Originally published at: https://peakprosperity.com/finance-u-energy-prices-spike-inflation-set-to-roar-and-urgent-warnings-about-credit-markets/

US-Iran talks have stalled, and the main talking point being circulated by Trump and Bessent is that Iran’s economy is destroyed and, as the WSJ put it, is in a “death spiral.”

The plan, apparently, is hoping that economic pain forces an Iranian political capitulation or uprising. Hope is a terrible strategy, especially given Iran’s past demonstrations absorbing considerable losses.

Meanwhile, the US is having its own pain tolerance thresholds explored with gasoline prices suddenly rising to an average of $4.50/gal (and over $5 in an increasing number of locations).

“Somebody” in the US system worked diligently to keep oil from rising over $100/bbl. April 28th saw oil rise and fall above and below the magic $100-mark numerous times, with clear signs of capping it under $100 at other moments:

But these efforts to keep the price low has only led to more demand pressure on US inventories of crude oil and petroleum products. Eventually, that process will have to end once stockpiles become worryingly low.

Inflation

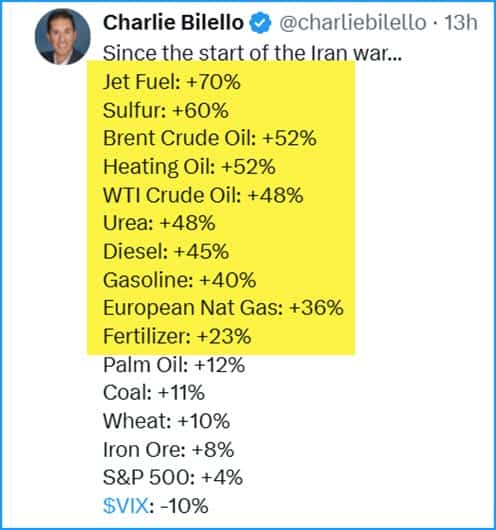

Since the start of the Iran war, a very wide range of energy and related products, including food, have risen dramatically in price:

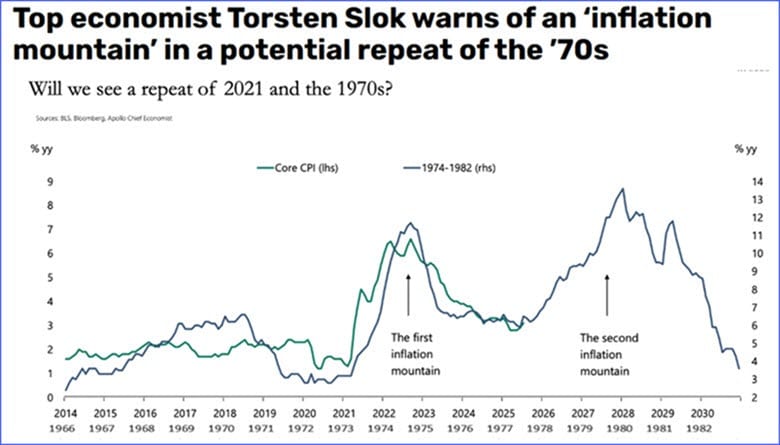

We expect these price hikes and even shortages to persist and increase for the duration of the war. If the Strait of Hormuz remains closed for another six months, then there’s every chance that we will almost perfectly repeat the dreaded ‘double hump’ inflation of the 1970’s and early 1980’s.

My prediction is that because this energy shock is so much larger than the 1973/74 shock, and because it encompasses so many more essential items than just crude oil alone, the second inflationary shock could easily be the most extreme one the dollar has ever faced. I can see a path to 18% to 20% inflation.

The effect on the bond markets will be extreme. The effect on poor countries and less wealthy people, even in core countries, will be extreme.

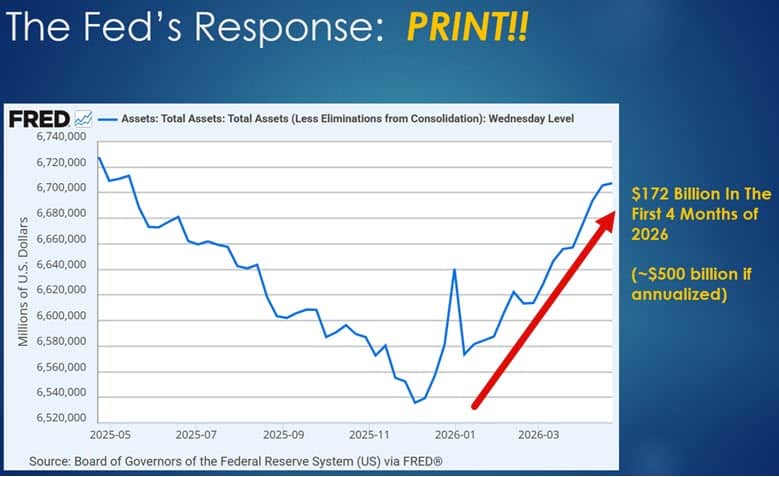

But, despite any of that, the Fed will print, and then print some more to keep its precious stock market moving up and to the right.

Actually, the Fed has already started printing, to the tune of $172 billion in just four months (which annualizes out to a cool half a trillion):

With inflation already picking up steam and equities at record highs, one really must ask what emergency the Fed is responding to with all that printing? Maybe the looming credit/Treasury crisis outlined below…

Super Expensive Equities

Please watch this entire clip with the legendary investor Paul Tudor Jones:

Paul Tudor Jones just said something the market really doesn't want to hear."We're clearly so leveraged in equities in this country. We're 252% of stock market cap to GDP. In 1929, we were at 65%. In 1987, about 85%. In 2000, we got to 170%. And now we're at 252." Every… pic.twitter.com/JMc7xcjFl7

— StockMarket.News (@_Investinq) April 28, 2026

With equities now at an unprecedented 232% of GDP, should they ‘mean correct’, the consequences would be an absolutely brutal stock market decline, which Paul put this way in the above interview:

“If you think about the periodicity of significant bear markets since 1970, we get a mean reversion about every ten years. That would be a 30 to 35% decline. Well, 35% on 250% of GDP is 89% of GDP. The reverse wealth effect, oh my gosh. 10% of our tax revenues are capital gains; they go to zero.”

Paul and I discussed what this means in some detail in the podcast.

Is a Bond Market Collapse on the Way?

Finally, we discussed the worrying comments made by both Hank Paulson (ex-Treasury Secretary and Goldman Sachs insider) and Jamie Dimon (CEO of JPMorgan).

Hank was promoting creating some sort of response playbook for when (not “if”) “we hit the Treasury wall.” When we hit it, he said that it will be “vicious.”

The Former Treasury Secretary Who Once Needed a $700 Billion Bailout Warns of Vicious” Bond Crash “We need an emergency break-the-glass plan, which is targeted and short-term, on the shelf, so it’s ready to go when when we hit the wall,” Paulson said in an interview for… pic.twitter.com/Z8UOHdmO4H

— kristen shaughnessy (@kshaughnessy2) April 16, 2026

Vicious? This is unusually blunt language for a big financial player and ex-politician; usually, they are far more reserved and delicate in their phrasing. Maybe he was just having a bad day.

But then along came Jamie Dimon speaking about credit markets more broadly, also speaking as if some sort of crisis is a done deal. He said, “The way it’s going now, there will be some kind of bond crisis.” When that credit crisis hits across all lending, he said it will be “worse than people think. It might be terrible.”

Jamie Dimon today: "The way it's going now, there will be some kind of bond crisis."He added that when a credit recession hits across all lending, it will be "worse than people think. It might be terrible."This is the CEO of the world's largest bank.Nothing to see here...

— Nic (@nicrypto) April 28, 2026

Terrible? Who speaks like that? Certainly not the head of the largest bank in the world…except that’s what he said. What does he know that we don’t know?

Timestamps

00:00 The Rising Tensions: Iran and Oil Prices

02:45 Market Reactions and Speculations

05:50 The Impact of Oil Prices on the Economy

09:05 The Future of Gasoline Prices

12:10 The Battle for Oil Prices

15:00 Supply and Demand Dynamics

18:10 Inflation: A Looming Threat

21:00 The Double Hump Inflation Scenario

24:05 Food Prices and Global Unrest

30:40 The Impact of El Niño on Food Prices

32:55 Understanding Agricultural Commodity Trends

35:40 The Role of Money Printing in Inflation

40:10 The Consequences of Federal Reserve Policies

45:35 The Dangers of Inflation and Economic Stability

51:55 Evaluating the Current Equity Market

58:40 The Psychology Behind Market Bubbles

01:00:20 Market Valuation and Mean Reversion

01:02:45 Historical Context of Market Declines

01:05:35 The Role of Federal Reserve and Monetary Policy

01:08:55 Lessons from History: The Roman Empire to Today

01:10:25 The Risks of Overexposure to Equities

01:13:10 Navigating Market Volatility and Investor Behavior

01:15:25 Energy Supply and Economic Stability

01:17:35 The Japanese Market Experience and Investment Strategies

01:19:40 Warnings from Financial Leaders

01:21:05 The Looming Credit Crunch

01:25:45 The Bond Crisis and Market Implications

01:31:10 Insider Selling and Market Signals

FINANCIAL DISCLAIMER:

The information contained in this video and the resources available for download through our affiliated website are not intended as and shall not be understood or construed as financial advice, nor should be interpreted as a solicitation to sell or offer to sell investment advisory services. No person who currently works for or contracts with Peak Prosperity or Peak Financial Investing is an attorney or accountant, nor are we holding ourselves out to be, and the information contained in the video and on the website is not a substitute for legal or tax advice from a professional who is aware of the facts and circumstances of your individual situation. While Peak Financial Investing is a registered investment advisor, please note that this podcast is not intended to be investment advice.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. We have done our best to ensure that the information provided is accurate and provides what we feel is valuable information. The views expressed are subject to change based on market and other conditions.<

No guests or clients appearing on the podcast receive any form of compensation for their appearance and obtained no other benefit from either Peak Prosperity or Peak Financial Investing.

All investing involves risks including the possible loss of capital. Asset allocation and diversification does not ensure a profit or protect against loss. Please note that out- performance does not necessarily represent positive total returns for a period. There is no assurance that any investment strategy will be successful. All investments carry a certain degree of risk. Dividends are not guaranteed, and a company’s future ability to pay dividends may be limited.

Additional important disclosures for Peak Financial Investing may be found in our Form ADV Part 2A, which can be found at https://adviserinfo.sec.gov/firm/summary/319672.