Originally published at: https://peakprosperity.com/warning-us-petroleum-inventories-are-being-raided/

Many people will be surprised to learn this, but here in April 2026, the US remains a net importer of crude oil.

When a nation is a net importer, logically, it means they have no extra crude oil to export.

The confusion about the U.S.’s energy situation stems from the unfortunate way that the EIA – the US agency responsible for energy reporting – has unhelpfully smashed every hydrocarbon into a single reported number.

Yes, technically, the US is “energy independent” and is a “net exporter of petroleum.” But it is also a net importer of crude oil. Want…what?

It turns out the subject has as much complexity as a medical diagnosis, and the nuance matters. A lot.

Those who take the time to become at least somewhat acquainted with the subject will gain a valuable perspective that will allow them to assess the current risks and opportunities properly.

“Petroleum”

It begins with the idea that the US EIA (the reporting party) has lumped everything into a category they call “petroleum,” which many people think is synonymous with “oil.”

On the basis of “petroleum,” the US is indeed a powerful net exporter, usually on the order of ~ 4 million barrels per day (Mb/d).

But on the basis of crude oil, the US is a net importer of ~ 2 Mb/d.

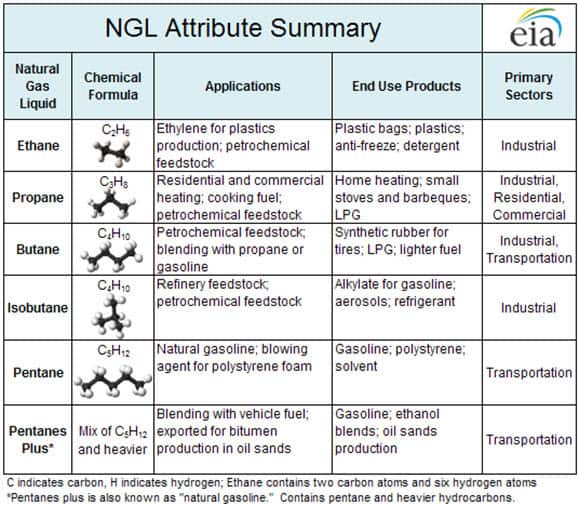

Now we get to the nuance, and we have to dust off a bit of our high school chemistry knowledge to have a proper discussion. The other name for petroleum is hydrocarbons, so named because they consist of hydrogen (H) and carbon (C) (atoms found on the periodic table). Hydrocarbons.

Those atoms can be combined into a dizzying array of molecules, with the simplest of them being a single carbon atom bound to four hydrogen atoms. This is called methane, or natural gas, an exceedingly important hydrocarbon to our industrialized world.

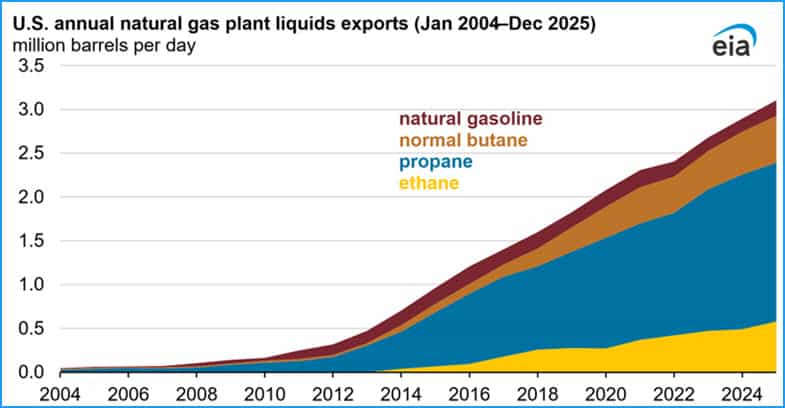

The next in our series would be ‘ethane’, consisting of 2 carbon atoms bound to 6 hydrogen atoms. Ethane is the largest component of “Natural Gas Plant Liquids” or NGPL. The US is absolutely swimming in this stuff, and it is a valuable industrial feedstock mainly going into plastics production.

The US uses all the ethane it can and exports the rest.

The remaining balance of the “NGPLs” consists of propane (3 carbon atoms) butane (4 carbon atoms) and pentane (5 carbon atoms).

Each of these compounds is valuable and useful. None of them is what we’d call “oil.”

Because of shale fracking, the US is absolutely swimming in these NGPL molecules, using what it can industrially and selling the rest.

But make no mistake; these NGPL molecules are not synonymous with oil. At all.

They cannot be refined into jet fuel, diesel, fuel oil, or asphalt. That’s what actual crude oil is for.

It is no overstatement to say that the world runs on jet fuel, diesel, and fuel oil. Those are the substances of prosperity and commerce.

For some reason, the EIA has elected to pour NGPLs and Crude Oil into one useless bucket of reporting. This can only be for political/PR purposes, as there is no usefulness to industry, analysts, or investors to be found in that sloppy pool. Sure it sounds great (PR) to state that “the US is energy independent,” but that masks the fact that the US has too much of some things and too little of others.

Vessels Inbound For The US

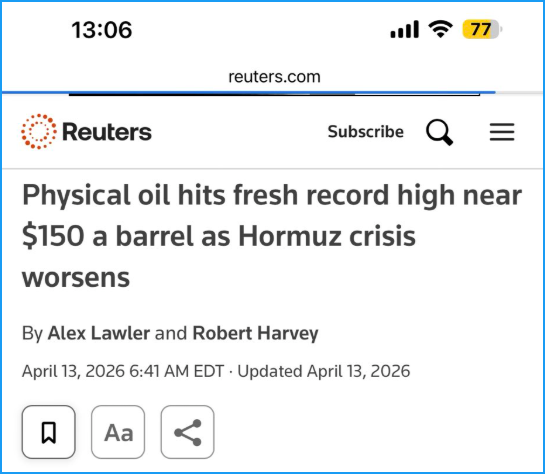

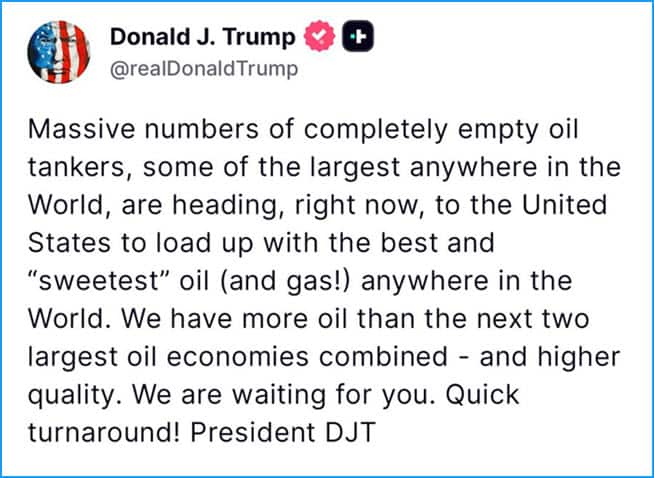

With that as background, we can now turn to the recent news that a huge number of oil tankers are steaming toward the US to load up with oil, which Trump has suggested can meet the world’s needs (spoiler: it cannot).

While it is true that a record number of empty tankers are headed to the US, so too are fully loaded tankers (coming from where, we wonder?)

![]()

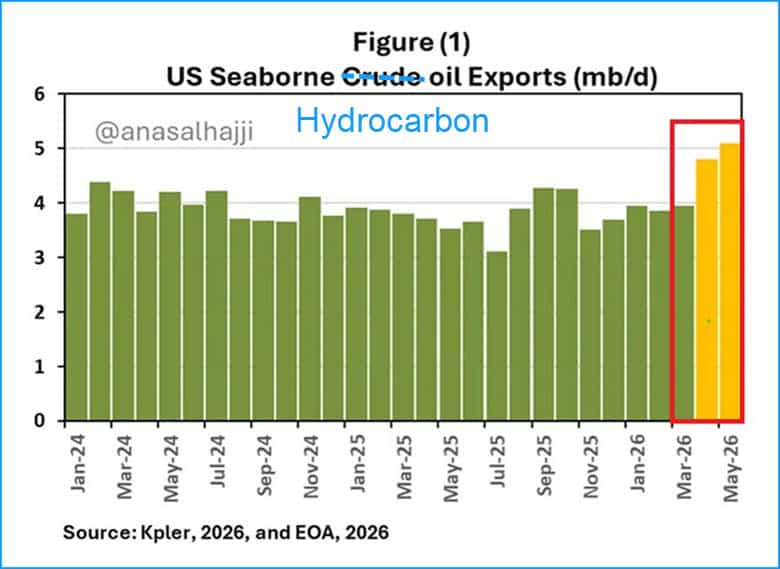

It is also true that the US has been exporting record amounts of hydrocarbons over the past 2 weeks (note that I have amended the chart title to reflect the more accurate definition):

(Source –Anas Alhajji on X)

However, it’s been reported that due to logistical reasons such as berth spaces and loading capacities, the most the US could export might be only another 1 Mb/d, which is a far cry from the 8 Mb/d missing in action from the Persian Gulf.

The idea that the US could somehow replace the lost flows from the Persian Gulf is so far removed from reality that it can be rejected immediately as a point of serious debate. The world is missing 8 Mb/d of exported Persian crude. The US is a net importer of 2 Mb/d of crude. It’s as simple as that.

The US Energy Balance Sheet

The energy position of any nation is constructed from ‘stocks and flows.’ The equation would be Production + Inventories – Exports = The Current Balance.

You can think of it as the nation’s energy balance sheet, if that helps.

To better understand why energy costs are about to rise sharply for US consumers (as well as the rest of the world), let’s step through that equation.

Production

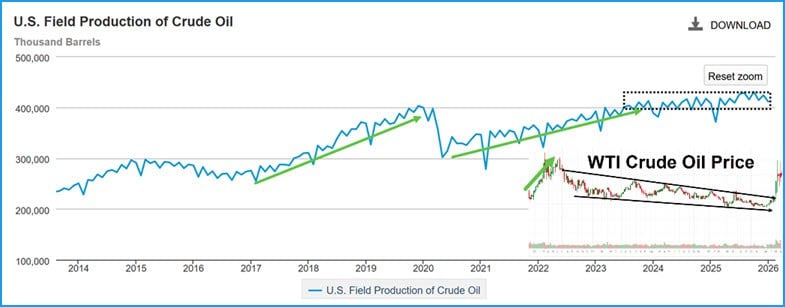

US production of crude oil hit a high in October of 2025. It has been more or less stagnant for 2.5 years. This is partly due to the shale fields having hit their maturity, and it’s partly due to oil prices having been too low to stimulate additional production from the more marginal shale areas.

In the chart below, you can see in the black dotted box that crude oil production has been flat, and beneath that, I’ve inset a chart of oil prices over that same period of time. The green arrows are times when production was growing.

Again, US oil production growth has been relatively flat over the past 2.5 years due to oil prices that were too low, and geology that has given up its best.

What has been growing, like mad, are the NGPLs. Those are up many millions of barrels per day over the past decade, and now top 10 Mb/d of production with exports topping 3 Mb/d.

But, again, these are surplus molecules that the US overproduces in abundance and would need to either export or simply burn them to dispose of them once storage areas were filled to the brim.

The key point here is that the US cannot meaningfully produce more crude oil over the short term, and the US is already a net importer of oil and therefore has no extra to export.

Which means that any additional exports will have to come from inventories.

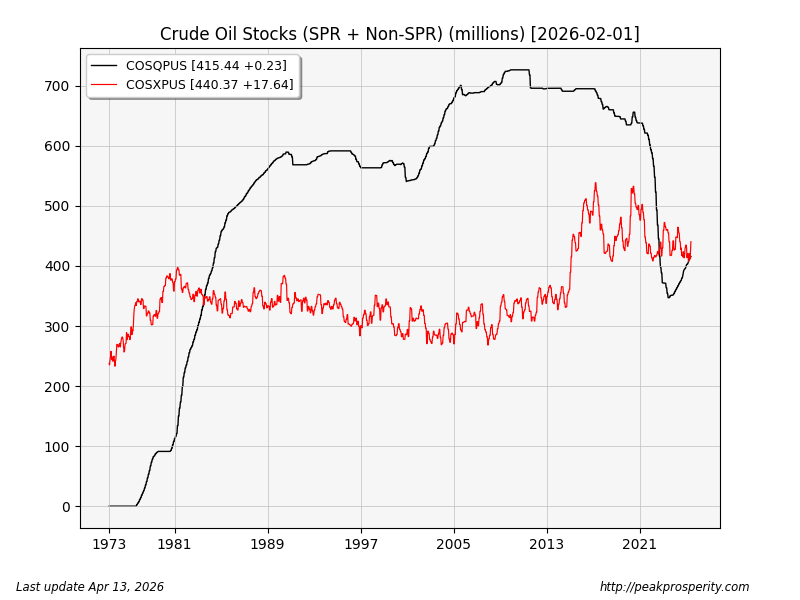

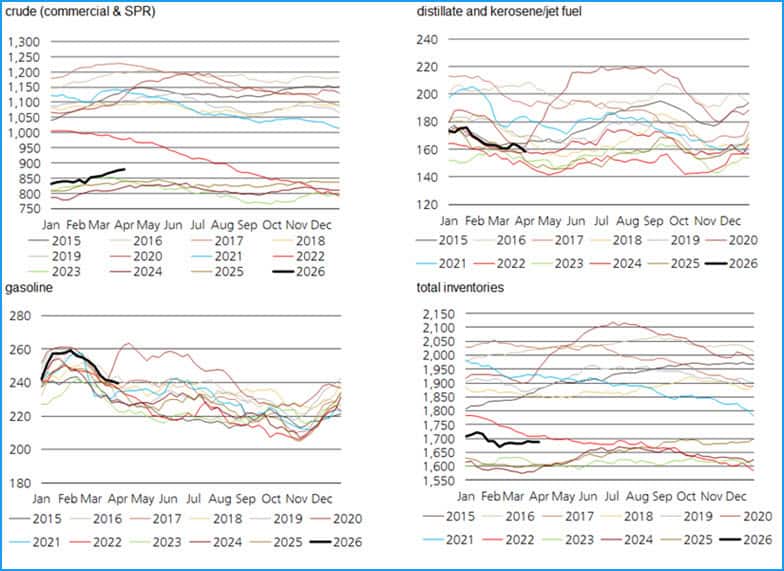

Inventories

Here’s where the story comes together. The US has some inventories of crude oil and related crude oil products, but all of those are either at the mid-range of the past ten years of data, or below.

(Source – Staunovo on X)

The punchline is that the US might be able to export from these middling to weak inventories, but only for a short while. Below a certain range, it either will not be able to because of minimum storage constraints, or because domestic consumers of these products will get worried and begin to bid up the prices to secure what they need.

This is how it always works, and now is no different.

When supplies get tight, prices go up. In economic jargon, oil prices are called “inelastic,” meaning smallish surpluses or deficits of supplies lead to outsized gyrations of prices.

A tiny bit too much supply (as small as 1% of daily consumption) and prices will decline by far more than 1%. Conversely, a tiny bit too little supply will lead to very large price increases. Oil prices aren’t elastic, able to absorb changes in supply-demand balances; they are more like a rigid see-saw that has a shorter length of board on the supply-demand side and a much longer board on the price side.

Conclusion

For political reasons, the US is about to load up a bunch of tankers with crude oil and related products. To the extent that those have to be drawn from inventory, prices will rise correspondingly for US consumers.

In other words, the Iranian War is about to come home.

I give it between 2 and 4 weeks before dwindling inventories become a major factor. This is the ticking clock that negotiators are working against.

To that, we should add that this week (April 13-17) is when the last tankers will be landing that left the Persian Gulf before the war started. That’s adding its own political pressure to the mix.

Which means the Iranians hold the cards. All they have to do is wait, which is easy compared to escalating military tactics.

Keep your eye on the negotiations. If the US continues to insist on getting everything it wants while denying anything Iran wants, then that dynamic will rapidly convert into significantly higher energy costs for the US and the entire world.

Let’s all hope the US-Israeli negotiators appreciate what’s truly on the line here. Beyond a certain price point, a world awash in $350 trillion debt cannot afford to service that debt. What happens after that is a massive economic crash led by the largest cascading debt defaults in world history. Which is to say nothing of the effects that will have on a quadrillion or two of derivatives.

In the meantime, we should all hope for the best but prepare for the worst. I am personally preparing as if US energy prices are going to double over the next month. That might be extreme, but it’s not an impossible outcome.

If you want to discuss this further or have any specific questions, I can be found 7 days a week, attending to these matters with my subscribers at PeakProsperity.com

Timestamps

00:00 The Impending Surge in Oil and Gas Prices

02:54 Understanding U.S. Oil Production and Exports

05:49 The Complexity of Oil and Natural Gas Liquids

08:47 The Role of the Strategic Petroleum Reserve

12:03 The Dynamics of Oil Pricing and Supply

14:55 The Future of Oil Exports and Market Chaos