Originally published at: https://peakprosperity.com/finance-u-the-not-so-great-economy-and-will-private-credit-be-the-spark-that-kicks-off-gfc-2-0/

Trump keeps saying we’re living in the greatest economy ever, but that’s not supported by the underlying statistics. At all.

Here’s the claim, repeated also in the recent State of the Union speech:

Trump: "I'm popular and I've done well. I think we have the greatest economy, actually, ever in history. We have to get the word out." pic.twitter.com/g4xv06sIhZ

— Aaron Rupar (@atrupar) February 10, 2026

By the numbers, a main reason that the headline GDP number is doing as well as it is (which isn’t all that great), is because the government is deficit spending like drunken sailors.

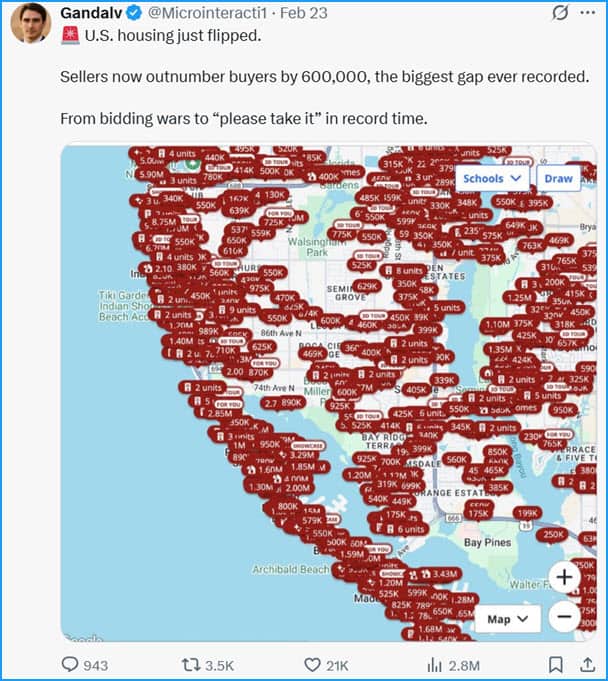

Take away that support and the economy is in a deep recession.Next houses are really wildly unaffordable, making residential real estate one of the largest real estate bubbles in history – larger even than during the GFC.

Take away that support and the economy is in a deep recession.Next houses are really wildly unaffordable, making residential real estate one of the largest real estate bubbles in history – larger even than during the GFC. It looks like gravity has finally caught up to home sales:

It looks like gravity has finally caught up to home sales:

GFC 2.0

Meanwhile, Jamie Dimon of JPMorgan is suggesting that the same sorts of excesses that led to the GFC 1.0 are now in place for a GFC 2.0 repeat:

JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon, asked about fierce competition across the financial industry, said he’s starting to see parallels to the era before the 2008 financial crisis, when a rush to make loans ended disastrously.

“Unfortunately, we did see this in ’05, ’06 and ’07, almost the same thing — the rising tide was lifting all boats, everyone was making a lot of money,” Dimon told investors on Monday. While JPMorgan isn’t willing to make riskier loans to boost net interest income, he said, “I see a couple people doing some dumb things. They’re just doing dumb things to create NII.”

(Source)

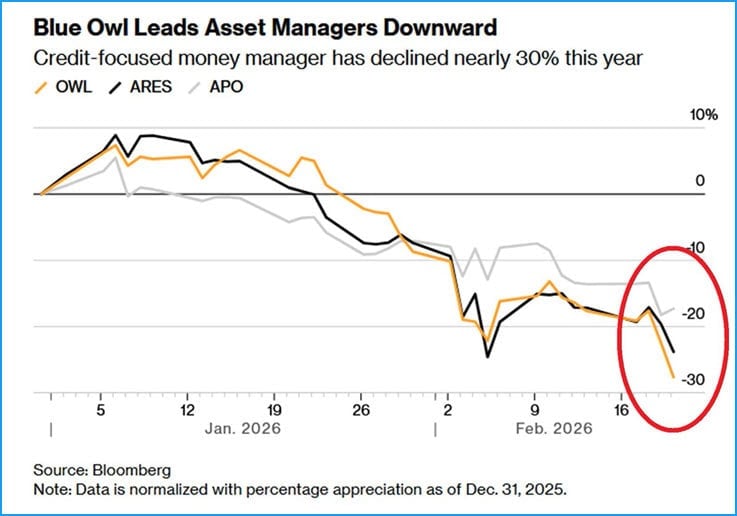

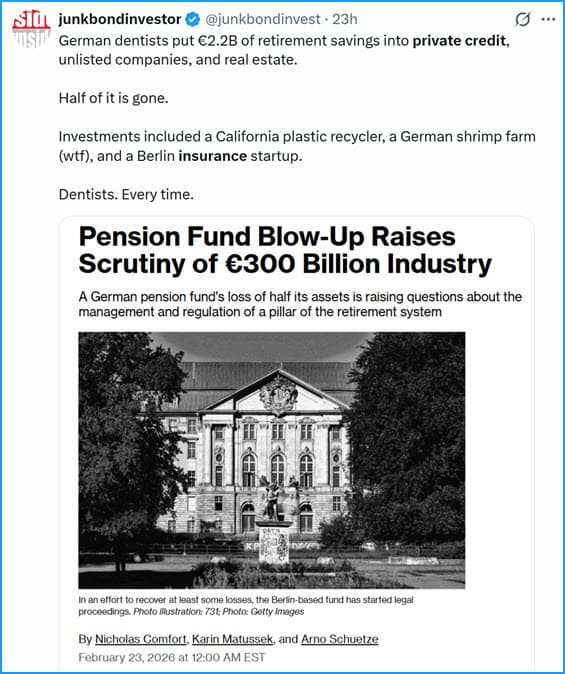

Because history rhymes, this time it looks like the epicenter will be something called ‘private credit.’

Remember, Trump put out an EO last year allowing private credit to be sold into 401k’s and 401k eligible funds. What great timing!

And, just like last time, Wall Street shoveled these defective products out the door as fast as they could once the easy money was stripped out and all that remained was risk.

How it started:

How it’s going:

It’s all just more of the same that brought us the GFC, where no lessons were learned because none of the painful consequences landed on the perpetrators who were bailed out.

All of which is to say, things are looking increasingly dicey out there in the financial world. It’s time to manage risk actively.

Timestamps

00:00 The State of the Economy: A Critical Examination

13:08 Consumer Credit and Economic Pressures

27:20 The Looming Threat of Financial Crisis 2.0

FINANCIAL DISCLAIMER:

The information contained in this video and the resources available for download through our affiliated website are not intended as and shall not be understood or construed as financial advice, nor should be interpreted as a solicitation to sell or offer to sell investment advisory services. No person who currently works for or contracts with Peak Prosperity or Peak Financial Investing is an attorney or accountant, nor are we holding ourselves out to be, and the information contained in the video and on the website is not a substitute for legal or tax advice from a professional who is aware of the facts and circumstances of your individual situation. While Peak Financial Investing is a registered investment advisor, please note that this podcast is not intended to be investment advice.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. We have done our best to ensure that the information provided is accurate and provides what we feel is valuable information. The views expressed are subject to change based on market and other conditions.<

No guests or clients appearing on the podcast receive any form of compensation for their appearance and obtained no other benefit from either Peak Prosperity or Peak Financial Investing.

All investing involves risks including the possible loss of capital. Asset allocation and diversification does not ensure a profit or protect against loss. Please note that out- performance does not necessarily represent positive total returns for a period. There is no assurance that any investment strategy will be successful. All investments carry a certain degree of risk. Dividends are not guaranteed, and a company’s future ability to pay dividends may be limited.

Additional important disclosures for Peak Financial Investing may be found in our Form ADV Part 2A, which can be found at https://adviserinfo.sec.gov/firm/summary/319672.