most Fed officials expect to hold off on a rate increase until 2015, according to assessments of monetary policy for the coming years that showed 15 of 19 officials expect the first tightening will come that year. The latest unemployment and economic-growth forecasts for 2014 are an upgrade from the last set of estimates, made in March. The projections reflect officials’ expectations and hint at their next monetary-policy moves... For 2014, Fed officials boosted their outlook on gross domestic product growth to 3.0% to 3.5%, versus a 2.9% to 3.4% estimate made in March.

The Fed sees much stronger growth and lower unemployment in 2014. Notably, the Fed's estimate of 2013 GDP, in the range of 2.3% to 2.6%, still looks rather high. But why this particular forecast now? Or more to the point, why start a tightening cycle now? The Fed has a habit of being chronically wrong and then notably wrong at turning points. Is this really the best time to change course?

The simple answer is that the Fed has normalcy bias. As an institution, it’s particularly weak on natural resources and ecological economics, and it is much likelier to embrace standard growth models and mean reversion in economic cycles. However, this bias is starting to come under pressure, as the Fed has spent the past 13 years since the Nasdaq bust trying to reflate the U.S. economy.

No sooner had the Fed, indicated more confidence in the U.S. growth outlook in its most recent June meeting than skies darkened in Europe, emerging markets, and new volatility appeared in U.S. markets. Justin Lahart at the Wall Street Journal noted that the Fed forecast for the 2H of 2013 suddenly looks very far away:

Macroeconomic advisers says 2Q gdp tracking 1.4%, saar. So now economy only needs to grow 3.4% in second half to hit Fed's forecast!

~ Justin Lahart (@jdlahart) June 27, 2013

The Interest Rate Shock

Most agree: The recent stream of communication coming from the Fed is unclear, contradictory, and voluminous.

Despite the Fed's mish-mash of signaling, however, we’ve now obtained some useful insight from the back-up in rates as Treasury bond prices have recently fallen hard. Without the Fed constantly on the bid in the Treasury market, the yield on the 10-year Treasury note would still be low, given the weakness in the economy – but it might not be quite as low as many presumed. Remember, many analysts long held the view that the Fed and QE really had no effect on long rates. The market, in their view, was pricing in slow growth, and rates were low because of the collective outlook. Fair enough, but perhaps even during slow growth long rates can’t really be sustained under 2%.

Unsurprisingly, these uncomfortable realizations hit the market very hard in the weeks after the Fed's June meeting. By contrast, during most of the reflationary period since 2009, whenever the Fed threatened to ease the pace of QE, discontinue QE, or was even thought to be vacillating about QE, Treasury bonds would rally in price (and fall in yield), as if the market was answering the Fed and saying “not yet.” Now, however, as rates back up, the market seems to be taking the Fed more seriously and possibly agreeing with the Fed forecast that stronger growth is indeed on the way.

But is stronger growth on the way?

The most recent jobs report, released on Friday July 5th, sent a fresh spasm through the Treasury bond market with the yield on the ten-year note soaring to fresh highs, for the current move, to 2.715%. With a seemingly strong headline number of 195,000 new jobs, and with previous revisions to the upside, the market initially seemed to come into better alignment with a pick-up in growth in the second half of 2013. However, closer examination of the report, in which the unemployment rate held steady at 7.6%, revealed that once again the quality of the jobs being created in the U.S. remains poor. Part-time jobs continued to outpace the growth in higher-wage, full-time jobs. Also, the broader measure of unemployment, U-6, actually rose:

The latest jobs report isn’t quite all roses. Behind the solid payroll gains are a few troubling signs. The number of Americans working part time because they can’t find full-time jobs and the number who want jobs but have given up looking both jumped last month. As a result, a broader measure of unemployment increased a half percentage point in June to 14.3%. That’s the highest level since February and the largest monthly increase since 2009 in that rate, known as the “U-6″ for its data classification by the Labor Department. That measure is among the data points Federal Reserve policy makers say they follow closely...The number of workers employed part-time because they couldn’t find a full-time job increased by a seasonally adjusted 322,000 last month. There were 1 million so-called discouraged workers in June, those who say they are not currently looking for work because they believe no jobs are available for them. That’s an increase of more than 200,000 from a year ago.

The scale of the task ahead is also worth mentioning. The U.S. economy still needs to add millions of jobs to fill the gap left in the wake of the Great Recession. A certain number of jobs each month are required to simply meet the normal demands of present-day population growth. However, to make progress on unemployment, job creation over and above that level must be sustained. Dean Baker at CESP explains, in his piece, Upbeat June Job Report Still Leaves U.S. Economy in a Deep Hole:

The 195,000 new jobs reported for June was somewhat better than most economists had expected. The job gains, together with upward revisions to the prior two months' data, raised average growth for the last three months to 196,000. While this may lead some to be dancing in the streets, those who actually care about the economy may want to hold off. First, it is important to remember the size of the hole the economy is in. We are down roughly 8.5 million jobs from our trend growth path. We also need close to 100,000 jobs a month to keep pace with the underlying growth rate of the labor market. This means that even with the relatively good growth of the last few months, we were only closing the gap at the rate of 96,000 a month. At this pace, it will take up more than seven years to fill the jobs gap. After severe downturns in the 1970s and 1980s, we had months in which the economy created over 400,000 jobs. And this was in a labor market that was more than one-third smaller. That is the sort of job growth that we should be seeing after a recession like the one we saw in 2008-2009. Unfortunately, such growth is nowhere in sight.

Energy Recession in the OECD

Plaguing the U.S. and other western economies is the continued fall in demand for goods, services, and energy. Demand has oscillated since the Great Recession, sometime rising and other times falling, but at much-reduced levels. This lower equilibrium has carried on for years, with Europe pulling the OECD lower, Japan in the middle, and the U.S. struggling to obtain modest but positive growth. However, the whole of the OECD remains in an energy recession. Demand for oil and electricity continues to fall. And while some point to efficiency gains as the explanation, you can't really have meaningful efficiency gains in economies operating in a state of low equilibrium. Rather, in the OECD, it's the raw shedding of demand that has dominated economies over the past five years.

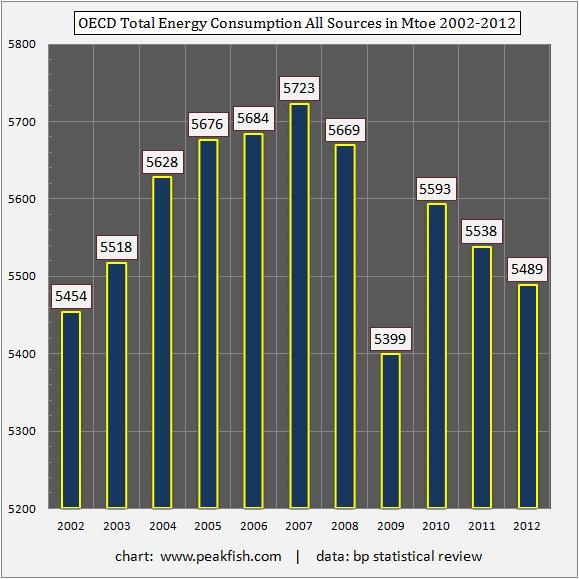

See OECD Total Energy Consumption All Sources in Mtoe (million tonnes oil equivalent) 2002-2012:

As with so many other data points in the OECD, total energy consumption from all sources is back to levels last seen a decade ago, with 2012's demand of 5489 Mtoe a nearly perfect match to 2002. Since 2007, OECD energy consumption has been declining at a little less than a percentage point per year, at an average annual decline rate of -0.83%.

It should not be a surprise, therefore, that GDP has been so weak, or that here in 2013, GDP would oscillate again, this time to the downside. The decline of energy consumption in the OECD is a proxy for lower throughput, lower levels of demand, lower transportation activity, and, of course, lower levels of labor participation. The recent GDP report in the U.S., for example, uncovered the fact that personal consumption of all goods, not just energy, is already turning down. This presents yet another hurdle for those who would forecast a stronger economy – no, a much stronger economy – in the second half in 2013.

Deflation Warnings

Probably the most dramatic market action in the first half of 2013 did not, however, center either in the U.S. or in Europe.

Instead, the titanic launch of the Nikkei under aggressive reflationary policy initially created hope and excitement. But the correction may have created new problems. Indeed, it seems that the OECD central banks (and especially the U.S. central bank) still have not learned a key lesson from the past decade: When you reflate asset prices on top of a stagnant economy and then asset prices begin falling, the ensuing deflation is often worse and certainly more intractable.

The crack in the Nikkei, which nearly reached 16,000 in mid-May, also sent tremors through the foreign exchange complex. The Japanese yen, aggressively devalued by the Bank of Japan all year, backed up considerably. And while the Nikkei has rallied back to the 14,000 level, it's clear that Abenomics is a fairly high-risk game. Interestingly, there seems to be almost universal excitement in the West, and especially in New York, about the prospects for Japan. However, as previewed in February's essay, The Arrival of Japan's Sunset, the idea that Japan can revive its moribund economy against the gravitational pull of imported resource costs and domestic demographics is specious.

Indeed, Japan is engaged in a classic battle with the Red Queen. As it tries to increase exports, it must also increase imports of raw materials. But to do this at the same time the Bank of Japan is pursuing currency devaluation means that Japan is simply running faster to stay in the same place. It would be comical if it were not so tragic. In April, for example, Japan exported ¥5.7 trillion worth of goods. But to achieve such export volumes, Japan had to import ¥2.1 trillion of energy.

Japan, however, is simply a more acute version of the pressures that exist for both the United States and Europe. All three of these OECD giants need exports – which is to say, they need other large economies to trade with them and import their goods. The U.S. has been lucky in this regard, as its exports of commodities from food to coal and petroleum products have soared in recent years. Indeed, exports have functioned as a kind of bright light for the U.S. economy in the period after the Great Recession. But now, notice that the U.S. dollar is soaring – presenting the same kind of problem that has plagued Japan for decades.

In Part II: How To Break Out of Stagnation, we take a look at some of the steps Western governments may take as central banks like the Fed attempt to tighten. Recent communication from the BIS (Bank for International Settlements) indicates that fiscal rather than monetary policy will be the tool going forward, as central banks have perhaps become growth-impatient and frustrated at having to carry the weight of reflationary policy. With the structure of employment participation still at low levels, and with the ongoing energy constraint of expensive oil, what policies might OECD governments undertake to more aggressively put people back to work?

Click here to read Part II of this report (free executive summary; enrollment required for full access).

This is a companion discussion topic for the original entry at https://peakprosperity.com/the-dead-weight-of-sluggish-global-growth/