Originally published at: https://peakprosperity.com/creak-pop-this-things-gonna-blow/

Every bubble is in search of a pin. The current stock market bubble isn’t just magnificent; it is without equal in the historical record.

As I like to say, plan accordingly.

Bubbles exist when asset prices rise beyond what incomes can sustain. This dynamic could not possibly be more evident than in this observation:

(Source)

A trillion of CapEx (Capital Expenditures) in a technology base that has a 5-7 year depreciation schedule, indicative of a short useful lifespan, with an income stream of $20 billion, indicating it would take 50 years to reach $1 trillion in revenues, to say nothing of profits?

That fits the definition of a bubble as cleanly as one could possibly hope for (or fear as the case may be).

Meanwhile, the recession indicators continue to mount:

Unless this time is different, a recession has already begun, according to the LEI. It just hasn’t yet been officially recognized.

Supporting the leading indicator series is this chart of existing homes for sale nearing the levels seen right before the GFC kicked off:

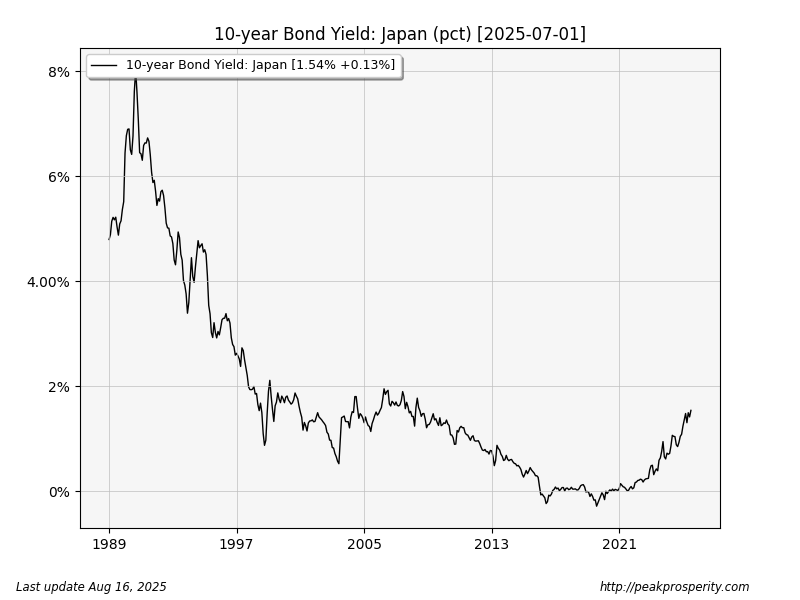

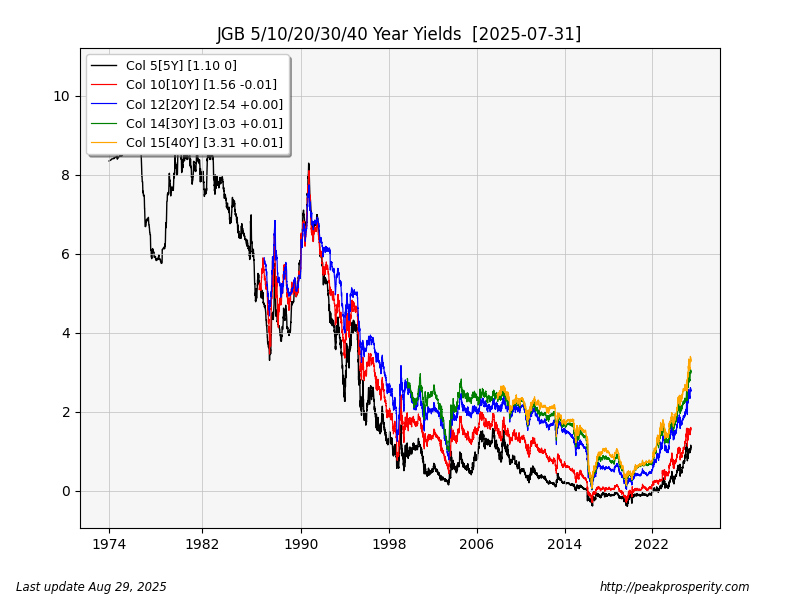

Of course, existing homes are wildly unaffordable, but what could help would be if long-term interest rates came down. On that front, the creaking and popping noises are reaching something of a crescendo. Japan’s bond market seems out of control, and yields are screaming higher:

The same is happening in Germany, France, the UK, and to a lesser extent, the US. But even here, the long bonds are not coming down in yield as Trump might have hoped as a result of having strong-armed the Fed into lowering short-term rates at the upcoming September FOMC meeting.

So, I’m not expecting much to change in the US real estate situation any time soon. That’s a big ship with enormous inertia, and right now its bow is swinging toward falling prices and lower sales.

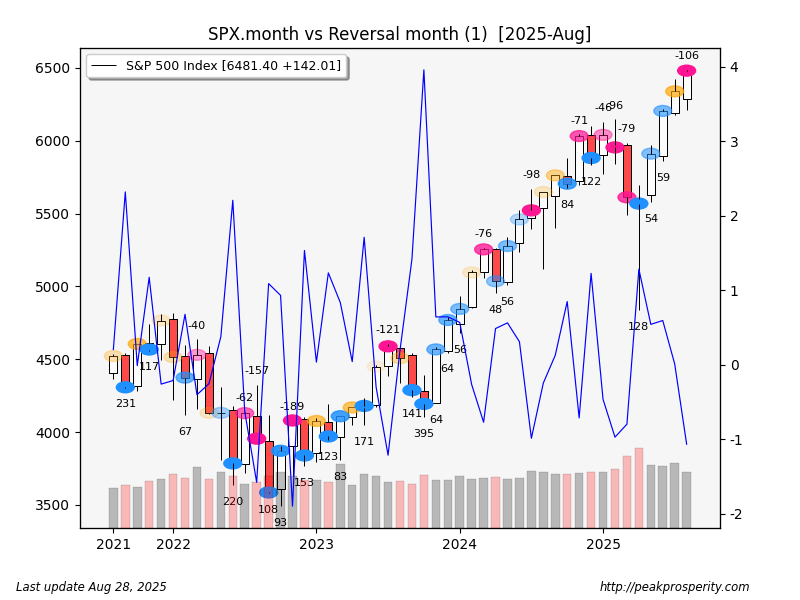

But all of that is merely a backdrop for the most magnificent bubble of our times, captured neatly in this one chart of NVDA’s stock price:

I asked Paul via text what his recollection was of why the bubble finally burst in 2000. He offered that it was a Broadcom earnings call where there wasn’t any particularly bad news, just a slight downward inflection to future earnings potential.

Pop!

That’s all it took.

NVDA just had an earnings call last night (after the time I recorded this Finance U episode) and the earnings were fine. But there was a slight hesitation among observers to believing NVDA’s CEO and his wildly optimistic projections:

(Source)

Obviously, NVDA is in a bubble, and obviously, someday that bubble bursts. Is that day today? Beats me, but I do know it’s coming, and my wish is for everyone to have a risk-managed approach to protecting their wealth when it finally bursts.

But that’s a vain wish because here’s the other bubble rule that’s both invisible and inviolable; It’s impossible for a majority of people to avoid massive losses.

It’s not a question of perception and action; it’s simply math. The true underlying value of the bubble’s assets is a fraction of what they trade for at the peak. That fraction represents what remains to be divvied up among those who own the bubble’s assets. By definition, there’s no way for a majority to come out whole.

Which means there’s a first-mover advantage that’s exceptionally large. Again, that advantage will belong to those with the ability to know a bubble when they see one, a nimble approach to investing, and with a good strategy in place before the bubble begins to unwind.

To schedule your first meeting with Paul and/or his amazing team – by far the best I’ve ever encountered – please click this link, fill out the simple form, and then respond promptly to their outreach to schedule your no-obligation consultation and portfolio review.

FINANCIAL DISCLAIMER. PEAK PROSPERITY, LLC, AND PEAK FINANCIAL INVESTING ARE NOT ENGAGED IN RENDERING LEGAL, TAX, OR FINANCIAL ADVICE OR SERVICES VIA THIS WEBSITE. NEITHER PEAK PROSPERITY, LLC NOR PEAK FINANCIAL INVESTING ARE FINANCIAL PLANNERS, BROKERS, OR TAX ADVISORS. Their websites are intended only to assist you in your financial education. Your personal financial situation is unique, and any information and advice obtained through this website may not be appropriate for your situation. Accordingly, before making any final decisions or implementing any financial strategy, you should consider obtaining additional information and advice from your accountant or other financial advisers who are fully aware of your individual circumstances.