“We are on the precipice of the greatest retirement crisis in the history of the world. And that makes perfect sense because, first of all, we have the largest elderly population in the history of the world.Just focusing on the United States: our elderly are woefully unprepared to retire. And in the decades to come we will witness millions of elderly Americans, Baby Boomers and others, slipping into poverty. ‘Too frail to work, too poor to retire’ will become the new normal for many elderly Americans.”

So warns forensic pension analyst Ted Siedle.

And Ted knows what he’s talking about.

He’s a former SEC attorney who has testified on pension abuse before the Senate Banking Committee. And in 2017, he secured the largest SEC whistleblower award in history of $48 million, and in 2018, the largest CFTC award in history at $30 million.

Too many of America’s public pensions are dangerously underfunded due to over-promised payouts vs contributions and poor fund performance. And corporate pension funds are in the hole a collective -$50 billion.

ZIRP has pushed these funds out of conservative investments into highly risky and opaque instruments they have no business being in. And that the rosy case, assuming markets continue their current trajectory.

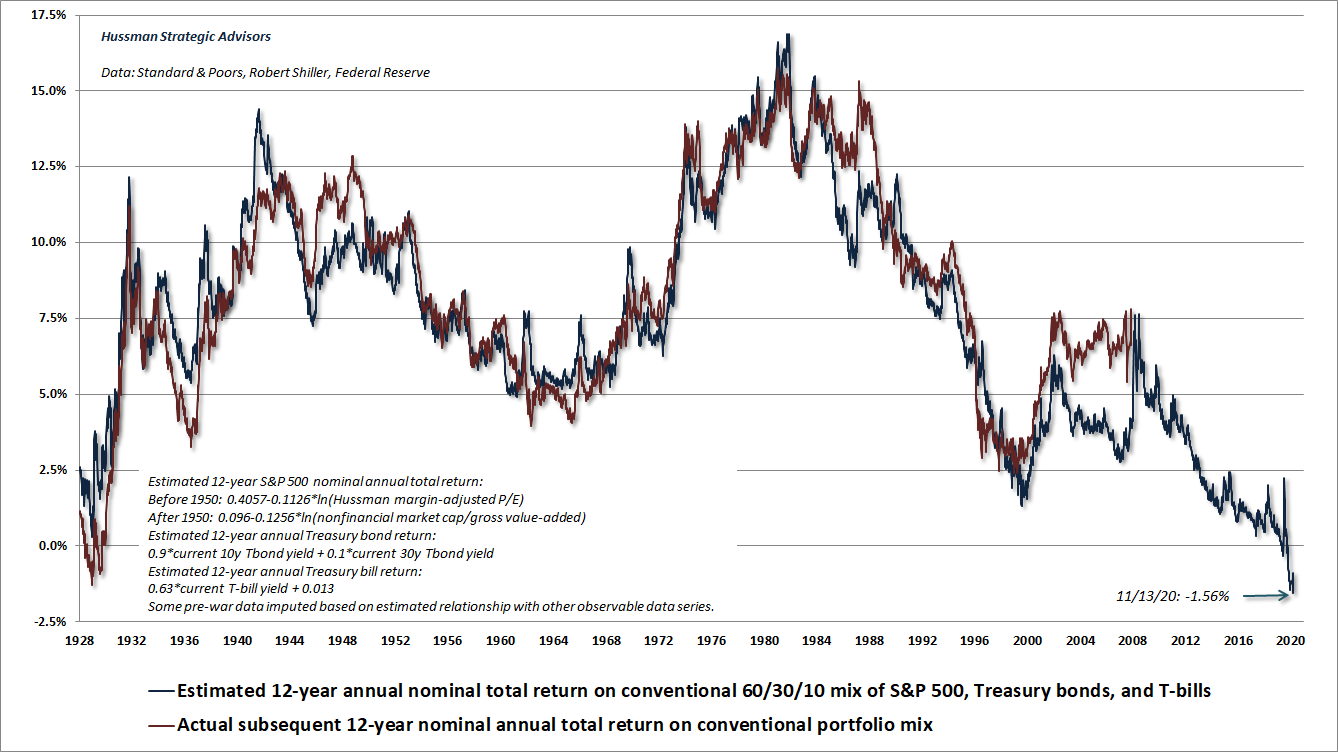

But given how overvalued they are, even just a period of 0% returns (which respectable analysts like John Hussman are waring will be the return over the next 12 years), let alone a sizable market correction, will unleash a catastrophic cascade of collapses across the pension system.

Which is very worrisome to consider when markets are this overvalued:

Ted strongly advises every investor look at their current exposure to these coming pension failures.

If you’re relying on one for your retirement, what will you do if your monthly payment is cut in half or worse? And even if you aren’t, these failures will send shockwaves across every asset class as these funds reduce their buying and perhaps become forced sellers. How vulnerable is your current portfolio to that?

Which is why now, more than ever, is the time to partner with a financial advisor who understands the risks in play, can craft an appropriate portfolio strategy for you given your needs, and apply sound risk management protection where appropriate:

And if you’re one of the many readers brand new to Peak Prosperity over the past few months, we strongly urge you get your financial situation in order in parallel with your ongoing physical coronavirus preparations.

We recommend you do so in partnership with a professional financial advisor who understands the macro risks to the market that we discuss on this website. If you’ve already got one, great.

But if not, consider talking to the team at New Harbor. We’ve set up this ‘free consultation’ relationship with them to help folks exactly like you.

This is a companion discussion topic for the original entry at https://peakprosperity.com/the-great-retirement-threat/

{kind=link}

{kind=link}